After a downturn in late summer to early fall, the stock market reversed itself on two pieces of good news. First, inflation seems to have stabilized. Next, the United States Federal Reserve paused Federal Fund rate increases for the second consecutive meeting in a row. The combination changed investor sentiment. The Nasdaq Composite, Russell 2000, S&P 500, and Dow Jones Industrial Average have all gained in the past month. In addition, ten of the 11 sectors have positive returns.

Favorable market trends suggest that previously struggling stocks may recover, providing attractive share price appreciation, earnings growth, and dividend yields. Although many dividend stock choices exist, we prefer dividend growth stocks, especially ones with high growth rates. These companies usually have climbing revenue and earnings per share, translating to brisk gains in share price and dividend payouts. Below are three high-dividend growth stocks to choose from that can generate solid total returns.

Affiliate

Stock Rover is an award winning investment research platform.

- The site has 8,500+ stocks, 4,000 ETFs, and 40,000 mutual funds.

- Access to 650+ metrics, financial data, market news, stock and fund ratings, fair value, margin of safety, etc.

- Includes brokerage integration, portfolio tracking, rebalancing, watchlists, alerts, future income forecasts, etc.

Click here to try Stock Rover for free (14-day free trial).

3 High Dividend Growth Stocks to Choose in December 2023

Dick’s Sporting Goods

Dick’s Sporting Goods (DKS) is the largest sports and leisure retailer in America. It operates 869 stores in 47 states, of which 725 are Dick’s Sporting Goods stores, and the remainder are specialty types. The company’s success has allowed it to capture around 8% of the market share, up from 7% in 2019. Dick’s sells large national brands like Nike, Yeti, Peloton, Wilson, Ping, The North Face, Wilson, Brooks, etc. It also has an assortment of private-label brands.

Total sales were over $12,368 million in the fiscal year 2022 and $12,705 million in the past twelve months. Like most specialty retailers, Dick’s grows its market share by adding more stores and more products within its stores. The company also gains in revenue and profit by selling more items per customer. Product volumes like sneakers, athletic wear, sports equipment, etc., are climbing, and Dick’s offers a wide selection and decent pricing.

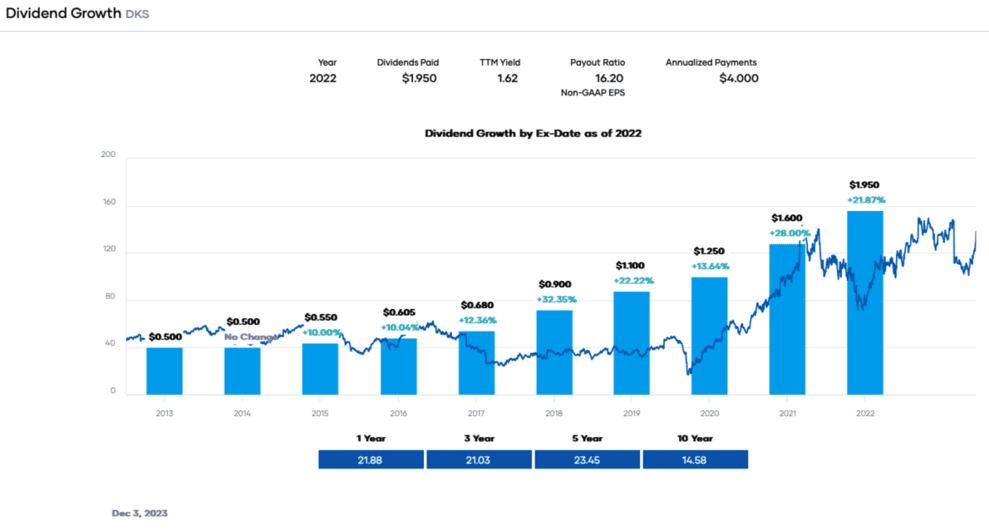

From a dividend growth perspective, the company is a current Dividend Challenger with a 9-year history of increases. The five-year growth rate is roughly 23.5% because Dick’s only commenced paying a dividend in 2013. Rising earnings per share suggest more additions to come, mainly because the payout ratio is miniscule at around 16%. The low percentage indicates solid dividend safety supported by high-interest coverage of 20X and a moderate leverage ratio of 1.2X. Moreover, the dividend quality grade is an ‘A.’

Dick’s stock price is flat for the year. However, excellent third-quarter results renewed interest in equity. The price-to-earnings ratio is low at ~9.9X, below the broader market and the five-year range. Investors are paid to wait with a 3.3% computed dividend yield. We view Dick’s as an industry consolidator.

Dollar General

Dollar General is the largest of the so-called dollar stores and it is the second high dividend growth stock on our list. Today, most items are priced at $5 or less. The retailer operates nearly 19,500 stores in all 50 states. Most stores are small at about 7,400 square feet and in towns comprising 20,000 or less. Besides the ubiquitous Dollar General stores, the retailer started the popShelf concept and has roughly 190 locations. The firm is also expanding internationally with the Mi Super Dollar stores in Northern Mexico. Dollar General has a goal of ten stores in 2023.

The current year has not been kind to Dollar General. A combination of high inflation and interest rates has stressed its core customer. As a result, the company needed to slash revenue and earnings estimates, causing the stock to plummet. The share price is down nearly 50% year-to-date. However, Dollar General grows like most retailers by selling more in its outlets and adding to its footprint. The firm’s small store size, popShelf brand, and international expansion mean future growth paths exist once inflation subsides.

The retailer is another Dividend Challenger with a nine-year streak. The trailing dividend growth level is about 27.4% during this time. Despite the recent struggles, Dollar General’s dividend payout ratio formula, a measure of safety, gives a low value of 24.5%, indicating more future increases to come. Although the net debt and leverage ratio has risen because of rapid expansion, interest coverage is still 10.5X.

Because the share price has declined almost 50%, the valuation has dropped to ~16.9X, at the lower end of the five- and ten-year ranges. Despite a weaker outlook, Dollar General is still growing, and results may improve if inflation returns to sub-2%. Investors should take a look at this stock now.

Thermo Fisher Scientific

Thermo Fischer Scientific (TMO) is the third high dividend growth stock on our list, the giant life sciences products, diagnostics, and services company. Because most customers are other businesses, the firm may not be that well-known. However, it has matured into a $188 billion market capitalization company. Thermo Fischer Scientific operates through four business segments: Life Sciences Solutions, Analytical Instruments, Specialty Diagnostics, Laboratory Products and Biopharma Services.

Thermo Fischer is snowballing through acquisitions. It has spent tens of billions completing dozens of purchases ranging from small, tuck-in ones to larger targets. Thermo Electron merged with Fischer Scientific in 2006. Since then, it has added Life Technologies Corporation for $13.6 billion, Patheon for $7.2 billion, Qiagen, PPD, and many smaller companies. Besides M&A, the firm operates in growing life science markets. We expect the top and bottom lines to grow further because of end markets and acquisitions.

The company is relatively new as a dividend stock, starting distributions in 2013 and increasing them in 2018. Consequently, Thermo Fischer is a Dividend Challenger. The past 5-year growth rate is ~14.9%. We expect the double-digit increases to continue due to the minimum payout ratio of roughly 5.2%. The company’s net debt is rising because of acquisitions, and the leverage ratio has reached 2.6X. But it has an investment-grade credit rating.

The stock typically trades at an elevated valuation between 18X and 26X. The forward P/E ratio is 21.6X in the middle of the range. Although not a deal, dividend growth investors may want to dip into this stock. Furthermore, we view Thermo Fischer as a consolidator in the life sciences industry.

Disclosure: Long DG

A version of this post by Dividend Power originally appeared on Investor Place and was republished with permission.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.