By now, you know that nearly everything in this world has costs. If you want to buy that brand new phone or that car, it will cost you money. Perhaps you want to start learning about woodworking? That will cost you time. But what does it cost to take advantage of a beneficial situation? Are you possibly missing out on something to do something else? In this post, I’ll be exploring the cost of opportunity, what it is, and what it means to you.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

What is Opportunity Cost?

Simply put, opportunity cost is the value difference in doing one thing versus doing another. An easily conceivable example of this is the cost of your daily coffee. On the one hand, you can drive to a Starbucks coffee shop and buy a cup of coffee of your favorite blend. On the other hand, you’ll spend, on average, about $3.77 if you do this. If the coffee you like is a bit fancier, you’ll obviously pay more.

How much would it cost for you to make your coffee at home instead? First, you’ll need a machine which will cost you a certain amount upfront. Then, you’ll need to supply your coffee. However, a cup of coffee made at home will be significantly less per cup, even with the fanciest of drinks. Even the widely available single-origin and ethically sourced coffees will cost only $1 a cup, at the most, when brewed at home. All it takes is a little time and forethought.

Because of the upfront cost of the ingredients and the machine, it will take a little bit of time for the cost of making your daily coffee at home to be less than the cost of buying it at the coffee shop every day. However, there is no looking back; it will always cost less to make it at home than to buy it out. By buying coffee out every day instead of making it yourself, you give up some of your money for convenience.

More Than Just Money

But this is just the basics of the cost difference. By making it at home versus getting it at the coffee shop, you might be spending a little more time in the morning preparing your coffee. What else could you be doing with the time that you are now spending making coffee? This time is a lost opportunity to be doing something else. If that time had been spent watching TV, then you are, arguably, still in the hole regarding the cost of your coffee. However, if you spend that time reading charts for possible day trading opportunities, the time you are spending to make your coffee and save a few dollars a day might be costing you more in trading.

On the flip side, if you are spending the money on the convenience of getting your coffee at the coffee shop, that’s money you aren’t using to pay off debts or increase your investments. This convenience (and better taste, let’s face it) of getting your favorite coffee drink at the shop is costing you the opportunity to get out of debt faster or retire earlier.

This fact is the fundamental basis of David Bach’s Latte Factor. Small amounts of money, compounded over time, can add up to vast sums over time. That $2.77 you spend extra today on your latte could be worth over $285,000 in 40 years. That’s quite a bit of opportunity to throw away for a quick and convenient caffeine hit today.

What Are Some Other Examples?

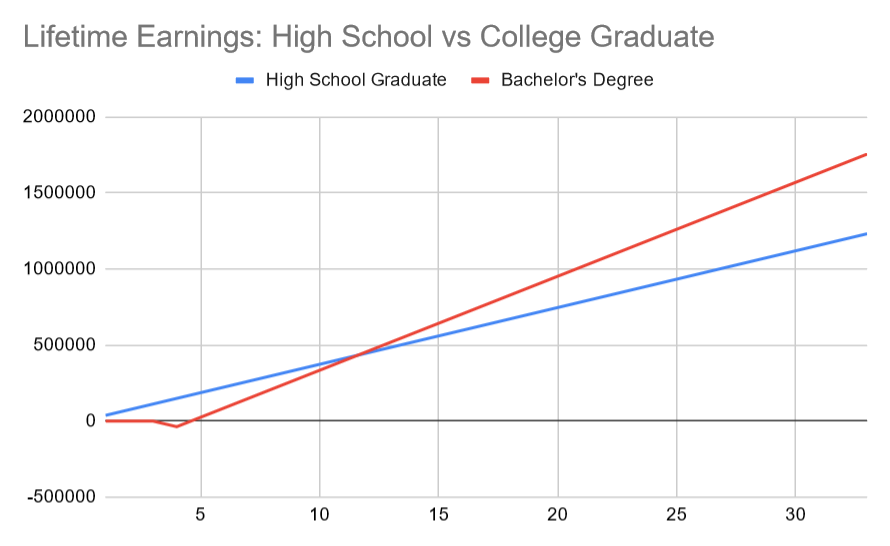

Another classic example of the cost of opportunity is attending college. Nearly everyone knows that it costs money to attend college and you may even need student loans. Additionally, while attending college, you are delaying the amount of time before you start to generate a full-time salary. Assuming you are going to college for a four-year degree, that’s four more years of you not making a full-time salary.

However, it’s also no secret that your earning potential is now higher than if you hadn’t attended college at all after those four years despite the cost of college. In fact, even after accounting for student loans, the median college graduate will surpass the median non-college graduate in just 12 years.

The high school graduate that jumps right into the workforce is getting more income four years quicker than the college graduate. However, they are paying for this by the lost opportunity of making more money with a college degree. As seen above, over the long term, the cost of this opportunity can be staggering.

How About the Opportunity Cost of Opportunity Itself?

When was the last time you heard someone tell a story that went like this:

“So, there I was, doing everything the same as I always have, and this awesome thing happened.”

Never; no one has ever told a story like that. Every story where something extraordinary happens starts with the storyteller doing something they wouldn’t normally do. The cost of having something incredible happen to you (and thus, having a great story to tell) is to get outside your comfort zone.

Whether you realize it or not, several other aspects of your life follow this same concept. Should you start that business, or should you keep working your current job? If you start that business, you might be giving up the opportunity for a steady paycheck but gaining a more fulfilling career and lucrative income. This path will take some hard work and dedication, though. Are you willing to pay that price of discomfort and uncertainty now for the potential of a more significant opportunity later?

Or, how about switching jobs? Are you willing to step outside of the BS you know at your current position, knowing that you might find even more BS at your new job? Will, what you gain in salary and reduction in stress outweigh the potential opportunities you may have had at your previous job?

Measuring the Cost of Opportunity

While measuring the opportunity cost of a financial decision can be relatively straightforward, it is much more challenging to estimate the cost of an opportunity itself. How much will it cost to get out of your comfort zone now and start that new job or business? And how much will you lose in the long term by not doing that? These are tough questions to answer. This tradeoff is what makes measuring the cost of opportunity so hard.

But remember, no good story starts with someone doing the same thing they’ve always done.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Michael Reed

Mike from Second Gen Finance is an early Millennial who identifies as a Generation X'er. He is a software developer by trade, but in January of 2020, he resolved to start reading more often. This change was when he began to learn more about finance and investing. Many of the lessons he learned while reading these books he lamented not having known earlier. Although he and his wife were doing well financially, they had been pretty much winging it and doing all the things "you're supposed to do."

As he read more and more, he realized that if they had been doing these things for longer, they’d be even better off financially. He wanted to be sure that all that he had freshly learned about money would be passed down to his young daughter so that she would be better off than her parents.

Second Gen Finance was created to organize these ideas and lessons and help build the foundation for generational wealth.