The Gordon Growth Model (GGM) formula or the Dividend Growth Model is used to determine the intrinsic value of a stock based on the current dividend rate and its expected constant growth rate. The Model calculates the intrinsic or fair value of a stock, and thus it ignores current market conditions. The Gordon Growth Model is a simplified version of the Dividend Discount Model (DDM). The Gordon Growth Model was first developed by Myron J. Gordon and published in an article entitled “Dividends, Earnings, and Stock Prices” in 1959 in the journal, The Review of Economics and Statistics.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

The Gordon Growth Model provides a relatively quick and simple way of determining stock valuation with only knowledge of the expected dividend rate expressed as dividends per share, an expected or required rate of return, and the expected dividend growth rate. Hence, it is an excellent valuation method for valuing dividend growth stocks. There are some limitations to the Gordon Growth Model, but it works reasonably well for mature companies with fairly predictable and stable dividend growth rates. For this reason, it should not be used or companies that do not pay a dividend or just started to pay a dividend.

However, one should always compare the results of the Gordon Growth Model with other valuation methods, like price-to-earnings ratio, when performing financial modeling and fundamental analysis.

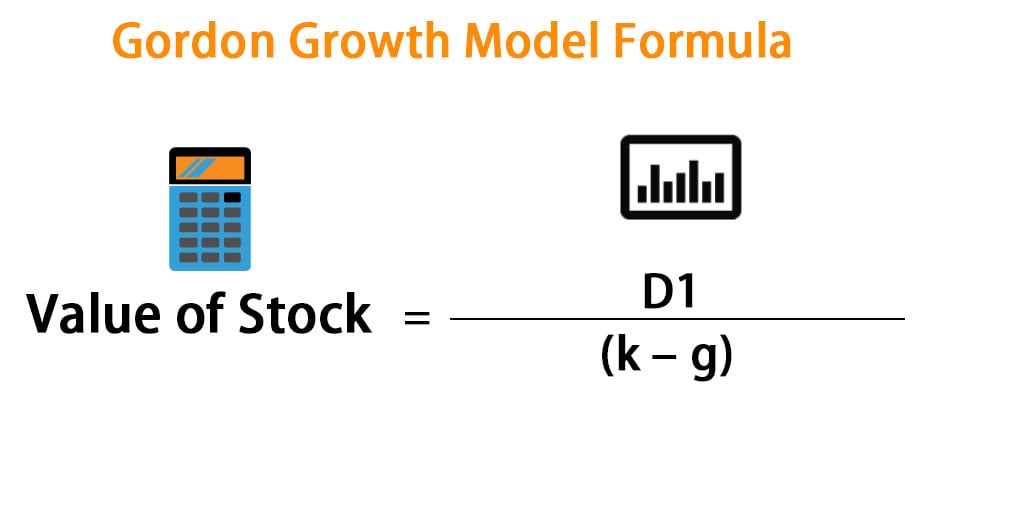

Gordon Growth Model Formula

The Gordon Growth Model takes an expected dividend per share and solves for the present value of an infinite series of future dividends. One important aspect is that the simplest form of the Model assumes a constant dividend growth rate out to infinite time. The formula for the Gordon Growth Model is

where P is the present value of each share of the company, D is the current annual dividend per share, r is the expected rate of return or cost of equity, and g is the expected annual dividend growth rate to infinite time. The quantity D is the easiest to determine as it is the actual expected dividend per share. The quantity g is an estimate but can be based on historical growth rates extrapolated into the future. The quantity r is also an estimate but it is the discount rate of return and it is also referred to as the discount rate.

Expected Rate of Return

One method to estimate the quantity r is to use the Required Rate of Return as determined under the Capital Asset Pricing Model (CAPM). If consistently applied, this will let you compare different investments with the similar risk profiles, e.g. regulated utilities. There are some limitations to using the Capital Asset Pricing Model but I will not address them here. In the equation below the risk free rate of return is often the interest on long-term government bonds, e.g. U.S. 10-year Treasury. The market rate of return can be taken as the long-term average return of a diversified index, such as the S&P 500 Index.

The result of equation (1) can be compared to the current share price. If the quantity P is greater than the current share price, then the stock can be considered overvalued and vice-versa. However, the Gordon Growth Model and formula should not be used in isolation. Rather, it should be used in tandem with other valuation methods, e.g. price-to-earnings ratio or discounted cash flow (DCF).

Gordon Growth Model Assumptions and Limitations

The Gordon Growth Model has a few assumptions and limitations. The obvious one is that the Gordon Growth Model assumes a constant dividend growth rate out to infinite time. This is generally a valid assumption for mature, stable companies that have been paying dividends for some time, e.g. Dividend Kings, Dividend Aristocrats, and Dividend Champions.

From an industry perspective, it is also valid for banking, utility, consumer staples, and real estate companies. Companies in these industries tend to have higher dividend and stable dividend growth rates. Large banks and financial companies generally means that they will not generate high growth, rather growth will be slow or moderate. In general this means that earnings growth rates and thus dividend growth rates are somewhat predictable. Utilities are regulated and their returns on equity are predictable. This means that they too have stable earnings growth rates and dividend growth rates. Consumer staples companies in general do not grow very fast. They have high dividends and payout ratios hence the dividend growth rates tend be predictable. Real estate investment trusts or REITs must pay out 95% of their earnings as dividends and growth at stable rates. This means that their dividends growth rates are somewhat predictable.

Dividend Growth Rate Should Be Relatively Stable

However, the Gordon Growth Model is generally not valid for companies that have only recently started to pay a dividend where the dividend growth rate is very high initially and then tapers off. The assumption is also not valid for a company that has a volatile dividend growth rate due to cyclicality in the business. For example, many industrial stocks exhibit long-term dividend growth. But when the economy contracts and thus earnings contract the dividend growth rate is very low. Industrial companies often try to conserve cash during these times. On the other hand, when the economy and earnings are expanding the dividend growth rate tends to be comparatively high.

Dividend Growth Rate Must Be Less Than The Expected Rate of Return

The second important limitation is the subtractive relationship between the expected rate of return and the dividend growth rate. If these two quantities are the same the quantity P approaches infinity. An obvious breakdown in the Gordon Growth Model.

Additionally, if the quantity g is greater than the quantity r, this means that the dividend growth rate is greater than the required rate of return. Then the result of equation (1) is a negative value and thus not meaningful. This often occurs when a company first starts paying a dividend and the payout ratio is low. The dividend growth rate can be very high for several years as the payout ratio rises. A high dividend growth rate can also occur when a company is growing rapidly through M&A.

Other Uses of Cash Are Not Considered

The third limitation is that the Gordon Growth Model makes the inherent assumption that all free cash flow (operating cash flow – capital expenditures) is used to pay dividends. Obviously if a company does not pay a dividend the Gordon Growth Model cannot determine an intrinsic value estimate for the stock. Other uses for free cash flow such as paying debt early or stock buybacks are not considered in the Gordon Growth Model. It also excludes intangibles such as brand strength, customer loyalty, intellectual property, and other non-dividend attributes that have value.

Assumes Company Operates for Forever

As one last point the Gordon Growth Model assumes that the company will operate forever, i.e. to infinite time. This is obviously not true. But on the other hand, most large capitalization, blue-chip companies tend to be around for decades. Even if they undergo M&A, the successor organization often pays a dividend.

Sensitivity to Rate of Return and Dividend Growth Rate

Small investors should be aware that the present value of a stock determined from equation (1) is very sensitive to the quantities r and g. In the example on Coca-Cola below a change in the assumption for the dividend growth rate from 5% to 6% causes a large increase in the intrinsic value estimate to $82 per share.

The Gordon Growth Model is also sensitive to the expected rate of return. It is for this reason that performing a sensitivity analysis is important. The Gordon Growth Model results in an increasing fair value estimate with higher starting dividends, at higher dividend growth rates, or lower expected rates of return.

Gordon Growth Model Examples

In this example, we use the Gordon Growth Model formula in equation (1) to determine the fair value a stock. We will look at a large-cap company that is a Dividend King since the Gordon Growth Model works best for mature companies that have been paying dividends for an extended duration.

Gordon Growth Model Example 1 – Coca-Cola (KO)

For our first example we choose, The Coca-Cola Company (KO). Coca-Cola has been paying a growing dividend for 58 years making it a Dividend King. The forward annual regular cash dividend payout is now $1.64.

The trailing 5-year dividend growth rate is about 5.6% and the trailing 10-year dividend growth rate is about 6.9%.

We will use 5% as the annual dividend growth rate to infinite time in order to be conservative. Our desired or expected rate of return is 8%, which is conservative, and somewhat below the average stock market return over long time periods. We ignore the effects of market volatility or beta in this example. Now using formula (1) we get:

The present value of $54.67 is the intrinsic value estimate determined from the Gordon Growth Model. From the perspective of a small investor buying Coca-Cola stock one would want a price below $54.67 in this example.

Gordon Growth Model Example 2 – Multistage Model for a Hypothetical Company

In the above example we made a key assumption that is a constant dividend growth rate. However, the Gordon Growth Model can be adapted for different near-term dividend growth rates that are higher and a constant long-term dividend growth rate. For instance, we can say that for an arbitrary stock ‘A’ the near-term dividend growth rate is 8% in year 1, 6% in year 2, 10% in year 3, and then a constant 5% growth rate as a terminal value after that. We first need to calculate the dividends in each of those years assuming $1.64 in year 1. So, we get:

The next step is to calculate the present value of every single dividend using the 8% expected rate of return.

Then we calculate the value of the dividends in the constant growth rate period in year 5.

The next step is to determine the value in year 5.

The present value of the constant growth rate period is then calculated.

Now add the present values for all years.

So, after all that work one can compare the intrinsic value estimate of the multi-stage Gordon Growth Model with the current stock price. We did these calculations by hand. But it is a simple matter to perform the financial modeling in a spreadsheet.

Gordon Growth Model Example 3 – Reverse Problem – What Dividend Growth Rate Would Justify The Stock Price?

The simplicity of the Gordon Growth Model means that the reverse problem can also be solved. What dividend growth rate justifies the current price? in this case you are solving for the quantity g when you know the stock price. Let’s use a real world example for Coca-Cola, which is trading at $51.04 at the most recent close.

In this case, the quantity g is equal to 4.8%. Note that we ignored volatility in this calculation. If the known dividend growth rate is less than this value, then the stock is overvalued by this method. On the other hand, if the dividend growth rate is higher than this value, then the stock is undervalued by this method.

Final Thoughts on the Gordon Growth Model

The advantage of the Gordon Growth Model and the formula is that it is relatively simple. For that reason it is also powerful. Investors can perform a quick calculation to get some idea if a stock is undervalued, fairly valued, or overvalued. Consequently, the Model is a good one for investors following a dividend growth investing strategy. More complex models exist but the Gordon Growth Model has stood the test of time and is still used today to determine intrinsic value. This is due to its simplicity and its focus on fundamental analysis. One does not need a company’s stock price or complex data. A spreadsheet to perform the financial modeling is all that is needed.

But one must remember that the Gordon Growth Model has its limitations. If the rate of return or dividend growth rate assumption are inaccurate, then the resulting intrinsic value calculation will not be correct. Next, if the dividend growth rate is not linear, a multi-stage model must be utilized.

The Gordon Growth Model is often best to use it in the context of multiple valuation models. For instance one can compare the stock valuation from the Gordon Growth Model with that based on earnings multiple or discounted cash flow. This comparison also provides a reality check for your assumptions. If the intrinsic fair value estimates from the different valuation models are too different then one needs to dig a little deeper into the reasons.

Disclosure: Long KO.

Related Articles on Dividend Power

- John Bogle’s Estimated Future Annual Total Return Formula

- What is the Rule of 72? We Explain It With Examples

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.

All true IMO for dividends and dividend growth investing.