As a dividend growth investor, I love Dividend Champions. These are stocks that have paid a growing dividend for 25-years or more. Thomson Reuters is a Dividend Champion. The stock is also one of the Canadian Dividend Aristocrats. Thomson Reuters is a Canadian company that trades on the Toronto Stock Exchange or ‘TSE’ and also trades on the New York Stock Exchange or ‘NYSE’. At the right price, the stock is probably a good addition to many dividend growth portfolios. The market downturn resulting from COVID-19 caused the stock price to drop, but it has recovered somewhat since then. The current dividend yield is roughly 2.0%, which is higher than the broader market average. Dividend growth investors may want to research this stock further.

Affiliate

Take the Simply Investing Course to learn more about investing and dividends.

- Lifetime access with 27 self-paced lessons.

- Covers placing stock orders, building and tracking portfolios, when to sell, reducing fees and risk, etc.

- Learn the 12 Rule of Simply Investing

- Simply Investing Coupon Code – DIVPOWER15.

Overview of Thomson Reuters

Thomson Reuter Corporation (TRI) is media, content, and data company that traces its founding back to 1934 in Canada and 1851 in London. The company in its current form is the result of a $17.6 billion merger between Thomson of Canada and Reuters Group of the U.K. in 2008. More recently, in 2018, the company divested its Finance and Risk business forming Refinitv in exchange for $17 billion. Thomson owns a 45% stake of Refinitv and The Blackstone Group (BX) owns the other 55%. In 2019, Thomson Reuters agreed to exchange the 45% stake in Refinitiv that it owns for a 15% stake in the London Stock Exchange Group subject to regulatory approvals. Total revenue was approximately $5,906 million in 2019.

Today, Thomson Reuters operates in five business segments: Corporates (22% of revenue), Legal Professionals (41% of revenue), Tax & Accounting Professionals (14% of revenue), Reuters News (11% of revenue), and Global Print (12% of revenue). The company will have about $5.9 billion in revenue in 2020 (before COVID-19 impacts). Thomson Reuters is the market leader in the global legal market segment, and the market leader in corporate legal and tax solutions in the U.S., and the tax market segment in the U.S.

Note that the company is controlled by the Thomson family of Canada through their investing vehicle, Woodbridge Company Limited. They control approximately 65% of the company’s common shares. The family holds the chairman position of Thomson Reuters.

Thomson Reuters’ Dividend and Safety

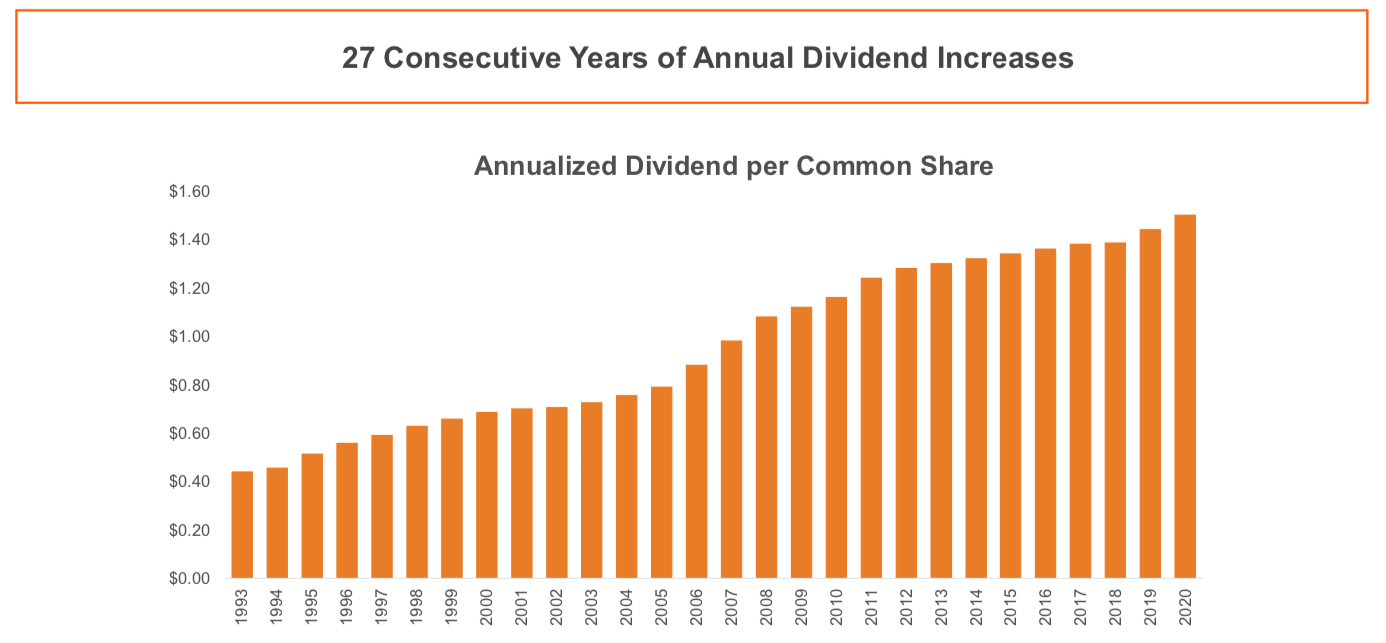

Thomson Reuters is a Dividend Champion and a Canadian Dividend Aristocrat. The company has paid a growing dividend for 27 consecutive years since 1993. The regular quarterly cash dividend has increased from $0.08 per share in 1993 to $1.52 per share in 2020. This gives a current dividend yield of approximately 2.0%, which is not bad compared to S&P 500s’ current average dividend yield of about 1.75% as of this writing.

Source: Thomson Reuters Investor Booklet Winter 2020

Thomson Rueters’ dividend safety metrics have historically been somewhat volatile due to special items. They have also worsened recently due to the divestment and subsequent loss of revenue and lower earnings, and COVID-19.

Looking forward, consensus 2020 earnings per share is $1.82. The forward dividend is $1.52 per share. This gives a payout ratio of approximately 83.5%. This value is a bit high for my l;iking and it is greater than my target value of 65% or lower. However, revenue and earnings are likely to be depressed in 2020 due to COVID-19. Further, Thomson Reuters is adding to revenue through bolt-on acquisitions. This should improve the payout ratio with time as these acquisitions grow and add to the bottom-line.

On a free cash flow basis, the dividend is also safe. The company is guiding for roughly $1 billion in free cash flow. This is down from guidance of $1.2 billion in FCF earlier in the year due to COVID-19. The dividend costs about $760 million annually ($1.52 x 500 million shares). This gives a dividend-to-FCF ratio of about 76%. This is an OK value but higher than my target value of 70%. The long-range target for Thomson Reuters is to pay 50% – 60% of free cash flow as the dividend. I used TIKR* for the data in this analysis.

The dividend is also seemingly safe from the perspective of debt. At end of the most recent quarter, Thomson Reuters had outstanding debt of $3.8 billion off set by cash on hand and short-term investments of $1,358 million. The leverage ratio is conservative at about 2.0X and interest coverage is over 5X. No debt is due until 2023 adding to the good picture for dividend safety from the perspective of debt.

Overall, the combination of the divesture, restructuring, and COVID-19 has likely made the dividend safety metrics somewhat worse the desired. However, Thomson Reuters has positioned itself in higher growth areas and is forecasting organic growth supplemented by bolt-on M&A.

Thomson Reuters’ Valuation

Is Thomson Reuters overvalued undervalued? The stock is currently trading at a forward earnings multiple of about 42.5X. This is higher than the average of the S&P 500, which is trading at 29.4 as of this writing. So, Thomson Reuters is overvalued at the moment. However, some of this elevated valuation is due to lower consensus forward earnings per share due to COVID-19. The high earnings multiple is also probably due to limited float that is also contributing to overvaluation. Recall that the Thomson family controls about 65% of the common shares. So, there is limited amount of stock that trades on a daily basis for a company of its size.

Final Thoughts on Thomson Reuters – A Dividend Champion

Thomson Reuters’ stock price dropped to about $52 per share at the depths of the downturn caused by COVID-19, which was probably a good entry point. The stock is arguably under the radar as dividend growth stock. For one, it is a Canadian company, which likely reduces interest for U.S. investors. But Thomson Reuters does trade on the NYSE, the company pays a regular quarterly cash dividend, and it is a Dividend Champion. I expect that the dividend will continue to grow in the future but at a slower rate. The company has seemingly prioritized share repurchases and M&A at the moment. With that said, dividend growth investors may want to research this stock further and keep an eye on it for a better entry point.

If you are looking for a good newsletter that tracks and analyzes many Canadian stocks sign up for the Simply Investing Newsletter*.

A version of this article first appeared as a guest post on the MoneyMaaster blog.

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.