Brandywine Realty Trust (BDN) cut its dividend because of declining occupancy rates and rising interest rates, resulting in a need for greater liquidity.

The REIT must improve liquidity to fund project development and meet interest expenses. One source was the dividend, and thus, the company cut it. The share price was already down substantially but fell another 20% to 25% as investors started selling this dividend stock. It is unlikely that the dividend will be increased to its previous level. Also, a risk exists for future cuts.

Affiliate

Portfolio Insight is a leading portfolio management and research platform.

- 9,000+ stocks and ETFs in its database

- Access up to dozens of metrics, 20-years of financial data from S&P Global, fair value, margin of safety, charting, etc.

- Avoid dividend cuts with the Dividend Quality Grade and screening tools.

Click here to try Portfolio Insight for free (14-day free trial).

Overview of Brandywine Realty Trust (BDN)

Brandywine Realty Trust is an office real estate investment trust (REIT) founded in 1986. The firm operates primarily in Philadelphia, Pennsylvania (~74.5% of the rent base), Austin, Texas (~17.8% of the rent base), and Washington, D.C (~4.9% of the rent base). It owns, develops, and manages urban, suburban, and town center properties. As of June 2023, the REIT owned 162 properties with 22.8 million square feet. Brandywine strongly focuses on life science buildings, especially in the Philadelphia metro area.

Total revenue was $484.5 million in 2022 and $485.3 million in the past twelve months. Most revenue is from rent, with a smaller fraction from management fees, leasing, labor reimbursement, and others.

Dividend Cut Announcement

Brandywine Realty Trust (BDN) cut its dividend on Thursday, September 20, 2023. The REIT’s quarterly dividend was $0.19 per share before the announcement. The dividend is now $0.15 per share. In a press release, the company’s CEO said,

“Our 2023 business plan remains on target with a continuation of strong leasing and operating metrics,” stated Gerard H. Sweeney, President and Chief Executive Officer for Brandywine Realty Trust. “However, current capital market conditions are such that further enhancing our already strong liquidity position makes sense. As such, we are adjusting our quarterly dividend rate to $0.15 per share that represents the minimum dividend payout level we expect to maintain for the foreseeable future.”

Brandywine Realty is obviously trying to strengthen its balance sheet because of high-interest rates. The Trust uses debt for expansion, and rising rates make debt more expensive.

Challenges

As a commercial real estate REIT, Brandywine Realty is facing a challenging office market with declining demand caused partially by hybrid work. In turn, this has pressured occupancy rates. New construction has not slowed and will add to the problem. In addition, high-interest rates are making debt more expensive.

Declining Occupancy Rates

One of the consequences of the pandemic was an acceleration and greater acceptance of remote and hybrid work. Increasingly, workers are seeking jobs where they can work from home for part or all of the week. As a result, hybrid work is gaining in popularity, and people will be in the office for three or four days per week and work from home for the remainder.

In turn, demand has taken a hit because office vacancy rates have risen. At the end of August 2023, the total vacancy rate in Philadelphia was 14.2%. Interestingly, the value is better than the national average of 17.5%. Washington, D.C., has a vacancy rate of 15.3%, and Austin’s is poor at 21.2%.

These values indicated that employers are using only some of their space. Hence, Brandywine’s occupancy rate is declining, dropping to around 89.4% on average. But Austin is more of a problem, with properties only 86% occupied and the Philadelphia area is doing much better.

New Construction Will Add to the Problem

Furthermore, pressure from new construction may cause office vacancy rates to increase further. Six million square feet are under construction in Austin, or nearly 7% of existing inventory. This is a significant amount for this market. In comparison, Manhattan and Brooklyn, a more considerable market, have 7.69 million square feet under construction. Philadelphia and Washington, D.C., are building three and 4.27 million square feet, respectively.

Property markets will probably only absorb some of the new space without impacting utilization rates. Brandywine Realty will likely need to lower leasing prices. Moreover, existing leases will expire, and releasing rates may price lower as clients reduce their footprint compounding the problem.

Rising Interest Rates

Rising interest rates are making debt more expensive. The REIT’s debt service and interest coverage ratios are decreasing. During the second quarter earnings call, the CFO stated,

“We anticipate our debt service and interest coverage ratios to approximately 2.7, which represents a sequential decrease in our coverage ratios due to our projected development spend and higher interest rates.”

Interest expense in 2022 was $71.86 million but rose to $86.72 million in the last twelve months. Refinancing existing loans at higher rates and new debt for projects will probably drive interest costs higher.

Dividend Safety

Brandywine Realty’s dividend safety has been low for some time. The REIT receives a dividend quality grade of ‘F.’ Moreover, we anticipate that dividend safety will remain poor until the office market demand and supply equation rebalances. However, this activity may take many years.

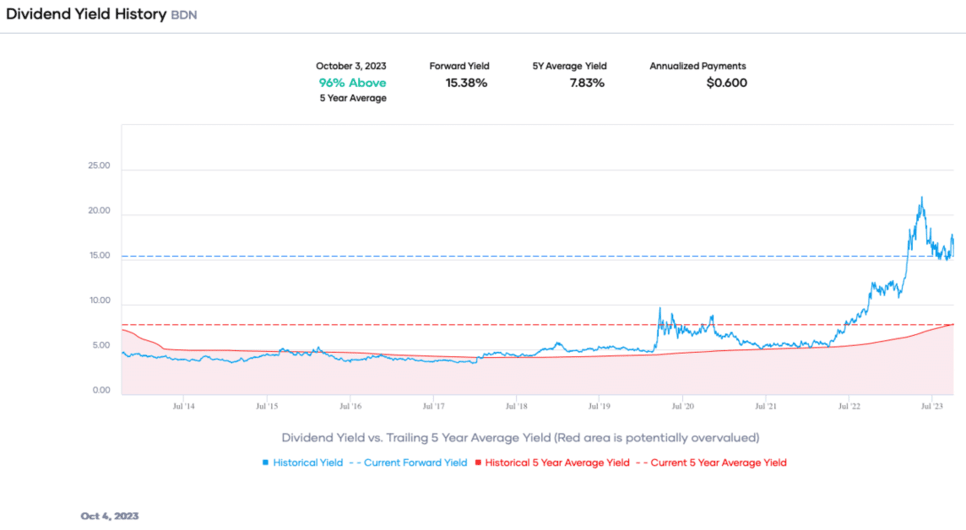

Despite slashing the dividend by 21.1%, the calculated dividend yield is still elevated at about 15.4%, a percentage usually associated with a distressed company. The quarterly rate is $0.15 per share.

The annual dividend now requires about $103.2 million ($0.60 yearly dividend x 172 million shares) compared to $130.7 million in 2022. The dividend-to-operating cash flow ratio will be better. However, the annual savings will probably go toward higher interest payments.

In addition, the Trust does not have an investment grade credit rating from S&P Global, which gives Brandywine Realty a BB+. However, Moody’s rates it a Baa3, the lowest investment grade rating.

Although safer, risk exists for a future dividend cut.

Final Thoughts on Brandywine Realty Trust (BDN) Dividend Cut

A challenging commercial real estate market is causing office REITs to struggle nationwide. The pandemic changed workers’ expectations and behavior, and hybrid work is increasingly common. Consequently, office space supply exceeds demand now. Additionally, interest rates are making debt and loans more costly. The combined pressure and the need to preserve liquidity caused Brandywine Realty to cut its dividend.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.