The year 2022 was disappointing after two excellent years of total returns driven by the COVID-19 pandemic. Although the pandemic’s economic impact is diminishing in the United States, its long-term influence on supply chains and the labor force is undeniable. The effect was the highest inflation in 40 years and increasing interest rates. As investors know, inflation is bad for stock markets because it affects earnings and depresses returns.

Beyond inflation and interest rates, other issues have made 2022 a challenging year. The Russo-Ukrainian War caused oil, grain, and vegetable oil prices to spiral upward. Additionally, China must resolve its COVID-19 problem because of less successful vaccines and poor strategies. The result has been lower economic output and global supply chain disturbances.

The year 2022 proved difficult to traverse for investors. But the dividend growth investing strategy performed reasonably well. This article discusses the three worst performing Dividend Aristocrats in 2022.

Affiliate

Take the Simply Investing Course to learn more about investing and dividends.

- Lifetime access with 27 self-paced lessons.

- Covers placing stock orders, building and tracking portfolios, when to sell, reducing fees and risk, etc.

- Learn the 12 Rule of Simply Investing

- Simply Investing Coupon Code – DIVPOWER15.

Market Overview

After two years of outperformance, tech and riskier growth stocks ended their run with a whimper. High inflation and the United States central bank’s actions reduced investors’ interest in riskier stocks and assets. Just the Energy sector had a positive return because of climbing oil and natural gas prices.

After two solid years of total returns, the tech-heavy Nasdaq-100 was down (-32.9%) in 2022. The Index is in a bear market as investors avoid risk.

The Dow Jones Industrial Average (DJIA) fell (-8.9%) in 2022, better than the other main indices. Stocks in the Energy, Consumer Defensive, and Healthcare sectors are helping the Dow outperform. Specifically, Chevron (CVX) was up +58.5%, Merck (MRK) gained +49.4%, and Travelers Companies (TRV) rose +22.4%.

The S&P 500 Index did better than the Nasdaq-100 but worse than the Dow 30 at (-18.3%). This performance is worse than in 2020 and 2021. Mega-cap tech stocks that led in 2020 and 2021 struggled all year, but previously, out-of-favor sectors and stocks came to the forefront. For instance, Exxon Mobil (XOM) and Chevron (CVX) performed well.

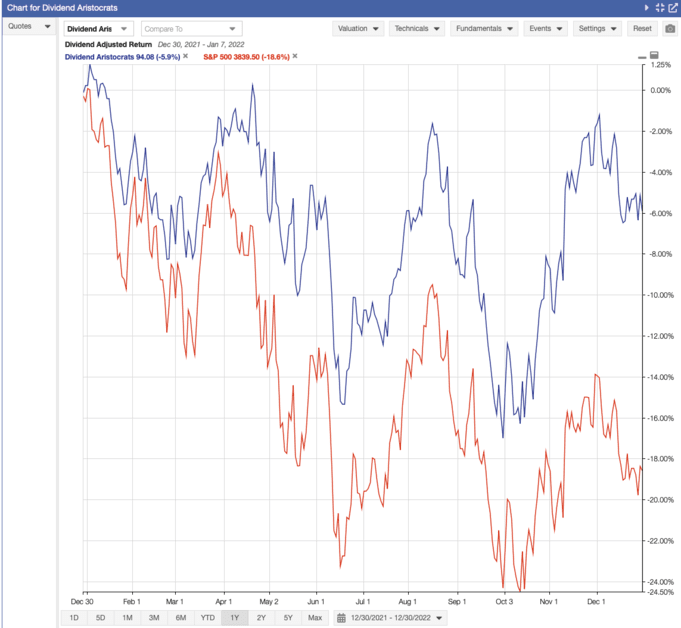

The Dividend Aristocrats 2022 performed relatively well compared to other indices. The group was still down at (-5.6%) with dividends reinvested, as seen in the chart from Stock Rover*. The Aristocrats did better than the Nasdaq-100, Dow 30, Russell 2000 (-20.5%), and the S&P 500 Index.

Last Year’s Worst Performers

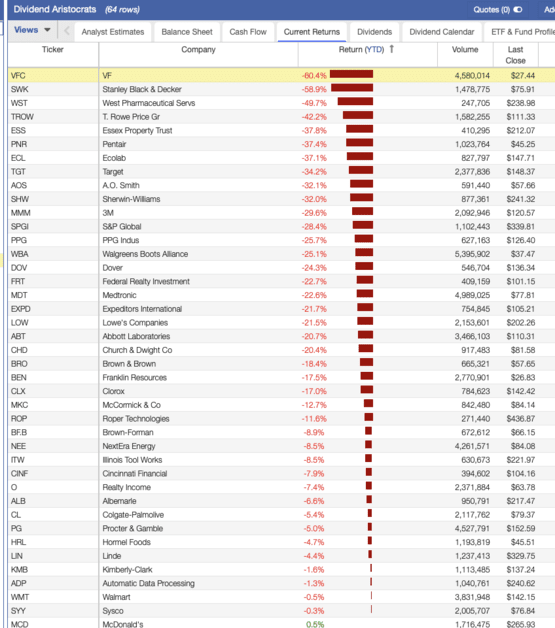

The three worst performing Dividend Aristocrats in 2021 were V.F. Corporation (VFC), Clorox (CLX), and Medtronic (MDT). In 2022, all three had negative returns, with VFC down a whopping (-60.4%).

The Dividend Aristocrats Dropped Three and Added Three

There were 65 Dividend Aristocrats at the end of 2021, and there are 64 Dividend Aristocrats at the end of 2022. Leggett & Platt (LEG) was dropped from the S&P 500 Index. In January 2022, Brown & Brown (BRO) and Church & Dwight (CHD) were added to the list. But AT&T (T) cut the dividend and was removed from the list. In March 2022, People’s United Financial (PBCT) was dropped because it was acquired by M&T Bank (MTB).

3 Worst Performing Dividend Aristocrat Stocks in 2022

So, after considering these changes, the three worst performing Dividend Aristocrat Stocks in 2022 were: V.F. Corporation (VFC) at (-60.4%), Stanley Black & Decker (SWK) at (-58.9%), and West Pharmaceutical Services (WST) at (-49.7%), based on our watch list in Stock Rover*.

VFC’s Terrible Year

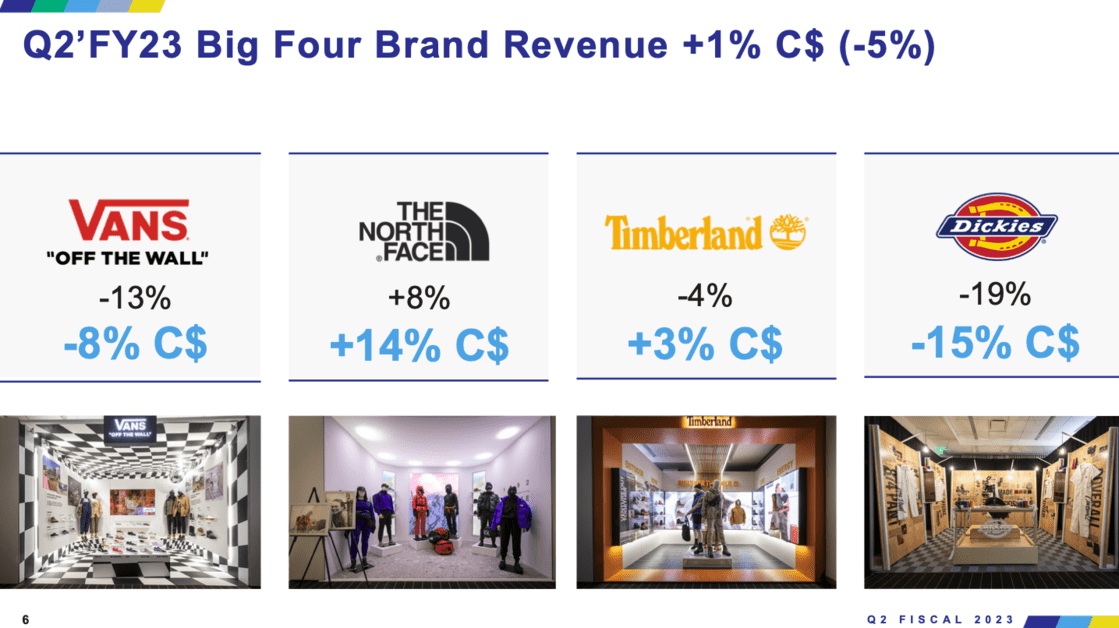

The company was founded in 1899 and was formerly known as Vanity Fair mills until 1969. Today, the V.F. Corporation is a global apparel and footwear company. The company’s 13 brands are categorized into Outdoor, Active, and Work. The big four brands are North Face, Timberland, Vans, and Dickies. Other brands include Smartwool, Icebreaker, Altra, Supreme, Kipling, Napapijri, Eastpak, and JanSport. The firm has about 55% of the U.S. backpack market.VFC sells its apparel through department stores, specialty stores, chain stores, and increasingly direct-to-customer (DTC).

In the past several years, VFC has reshaped its portfolio of brands by separating smaller and non-core ones. The company also divested its jeans business into a separate company, Kontoor Brands (KTB). It is now looking at the sale of the Jansport business.

Total revenue was $11,842 million in the fiscal year 2022 and $11,791 million in the last twelve months.

VFC’s strength is its scale and ability to take small brands and grow them through better marketing and distribution. In addition, the company continuously reshapes its product portfolio, as seen by exiting jeans and buying Supreme.

The firm is faced with substantial headwinds impacting its supply chain. Also, COVID-19 is affecting sales in China, while the European business is slowing. Unfavorable foreign exchange, weak consumer sentiment, and high inventories are also factors. In addition, VFC issued a warning about inventories and the promotional environment.

Therefore, the stock was punished and down more than 60% in 2022. VFC is trading at prices last seen in 2011, and the dividend yield has soared to more than 7%. On the plus side, the company is now a Dividend King.

V.F. Corporation is worth tracking, but investors should be prepared for volatility. It may be some time before inflation tapers and consumers are more confident buying casual clothing. The dividend safety is acceptable, but it bears watching.

Related Articles About V.F. Corporation (VFC) on Dividend Power

Stanley Black & Decker Demand Is Lower

Stanley Black & Decker is a worldwide leader in hand tools, power tools, and outdoor equipment., It is also a major player in industrial engineered fasteners and infrastructure. The company owns iconic brands like Stanley, DeWalt, Craftsman, Black+Decker, Cub Cadet, etc. Stanley sold its security business in 2022 to Securitas.

Total revenue was $15,617 million in the fiscal year 2021 and $17,278 million in the last twelve months.

The 150+-year-old company continues to maintain its lead through acquisitions and innovation in its core brands. For example, the 2017 acquisition of Craftsman helped drive the top and bottom lines. Moreover, the company’s brands have extensive distribution and sales channels. Hence, the firm operates in a reinforcing cycle maintaining its market leadership.

Stanley Black & Decker is struggling because of inflation and rising interest rates. In addition, the poor macroeconomic environment affects the housing and commercial real estate market, impacting demand. The company benefitted during the COVID-19 pandemic as people staying at home spent on home improvement and outdoor projects facilitated by the federal government’s largesse. But a return to more normal habits and the removal of federal stimulus has caused the demand to weaken and affected margins. On a positive note, the Industrial segment is doing well.

Thus, the stock price has been hammered and is down nearly 60% YTD. But the decline is likely overdone. The stock is trading at almost a decade low. In addition, the dividend yield is the highest since 2008, during the subprime mortgage crisis. Investors know of the company because it has one of the longest dividend streaks at 146 years and has increased the dividend for 55 consecutive years.

Stanley Black & Decker is worth looking at because of its market leadership and dividend history. Granted, interest rates are trending higher, which portends a poor housing market, but the firm had faced challenges before and recovered. Moreover, the conservative payout ratio of about 28% suggests the dividend should be okay. The stock is not only in the list of worst performing Dividend Aristocrats in 2022 but also the worst performing Dividend Kings in 2022.

Headwinds for West Pharmaceutical Services

West Pharmaceutical Services (WST) is probably one of the least well-known Dividend Aristocrats. But the nearly 100-year-old company is a major player in producing containment and delivery systems for injectable drugs and products. The company sells proprietary, custom, and contract solutions. Reportedly, West has about 70% market share in injectables and even more for biologics.

Total revenue was $2,832 million in the fiscal year 2021 and $2,909 million in the last twelve months.

West missed estimates with declining revenue and earnings per share. Even worse, from the market’s standpoint, West lowered its outlook. Also, foreign exchange headwinds are taking a toll. The stock price was overvalued and trading at an elevated P/E ratio before the earnings announcement. Consequently, the stock price plummeted by 19%.

West’s market leadership, intellectual portfolio, manufacturing, scale, and cost efficiencies make it a desirable stock. Moreover, dividend safety is outstanding, with a low payout ratio and no debt. However, West stock is only for some because the dividend yield is low and the stock price volatile.

Disclosure: Long WST

Related Articles on Dividend Power

Prior Year Worst Performing Dividend Aristocrats

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.