Carter’s, Inc (CRI) cut its dividend due to tariffs, inflation, and a stressed customer base. Additionally, difficult market and business conditions have created uncertainty for the company. The firm slashed its dividend to zero during the pandemic in fiscal year 2020 and restored it but too quickly.

The share price has fallen dramatically since late 2021. Investors have been selling this dividend stock due to concerns about operating results, a declining outlook, and a possible dividend cut, as safety concerns have increased. Depending on market and business conditions, as well as earnings results, another reduction may occur in the future.

Affiliate

Portfolio Insight is a leading portfolio management and research platform.

- 9,000+ stocks and ETFs in its database

- Access up to dozens of metrics, 20-years of financial data from S&P Global, fair value, margin of safety, charting, etc.

- Avoid dividend cuts with the Dividend Quality Grade and screening tools.

Click here to try Portfolio Insight for free (14-day free trial).

Overview of Carter’s, Inc

Carter’s, Inc. was founded in 1865 in Needham, Massachusetts. The founding family owned the business until 1990. Today, it is based in Atlanta, Georgia. It designs and sells children’s clothing, footwear, and accessories through department stores, discount retailers, its own Carter’s and OshKosh B’gosh stores, and its website. Essential brands include Carter’s OshKosh B’gosh and Skip Hop. The company also sells exclusive brands at Target, Walmart, and Amazon, such as Just One You, Precious Firsts, Genuine Kids, Child of Mine, and Simple Joys.

Total revenue was $2,844 million in the fiscal year 2024 and $2,812 million in the past twelve months.

Dividend Cut Announcement

During an update of the company’s return of capital strategy on Tuesday, May 20th, Carter’s Companies (CRI) lowered its dividend. The company’s quarterly dividend rate was $0.80 per share before the announcement. The dividend is now $0.25 per share, a 68.8% reduction. In the update on May 20th, the press release stated,

“Our current cash position and liquidity are strong and are forecasted to remain so. However, as we anticipate making strategic investments in our business in the coming years, our current dividend is misaligned with our current level of profitability, especially against the backdrop of a challenging market environment and the possibility the Company may incur significantly higher product costs as the result of the new proposed tariffs on products imported into the United States.”

“In light of these factors, our Board of Directors declared a dividend of $0.25 per share payable on June 20, 2025, to shareholders of record as of June 2, 2025. As the Company progresses in its goal of returning to growth, the Company will continue to evaluate its capital allocation priorities, including the amount and timing of returning capital to shareholders.”

Effect of the Change

By executing an approximately 69% dividend cut, Carter’s sought to align its dividend with its level of profitability. The company is facing challenging market and business conditions, expects revenue and income to be lower in 2025, and has suspended its guidance. Additionally, tariffs will likely impact the firm’s margins and, consequently, its profitability. They had a 1-year streak of increases. The result is less free cash flow is required for the dividend payout, allowing the retailer to preserve liquidity.

Challenges

Carter’s is facing a challenging market and economic environment globally because of tariffs and market conditions. A stressed customer is also affecting results.

Market and Business Uncertainty

The American economy ended 2024 with significant optimism and momentum. However, the ad hoc enactment of tariffs and their ambiguous nature has affected consumer and business confidence. Moreover, no one really knows what the future tariffs will be. This lack of stability has resulted in significant uncertainty for businesses, as they cannot accurately plan or model future costs. Although the highest tariffs are currently paused, the situation remains unpredictable.

Tariffs

Tariffs are a major concern for Carter’s. Essentially, all its production is overseas in countries with higher tariff rates. For instance, China currently has a 55% rate, while other countries are subject to the de minimus rate of 10%. That said, higher rates may return after the 90-day pause is completed. Tariffs are a direct cost to importers and will be passed on to consumers.

Inflation and Stressed Consumers

Inflation remains a primary concern of retailers. Cost of goods inflation had stabilized but may be rising again. Inflation impacts margins because not all costs can be immediately passed on to customers. Additionally, labor inflation remains higher than usual, placing upward pressure on wages. Low unemployment has made it difficult to find inexpensive labor.

Dividend Safety

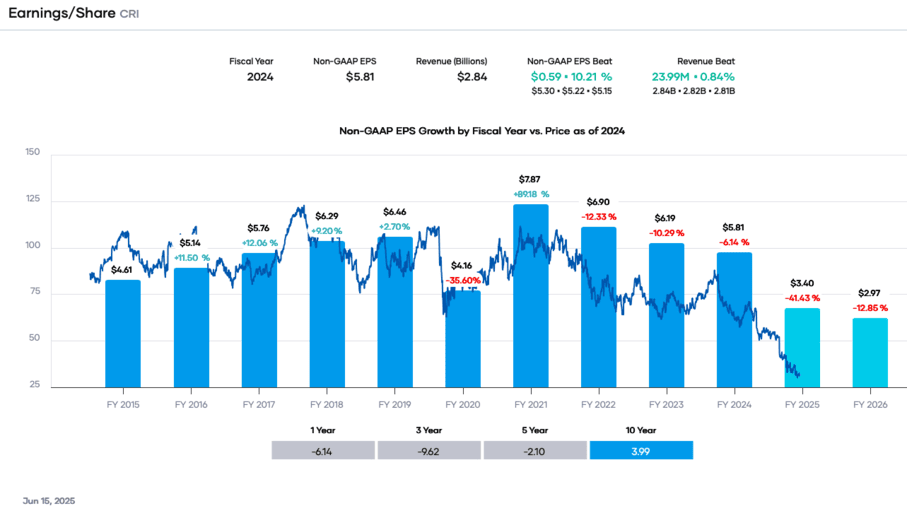

Besides the pandemic year, Carter’s revenue and earnings per share (“EPS”) were generally rising until fiscal year 2021. Earnings per share exhibited a rising trend, peaking in fiscal year (FY) 2021 at $7.87. However, it has declined since then. Earnings per share are expected to decrease to $3.40 per share in FY 2025.

As seen in the chart below from Portfolio Insight*, the dividend yield increased rapidly to over 10% due to a declining share price. This value, along with the rapid rise, indicates poor operating results. In addition, 10% is often considered a threshold for a distressed company. The yield was much greater than the 5-year average of 3.90%. After reducing the dividend by approximately 69%, the dividend yield is now around 3.21%. The quarterly rate is $0.25 per share. However, the yield is still considerably higher than that of the S&P 500 average.

The annual dividend now requires approximately $36.5 million ($1.00 yearly dividend x 36.5 million shares), compared to $116.2 million in fiscal year 2024. In addition, based on the 2025 consensus estimates of $3.40, the estimated payout ratio will be approximately 28%. We expect the annual difference in cash flow requirements to enhance liquidity, enabling the firm to manage periods of lower sales and profitability.

Although the dividend is in a better position and more secure now, the firm’s dividend is not entirely safe. Poor operating results or significantly higher tariffs may force another dividend cut. Additionally, Carter’s receives a BB+/Ba3 non-investment-grade speculative rating from the credit rating agencies.

In addition, the restaurant firm receives a dividend quality grade of ‘F’ from Portfolio Insight. Hence, Carter’s is at the bottom of all dividend stocks tracked. We view the equity as at risk for another dividend cut unless the results improve and tariff policies stabilize.

Final Thoughts on the Carter’s (CRI) Dividend Cut

Before the pandemic, Carter’s was a dividend growth stock, with annual dividend increases between 2013 and 2020. However, COVID-19 interrupted the streak and reduced the payout to zero in FY 2020. The firm restored the dividend and increased it too rapidly in the face of falling revenue and earnings. However, market and business uncertainty, inflation, and a stressed customer have created significant challenges for the clothing designer and marketer. As a result, Carter’s cut its dividend. However, we view the firm as at risk for another reduction.

Related Articles on Dividend Power

- Kohl’s Dividend Cut: A Symptom of Broader Retail Industry Challenges

- V.F. Corporation (VFC) Dividend Cut

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.