V.F. Corporation (VFC) was nearly a Dividend King, with 49 years of dividend increases before the dividend cut. Rarely does a company with such a long track record cut the dividend. Most companies try to defend the dividend. But the company added debt during the COVID-19 pandemic. Subsequently, inflation caused input prices to rise and consumers to retreat from discretionary purchases. Also, supply chains have been stressed for much of 2021 and 2022. As a result, the stock price dropped, and the dividend yield surged. The payout became unsafe. Consequently, VFC cut the dividend.

Affiliate

Portfolio Insight is a leading portfolio management and research platform.

- 9,000+ stocks and ETFs in its database

- Access up to dozens of metrics, 20-years of financial data from S&P Global, fair value, margin of safety, charting, etc.

- Avoid dividend cuts with the Dividend Quality Grade and screening tools.

Click here to try Portfolio Insight for free (14-day free trial).

Overview of V.F. Corporation (VFC)

The V.F. Corporation was founded in 1899. It is a global apparel and footwear company headquartered in Denver, Colorado. The company was formerly known as Vanity Fair mills until 1969 when it changed its name. Today, VFC sells outdoor, lifestyle, and casual apparel; footwear; equipment; backpacks; streetwear; etc.

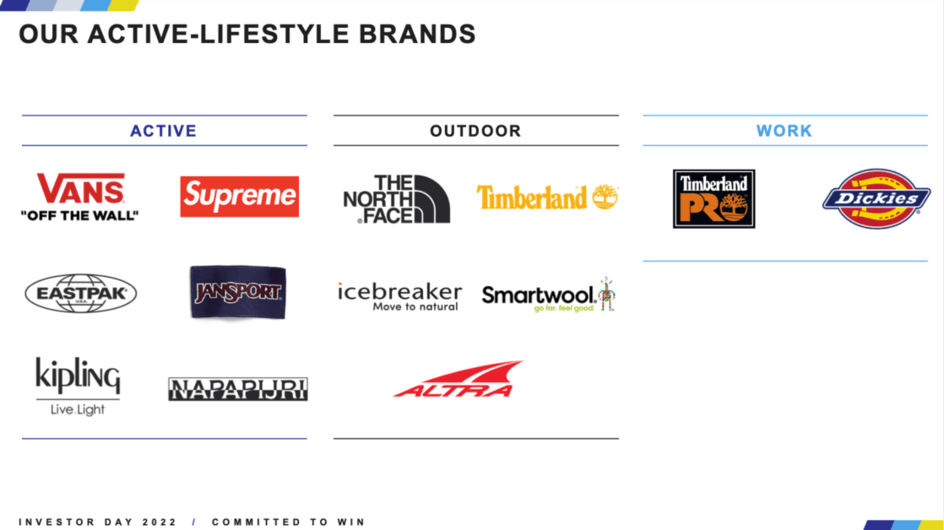

The company’s 13 brands are categorized into Outdoor, Active, and Work. The leading brands are North Face, Timberland, Smartwool, Icebreaker, Altra, Vans, Supreme, Kipling, Napapijri, Eastpak, JanSport, and Dickies. In addition, the company is the market leader in the U.S. backpack market with the JanSport, Eastpak, Timberland, and North Face brands. It has a 55% market share.

Total revenue was $11,842 million in 2022 and $11,698 million in the past twelve months.

Dividend Cut Announcement

V.F. Corporation cut its quarterly dividend by 41.2% on February 7, 2023. The company’s quarterly dividend was $0.51 per share. The new dividend rate is $0.30 per share. Specifically, VFC’s Interim CEO, Benno Dorer, stated,

“We are pleased to reaffirm the recently communicated full year 2023 EPS outlook with revenue growth at approximately 3%, after navigating an increasingly challenging fiscal Q3. Spending the last few weeks with VF’s dedicated and talented teams around the world has reinforced my belief in the tremendous opportunity ahead for our company. We are committed to improving execution through a sharpened focus on the biggest consumer opportunities and enhanced operational performance. Consistent with this objective, we are shifting resource priorities across the Company, including by reducing the dividend, exploring the sale of non-core assets, cutting costs and eliminating non-strategic spend, while enhancing the focus on the consumer through targeted investments. We are confident these actions will enable a return to profitable and sustainable growth and, with that, strong shareholder value creation.”

Challenges

V.F. Corporation’s issues are high leverage, rising interest rates, high inflation, and high inventory.

Debt and Leverage

VFC’s total and net debt has risen because of acquisitions and share buybacks. For example, the company acquired Supreme in 2020 for $2.1 billion in cash, indebtedness, and working capital. In addition, the company has been aggressively lowering its share count. As a result, total and net debt has grown.

At the end of Q3 fiscal year 2023, the firm had $571.4 million in cash, short-term debt of $901.7 million, current long-term debt of $910.6 million, and long-term debt of $4,617.4 million. To put this in context, V.F. Corporation has a market capitalization of about $8.4 billion. Consequently, total debt has increased relative to market capitalization as the latter has come down.

The leverage ratio has come down from its peak but is still elevated and above the target of 2.5X. Management stated,

“What this does is it strengthens our balance sheet. Our gross debt to EBITDA right now is about 4.5x and this gets us much closer to our target of 2.5:1…And then what are we going to do with the capital, pay down debt, serve the dividends. And then I would say, secondarily, but still importantly, it gives us flexibility to invest in our brands and consumers.”

Thus, it is unsurprising that VFC cut the dividend and is redirecting capital and free cash flow (FCF) to pay down debt and invest in brands and consumer initiatives.

Higher Interest Rates and Expenses

Higher interest rates make debt costlier, especially short-term and current long-term debt, which renews within twelve months. VFC has nearly $1.9 billion of debt in this category.

Interest rates are rising because of the U.S. Federal Reserve’s objective to withdraw liquidity from the bond market and raise the Federal Funds rate to counter high inflation. In about 12 months, the Federal Funds rate has risen to 4.75% – 5.00% from 0.0% – 0.25%. As a result, this significant increase has caused short-term rates to spike. In addition, business loans or revolving credit lines are often based on the Prime Rate of around 7.75%, a 4.55% rise in the last year, like the Federal Funds rate. A second loan index, the Secured Overnight Financing Rate (SOFR), has increased rapidly too.

Hence, interest expense for VFC is trending up. In the last quarter, interest expense was ~$54 million, more than the $34 million in the prior quarter. With rising interest payments and lower earnings per share, VFC probably needed to cut the dividend.

Inventory Issues

Clothing and footwear companies are struggling with excess inventory. Some companies have done a better job managing it than others. VFC is not one. According to the CEO,

“Inventory has been a challenge. It’s been an overhang for us for a couple of quarters and continues to certainly persist.”

But he expects supply chain issues to fade, merchandise levels to decline, and margins to rise. If his expectations are met, it should make V.F. Corporation more profitable. Also, the company is struggling with high inflation affecting making retail consumers wary about purchasing new apparel and footwear.

Dividend Safety

V.F. Corporation’s dividend safety declined in the two years before the cut. The dividend yield was at ~8.5%, a value associated with greater risk. Moreover, the company received a dividend quality score of F. After the cut, the grade remained the same, but the dividend safety improved.

The payout ratio is now approximately 58% based on an annual dividend rate of $1.20 and consensus forward earnings of $2.08 per share. This value is acceptable and below our target of 65%.

The annual dividend now requires about $466.8 million ($1.20 yearly dividend x 389 million shares) compared to $773 million in the fiscal year 2022. The dividend-to-FCF ratio is now 75%, a better value than before the cut. However, this quantity is still above our criterion of 70%. That said, VFC’s capital expenditures are elevated and should come down.

V.F. Corporation’s balance sheet is leveraged and the firm needs to reduce the leverage ratio. But the credit rating agencies have assigned a BBB+/Baa1 lower-medium investment grade credit rating.

Overall, the cut improved dividend safety and coverage. Thus, the company can pay the current annual dividend rate. But a possible recession may lower consumer spending and place the dividend under pressure.

Final Thoughts on V.F. Corporation (VFC) Dividend Cut

V.F. Corporation’s problems are primarily of its own making. Higher inventories mean the company is not attuned to consumer tastes and demand. In addition, the Supreme acquisition increased net debt and leverage. However, higher interest rates, inflation, and supply chain issues are out of the company’s control.

Investors had sold V.F. Corporation’s stock since late-2019 about when the Supreme acquisition announcement was announced. COVID-19 and the aftermath have made for a challenging operating environment. Ultimately, VFC needed to cut the dividend.

Disclosure: None

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.