Essential Properties Realty Trust, Inc. (EPRT): Undervalued REIT and 4.3% Yield. If you are looking for an income with high dividend growth stock that is undervalued, you will be very interested in our next undervalued Real Estate Investment Trust (REIT). The industry was beaten down in 2022 because of higher interest rates and recession fears. This decline provides long-term investors with great opportunities in the Real Estate sector if they are willing to hold on through the higher rate interest environment.

Essential Properties Realty Trust, Inc. (EPRT) is one company I have had my eye on, and it looks like an excellent company to pick up some shares. As a matter of fact, I bought shares in this price range as it is near a support level of around $20. The chart below shows that the $20 to $21 level was a support and resistance level at least six different times. The stock is trading at $25.39 per share as of this writing. Even though it is higher than the $20 per share support, the stock is still at a very attractive price. Thus, EPRT stock looks like it is at an excellent price to pick up shares. In this article, we will determine if the company is undervalued and deserving of our hard earn money.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

Overview of Essential Properties Realty Trust, Inc.

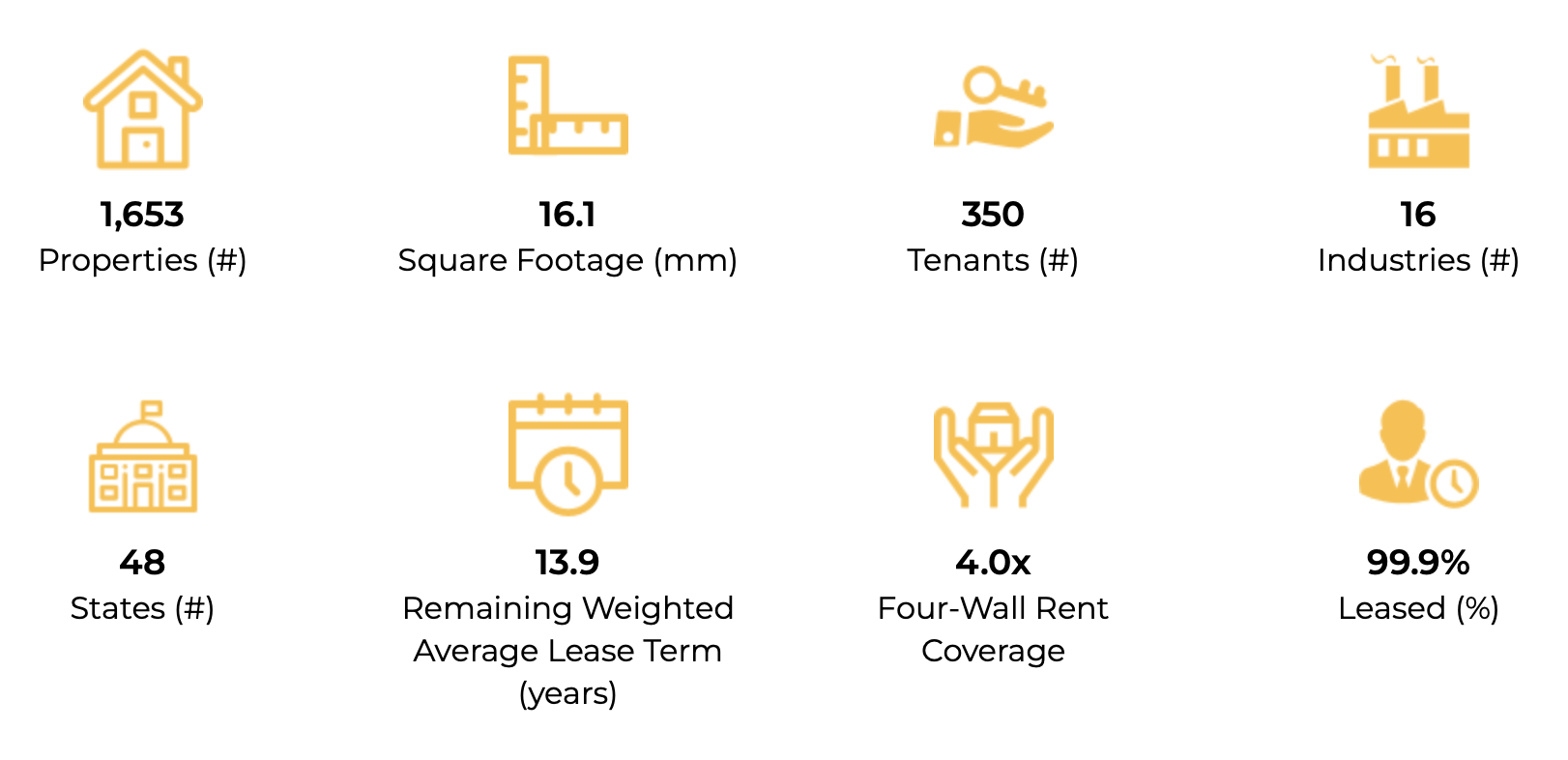

Essential Properties Realty Trust Inc is a real estate investment trust that acquires, owns, and manages single-tenant properties leased on a long-term basis to middle-market companies that operate service-oriented or experience-based businesses. Some businesses include restaurants, car washes, automotive services, medical services, convenience stores, entertainment, health & fitness, and early childhood education. The company owns 1,572 properties spanning 14.8 million square feet. There are 329 diverse tenants across 16 industries in 48 states. The properties are 99.9% leased. The diversified REIT trades on the NYSE under the ticker symbol EPRT. The Trust has a market capitalization of $3.6 billion and is headquartered in Princeton, New Jersey.

EPRT’s stock price was down 22.9% since its all-time high in September 2021. The main driver of the stock price decrease has nothing to do with the company itself, as earnings are expected to grow 14% in 2022 and another 4% in 2023. Instead, it concerns the increasing interest rates affecting all REIT stocks. Also, the stock was very much overvalued in September 2021.

The current stock price of $25.39 (as of this writing) is right at the mid-to-high end of the 52-week range, between $18.88 and $26.75 per share. Thus, Essential Property Realty Trust looks like a stock in the right place to buy up shares where both the 52-week range and near support the line. Also, the REIT is reasonably valued.

EPRT Dividend History, Growth, and Yield

We will look at Essential Properties Realty Trust’s dividend history, growth, and yield. We will then determine if it’s still a good buy at current prices.

In this case, EPRT stock has increased its dividend for three consecutive years. EPRT’s most recent dividend increase was 2%, announced in December 2022. Investors should expect another increase at the end of 2023.

Dividend Growth

Additionally, according to Portfolio Insight*, EPRT has a three-year dividend growth rate of about 6.9%, which is admirable considering how fast inflation increased last year and this year. Additionally, since this is a new company that was listed in 2019, there is not much more information on the dividend history for the company.

Something significant to note is that EPRT continued to pay its dividend during the most challenging period in the last 100 years. Many businesses and industries cut or suspended their dividend payments during the COVID-19 pandemic. However, unlike many other REITs, EPRT continued to pay out its dividend and increased them. That is very noteworthy. This fact alone leads me to believe in the strength of the company and the fact that management is focused and committed to the dividend policy.

Dividend Yield

The company has an excellent dividend yield of approximately 4.3%, more than double the average dividend yield of the S&P 500 Index. This dividend yield is a respectable initial yield for dividend growth-driven investors. And it may be an excellent stock for income-driven investors who want a 4.5% yield or higher. However, with the company’s recent dividend increase rate, I can see over 5% yield-on-cost (YOC) in the next 3 to 5 years.

EPRT’s current dividend yield is higher than its 4-year average dividend yield of ~4.0%. I like to look at this metric because it gives me a good idea if a company I am researching is undervalued or overvalued based on the current and 5-year average yield. Stock price and dividend yield are inversely related. If the stock price increases, the dividend yield decreases, and vice versa.

Dividend Safety

Is the current dividend safe? This metric is critical to look at as a dividend growth investor. Undervalued dividend stocks sometimes present a “value trap,” and the stock price can continue to decline.

We must look at two critical metrics to determine if the dividend payments are safe yearly. The first one is Funds from Operation per share (FFO), and then we must look into Free Cash Flow (FCF) or Operating Cash Flow (OCF) per share.

Analysts predict that Essential Property Realty Trust stock will earn an FFO of about $1.64 per share for the fiscal year (FY) 2023. Analysts are 67% accurate when forecasting EPRT’s future FFO. However, the company misses these estimates 33% of the time. In addition, the company is expected to pay out $1.11 per share in dividends for the entire year. These numbers give a payout ratio of approximately 67.9% based on FFO, a conservative value, leaving the company with much room to continue to grow its dividend. Most REITs tend to have a payout ratio of over 80%.

I am excited by having an 80% or lower dividend coverage with a dividend yield of ~4.3% with future growth. At this point, it will allow the company to continue to grow its dividend at a mid-single-digit rate without sacrificing dividend safety. In addition, EPRT has a dividend payout ratio of 68% on an free cash flow (FCF) basis. Thus, the dividend is well covered by both FFO and FCF.

EPRT Revenue and Earnings Growth / Balance Sheet Strength

We will now look at how well EPRT performed and grew its FFO and revenue throughout the years. When valuing a company, these two metrics are at the top of my list to study. Without revenue growth, a company can’t have sustainable FFO growth and continue paying a growing dividend.

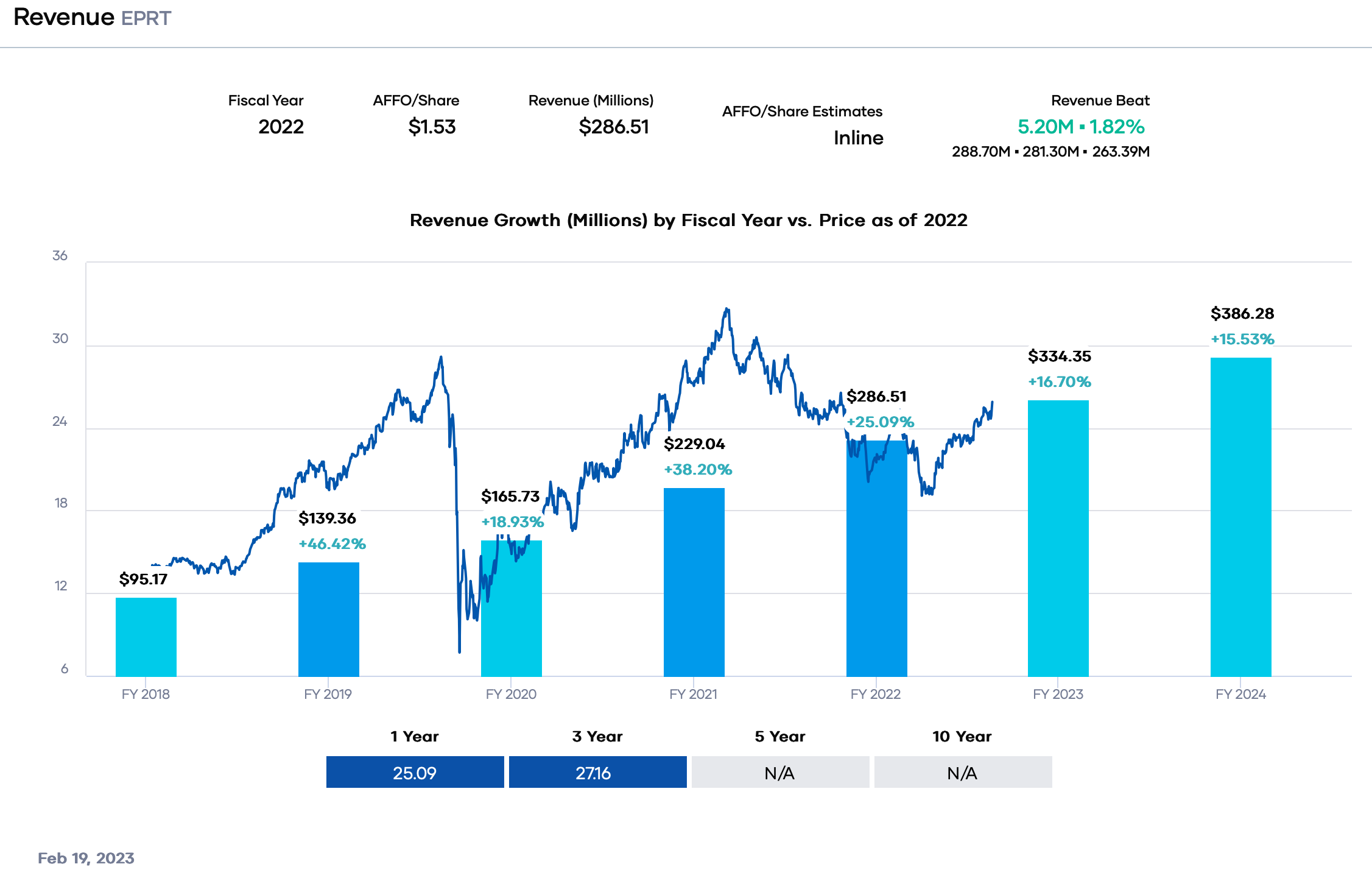

EPRT’s revenue has been growing outstanding at a compound annual growth rate (CAGR) of about 42.2% for the past four years, according to Portfolio Insight*. Net income, however, did much better with a CAGR of ~97.4% over the same four-year period. However, FFO has grown 7.6% annually for the past four years.

Since revenue, net income, and FFO did have good growth over the years, we will determine if this stock is attractive based on its valuation and dividend yield. We will talk about the company’s valuation later in this article. In the meantime, analysts predict that the company will grow FFO at a 6% rate over the next five years.

Last year’s FFO increased from $1.11 per share in FY2020 to $1.34 per share for FY2021, an increase of 21% and excellent percentage, considering the challenging two years because of the COVID-19 pandemic. Additionally, analysts expect EPRT stock to make an FFO of $1.53 per share for the fiscal year 2022, which would be a ~14% increase compared to FY2021. So again, this is something I like to see that future earnings continue to grow.

The company has a solid balance sheet. EPRT does not have an S&P Global credit rating. However, the company has a debt-to-equity ratio of 0.5, which is a solid ratio. Thus, the company has a stable balance sheet to overcome significant economic downturns like the COVID-19 pandemic last two years, adding to the dividend safety.

EPRT Stock’s Competitive Advantage

Management execution of adding new properties, either through acquisition or construction of new properties, is the REIT’s most significant competitive advantage as we advance. Thus, the efficiency to scale is its most crucial growth driver. Also, because of the lower debt than most REITs, EPRT can leverage finances to buy up distressed properties that can be bought at a higher cap rate.

Moreover, Essential Property Realty Trust puts its concentrations on sale-leasebacks with bank-dependent, middle-market firms. This gives the company negotiating leverage to obtain many landlord-friendly lease terms. For example, unit-level and property-level financial reporting and long lease durations.

However, there are still risks with an investment in EPRT stock. For example, if there is a recession, this can continue to lower the stock price as it did most stocks in the Great Recession and during the COVID-19 pandemic, which saw prices decrease by 64%.

Valuation for Essential Property Realty Trust

One of the valuation metrics that I like to look for is the dividend yield compared to the past few years’ histories. I also want to look for a lower price-to-earnings (P/FFO) ratio based on the past 5-year or 10-year average. Lastly, I like to use the Dividend Discount Model (DDM). I use a DDM analysis because a business ultimately equals the sum of the future cash flow that that business can provide.

Let’s first look at the P/FFO ratio. EPRT has a P/FFO ratio of ~15.9X based on FY 2023 FFO of $1.65 per share. The P/FFO multiple is excellent compared to the 4-year P/FFO average of 19.5X. If EPRT were to revert back to a P/FFO of 19.5X, we would obtain a price of $31.14 per share.

Now let’s look at the dividend yield. As I mentioned, the dividend yield currently is 4.3%. There is good upside potential as EPRT’s 4-year dividend yield average is ~4.0%. For example, if EPRT were to return to its dividend yield 4-year average, the price target would be $27.00.

The last item I like to look at to determine a fair price is the DDM analysis. I factored in a 9% discount rate and a long-term dividend growth rate of 5.0%. I use a 9% discount rate because of the higher-than-normal current dividend yield. In addition, the projected dividend growth rate is conservative and lower than its past 4-year average. These assumptions give a fair price target of approximately $28.35 per share.

If we average the three fair price targets of $31.14, $27.00, and $28.35, we obtain a reasonable, fair price of $28.84 per share, giving EPRT a possible upside of 13.5% from the current price of $25.39 share price.

Final Thoughts on Essential Properties Realty Trust (EPRT)

Essential Properties Realty Trust, Inc. is a high-quality company that should meet most investors’ requirements. The company has a market-beating 4.3% yield and a dividend growth history. Past earnings growth has been excellent and occupancy rates are high. However, past performance does not mean it will be the same in the future. However, at the current price, the stock looks attractive.

Disclosure: Long shares of EPRT

You can also read Essex Property Trust (ESS): Undervalued REIT by the same author.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.