Investing in dividend growth stocks is a slow and steady way to build wealth. Stocks characterized by this investing style will raise the dividend annually but also typically experience a rising share price. This makes for a powerful combination that adds to wealth annually.

We highlight three companies with high dividend growth rates over five and ten years. Two of the three equities are Dividend Kings, while one is a Dividend Contender. The firms clearly prioritize investors. We discuss Lowe’s Companies (LOW), UFP Industries (UFPI), and Nordson Corporation (NDSN).

Affiliate

Try the Simply Investing Report & Analysis Platform to pick the best stocks.

- Analyzes 6,000+ stocks with 120 metrics and financial data.

- Tracking portfolios, watch lists, dividend income, e-mail alerts, undervalued and overvalued stocks, etc.

- List of top ranked stocks based on the 12 Rules of Simply Investing.

- Simply Investing Coupon Code – DIVPOWER15.

3 High Dividend Growth Stocks

Lowe’s Companies

Lowe’s Companies is one of the leading high dividend growth stocks. Some people find this fact surprising because the firm is also a 2024 Dividend King, a company that has increased its dividend for 50+ years and is over 100 years old. A mature company usually does not have high dividend growth.

Lowe’s is the No. 2 firm in the home improvement market, behind Home Depot (HD). It sells products and services for home remodeling, repair, construction, and maintenance. This includes paint, electrical switches, fixtures, lumber, flooring, plumbing, etc. It focuses on national and private brands. Lowe’s also offers installation services through its network of independent contractors. The result is more than $86.4 billion in revenue in fiscal year 2024.

Lowe’s has been successful because it locates stores conveniently where demand is presumably high. Older homes need upkeep, remodeling, and renovation. New homes need paint, landscaping, and personal touches. Revenue and earnings per share typically increase annually by selling more items, raising prices, and opening more stores. Lowe’s operates over 1740 stores in the United States, leaving room for expansion in the country and, importantly, internationally.

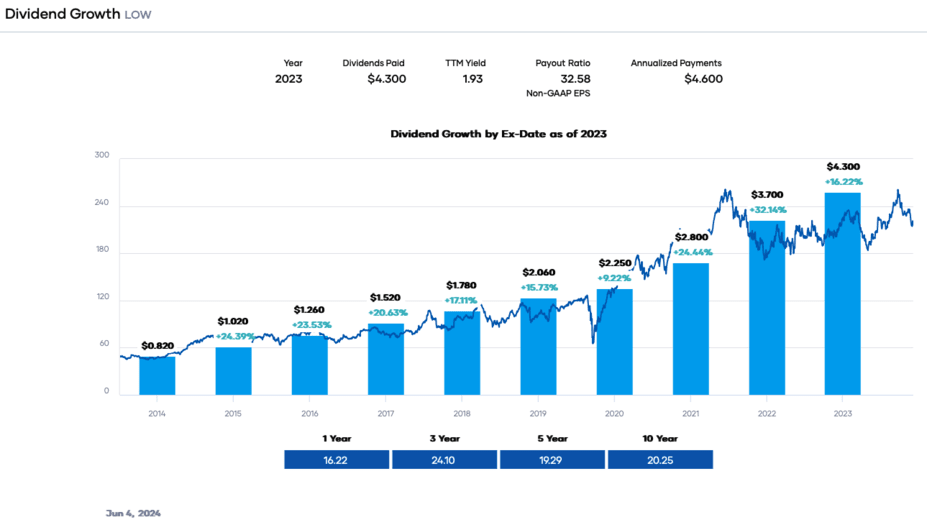

Lowe’s is a favorite with investors when it comes to dividend growth combined with price appreciation. It is a Dividend King with a 62-year streak of yearly increases, one of the few companies reaching the six-decade threshold. It last raised the dividend at the end of May 2023. Investors should expect another increase soon. According to Portfolio Insight, the dividend growth rate has been roughly 20% on average in the past five years and decade. We expect a lower increase this year because EPS may decline, but we anticipate higher growth rates when revenue and earnings per share rebound.

The share price is slightly down in 2024 because of a challenging economic environment. The dividend yield is nearly 2%, more than the 5-year average of ~1.8%. This yield is backed by a modest payout ratio of approximately 33%. Free cash flow of $8,330 million exceeds the dividend distribution requirement of $2,531 million in the last twelve months. The ‘A+’ dividend quality grade and the BBB+/Baa1, lower-medium investment grade credit ratings boost dividend safety.

The challenging business environment and impact on Lowe’s has caused the share price to remain relatively flat this year. Consequently, it trades at a price-to-earnings ratio of ~18.5X, a reasonable value relative to the long-term average. Although not deeply underpriced, it does fit Charlie Munger’s advice, “A great business at a fair price is superior to a fair business at a great price.” Consensus earnings are anticipated to fall in 2024 and possibly 2025, but the firm should return to growth as inflation and interest rates fall. We view Lowe’s as a long-term buy.

UFP Industries

UFP Industries is a much smaller company, but its dividend growth rate is even more impressive than Lowe’s. Most people probably have not heard about the business. It has a nearly 70-year history selling wood and other products to the housing industry. It was previously known as Universal Forest Products. Today, the business operates in eight countries through three segments: UFP Retail Solutions, UFP Construction, and UFP Packaging. Total revenue reached $7,218 million in 2023.

The company has grown organically and recently through numerous tuck-in acquisitions. It has recently added PalletOne, CedarPoly, and DWP, expanding UFPI’s packaging offerings. These three acquisitions are in addition to ten earlier ones. The company lists acquisitions as a priority in its capital allocation strategy to contribute half its total annual sales growth.

UFPI is on the list of Dividend Contenders with a 12-year streak of increases. The share price has declined this year because of lower sales. Revenue peaked in 2022 at over $9.6 billion. The dividend yield is only 1.1%, slightly greater than the 5-year average. The dividend growth rate is outstanding at over 25% in the trailing five years and almost that value in the last decade. The meager payout ratio of ~13.6% indicates more increases to come. However, because revenue and earnings are expected to decline in 2024 and 2025, the increases may be subdued until the trend reverses.

The payout ratio suggests that the dividend safety is simply outstanding. Free cash flow of $780 million covers the dividend requirement of $68 million in 2023. UFPI also has a BBB+/Baa1 lower-medium investment credit rating. The balance sheet is rock solid with a net cash position.

UFPI’s struggling share price makes it attractive because it trades only at 15.6 times forward earnings. This is a reasonable value within the five-and ten-year ranges. As a result, we view this equity as a buy.

Nordson

Nordson Corporation is another Dividend King. However, it is not well-known even though the market capitalization exceeds $15 billion. Besides being a member of the Dividend Kings, the equity is known for its higher dividend growth rate. Nordson is third in our article about high dividend growth stocks.

The company designs, manufactures, and sells systems and products to dispense fluids, like adhesives, coatings, polymers, sealants, etc. It has three operating segments: Industrial Precision Solutions, Medical and Fluid Solutions, and Advanced Technology Solutions. Total revenue was $2,651 million in the last twelve months.

The business grows organically by adding customers and developing new technologies to stay ahead of competitors. It also periodically expands through M&A. Nordson most recently purchased CyberOptics Corporation, which added to its semiconductor and electronics business.

Nordson has increased the dividend rapidly, and it has a 61-year streak. The trailing growth rate over the past five and ten years is roughly 15%. Moreover, the low payout ratio of 29.5% suggests many more future increases. Earnings are predicted to rise in the next three years, and we expect another solid increase in August 2024.

One negative is the low yield of 1.1%, which likely keeps this stock off an income investor’s radar. However, the value is above the 5-year average of ~1%. The modest payout ratio points to excellent dividend safety. Also, a free cash flow of $607 million easily covers the dividend payout of $154 million. Nordson earns an ‘A+’ dividend quality grade, meaning it’s in the 95th percentile of dividend-paying stocks. It also has a BBB/Baa2 lower-medium investment grade credit rating, giving greater confidence about safety.

The share price has declined about 7.5% year-to-date. However, the valuation is still at a price-to-earnings ratio of 26.1X, which is in the 5-year range. We view Nordson as a buy because of its dividend growth, safety, streak, and acceptable valuation.

Disclosure: Long LOW

A version of this post by Dividend Power originally appeared on Investor Place and was republished with permission.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.