Nucor (NUE) has been one of the top-performing Dividend Aristocrats over the last two years. With the stock price per share increasing from just around $50 to over $187 in April. NUE has had a great performance, mostly driven by higher steel prices, and continued to increase its dividend during this time. Despite this the valuation is still not reflecting the intrinsic value of the business.

There is no other dividend stock that you can invest in with a 20% free cash flow (FCF) yield, that continues to grow dividends, and has a stock buyback program that will buy over 10% of the outstanding shares this year alone

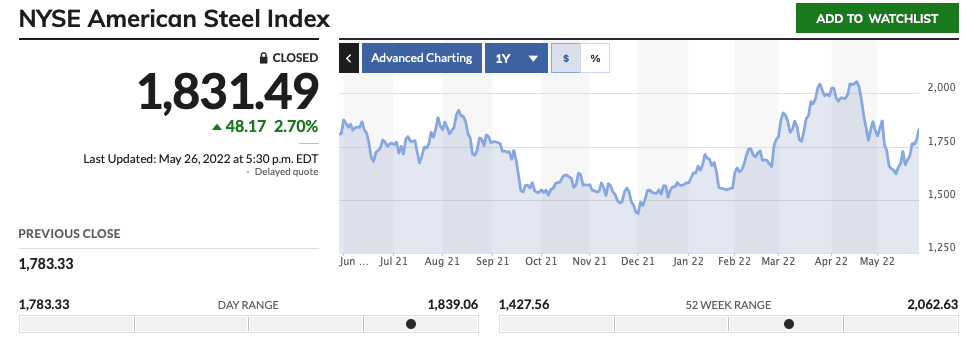

But over the last months, the price of steel has declined from a recent high, despite the recent bounce back.

With the recent downtrend in the price of steel, many dividend investors are reluctant to invest in Nucor, because its share price is very correlated with the price of steel. Let’s look deeper and try to understand if Nucor is still an interesting stock for dividend growth investors.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

Nucor’s Growth Through Acquisitions

If you still wondering why Nucor’s dividend rate of $2.00 and dividend yield is so low, compared to the earnings, and even the dividend payout of about 6.43% is the lowest among Dividend Aristocrats for a reason – acquisitions.

Recently the company announced the acquisition of Overhead Doors for $3B, which is one of the largest company garage doors for both residential and commercial use. Given the size of Nucor, the company needs to look for acquisitions to continue to grow, and it seems like that is one of the main reasons why management has not raised the dividend as much as it could.

The acquisition allows Nucor to benefit from additional synergies and costs savings, and given the price of 13X trailing EBITDA, for a company that has 60% of the overhead door market does not seem like a bad deal.

Additionally the company also acquired a majority stake in California Steel, and Elite Storage Solutions.

Current Valuation

Nucor remains one of the cheapest Dividend Aristocrats and Dividend Champions, with a price-to-earnings (P/E) ratio under 5X, and its trailing twelve month (TTM) free cash flow yield of nearly 20%. At the same time the company has one of the lowest dividend payout ratios, under 7%, and it has a manageable amount of debt, as seen in the chart from Portfolio Insight*.

While trading at a price-to-book (P/B) ratio just slightly over 2X, the stock seems incredibly attractive. But there is a clear reason why the valuation has been low – declining steel prices. Apart from that the company continues to increase its free cash flow generation, which is a great sign for investors and shareholders of the company

The company continues to focus on increasing its dividend, and according to the Dividend Radar tool from Portfolio Insight* the company has raised the dividend for 49 consecutive years. However, even despite the increases, the payout ratio remains extremely low.

While Nucor continues to increase its dividend, it also expanded its buyback program of $4B for this year, which given the current stock price is expected to buy over 10% of the company’s total outstanding shares. Adding this to the stock performance, and the dividend, investors can expect a double digit return on Nucor, as long as the stock price remains relatively stable, and steel prices don’t fall abruptly.

Steel Market Risks

Government Risk

The steel market has a strong governmental influence, in order to control the level of steel imports into US and prevent the production of steel to be completely outsourced overseas. It is a matter of national security, and it is one of the reasons why Section 232 exists. This has indirectly pushed steel prices in the US upwards, because importing steel freely would de-incentivize the production in US soil.

The fact that Nucor operates in a sector with a lot of scrutiny and legislation that protects its business model is a clear advantage, and one of the reasons the company has had a stellar performance over the last year.

Underlying Commodity Risks

The major risk that Nucor faces is a lower steel price, this could really hurt the stock price, as the earnings estimates are revised lower. While demand for steel remains high, and the supply is relatively stable in the US, worldwide, there is plenty of supply. In essence, the current legislation that prevents companies from importing steel remains one of the biggest advantages of Nucor.

Conclusion on Nucor (NUE) – Is the Rally in Steel Prices Over?

Although the recent decline in steel prices could continue to drive prices lower, Nucor (NUE) remains an undervalued Dividend Aristocrat. At these levels investors are getting a nearly 20% free cash flow yield, and even if we factor in lower steel prices, Nucor is still trading at a very attractive valuation.

Disclosure: Value of Stocks holds no positions in the stocks mentioned. You can read his disclosure.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Value of Stocks

Value of Stocks is an independent financial information provider. Focused on analyzing stocks and providing investors with information, so they can make better investment decisions. Access multiple articles on stock analysis, commodities and market news.