Picking income stocks can be challenging. Some equities pay dividends only to cut them in the future, and others are more focused on stock buybacks instead of dividends. However, research has shown that dividends provide investors with about 35% of total returns over time. It varies year-to-year, but holding solid income stocks that consistently raise their annual payout has proven successful.

We highlight three stocks for your portfolio that have prioritized returning cash to shareholders through dividends. Also, they all have excellent long-term growth prospects. We discuss PepsiCo (PEP), Amgen (AMGN), and Chevron Corporation (CVX).

Affiliate

Take the Simply Investing Course to learn more about investing and dividends.

- Lifetime access with 27 self-paced lessons.

- Covers placing stock orders, building and tracking portfolios, when to sell, reducing fees and risk, etc.

- Learn the 12 Rule of Simply Investing

- Simply Investing Coupon Code – DIVPOWER15.

Tried and True Dividend Stocks for Your Portfolio

PepsiCo

PepsiCo, Inc. (PEP) is a popular income and dividend growth stock. It is the No. 2 player in non-alcoholic beverages but is the market leader in salty snacks. The firm competes in almost every non-alcoholic beverage segment with many brands. It is known for drinks such as Pepsi, Gatorade, Mountain Dew, 7Up, Aquafina, Lipton, Sodastream, etc. Besides beverages, PepsiCo is the global leader in chips with brands like Lays, Doritos, Fritos, Cheetos, and more. The firm also owns Quaker Foods. The result is a diversified product line reaching $91,471 million in revenue in 2023.

PepsiCo’s products have high demand. It sells to restaurants, wholesalers, and retailers through its extensive distribution system. The distribution network offers a wide moat and is challenging to replicate.

Revenue and earnings per share typically increase annually because of more volume, price hikes, packing innovation, and brand extensions. Large brands offer seasonal variations and sometimes extend into niche market segments. Furthermore, as one of the largest beverage and food companies, PepsiCo acquires or partners with smaller players. For example, PepsiCo partnered with Celsius and took an equity stake, strengthening its energy drink offerings.

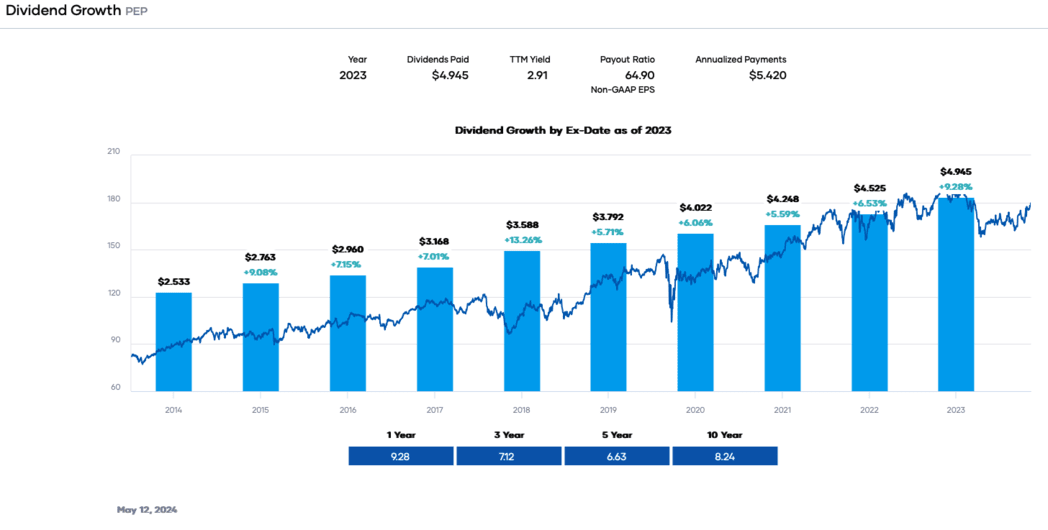

PepsiCo is a favorite equity when it comes to income. It is a Dividend King with a 52-year streak of yearly increases. It last raised the dividend in May 2023. People should expect another increase next month. According to Portfolio Insight, the dividend growth rate was around 8.3% on average in the past decade. Based on past history, we expect a mid-to-high single-digit percentage increase annually.

The share price has been relatively flat in 2024, resulting in a dividend yield of approximately 3%. This yield is backed by an adequate payout ratio of approximately 65%. Free cash flow of $7,924 million exceeds the dividend distribution requirement of $6,841 million. The ‘B+’ dividend quality grade and the A+/A1, upper-medium investment grade credit ratings boost dividend safety.

Despite growing top and bottom lines, PepsiCo’s stock price is below its all-time high in May 2023. It currently trades at a price-to-earnings ratio of ~21.6X, below the 5-year range. However, consensus earnings are anticipated to grow in 2024 and 2025. We view PepsiCo as a buy. It is one of those stocks that investors can buy and set on autopilot as part of a dividend reinvestment plan.

Related Articles About Pepsico on Dividend Power

- Pepsi (PEP) Investor Relations Guide

- Coca-Cola (KO) vs. Pepsi (PEP) Stock: Dividend Aristocrat Matchup

Amgen

From its founding in 1980, Amgen has grown into a leading biotechnology company. The firm is now valued at almost $150 billion. It is known for innovative blockbuster therapies like Enbrel to treat plaque psoriasis, rheumatoid arthritis, and psoriatic arthritis; Otezla for the treatment of adult patients with plaque psoriasis, psoriatic arthritis, and oral ulcers; and Prolia to treat postmenopausal women with osteoporosis. it is the second dividend stock we suggest for your portfolio.

Besides these drugs, Amgen has strengths and products in oncology, immunology, and cardiology. Total revenue was greater than $28 billion in 2023.

Amgen grows organically, and by M&A. Biotechnology, companies must consistently conduct research and development to renew their pipelines. They research new molecules and compounds to commercialize new therapies. However, the process takes years and costs billions of dollars. As a result, Amgen periodically acquires smaller companies. It most recently bought Horizon Therapeutics. This acquisition added several drugs in the market and future candidates.

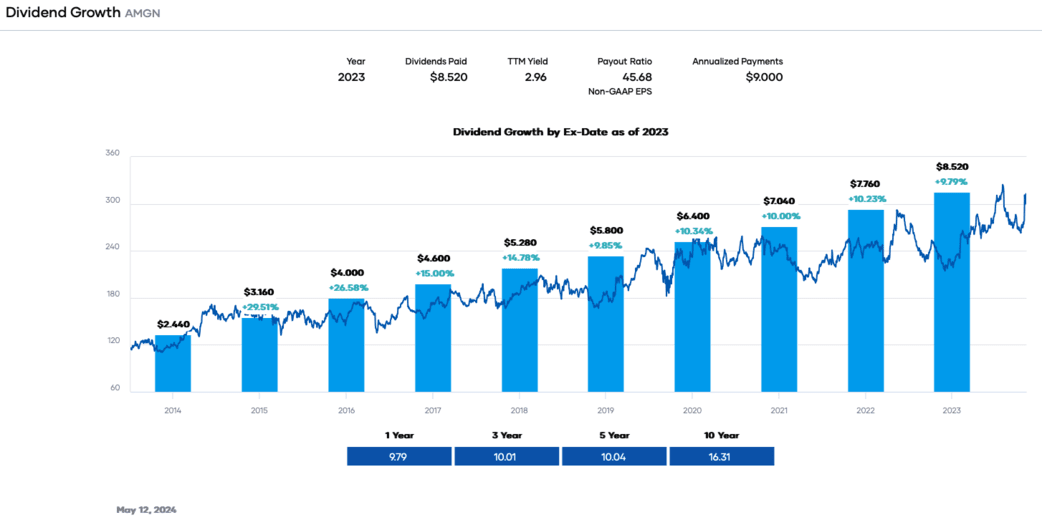

Amgen has paid a dividend since 2011. It is a Dividend Contender with a 12-year streak of increases. Because of the share price decline this year, the dividend yield has reached 3.3%. This value is below the 5-year average and more than double that of the S&P 500 Index. The dividend is growing about 10% per annum. We anticipate the rate to continue in the near term because of the 46% moderate payout ratio.

The moderate payout ratio suggests that the dividend safety is still excellent. The equity receives a ‘B’ from Portfolio Insight for its dividend quality. The one detraction is the high leverage ratio of 4.4X because of acquisitions. Amgen also has a BBB+/Baa1 lower-medium investment credit rating. In addition, free cash flow of $7,359 million more than covers the dividend requirement of $4,556 million.

Amgen’s struggling share price makes it attractive for income and dividend growth investors. Amgen’s stock is undervalued and trades at about 14 times anticipated 2024 earnings. As a result, we view this equity as a buy.

Related Articles About Amgen on Dividend Power

Chevron

Climbing energy prices have resulted in the Energy sector outperforming the other ten in 2024. High demand combined with curtailed supply will probably keep prices elevated. Integrated oil and natural gas companies, like Chevron, should benefit. It is the third dividend stock we like for your portfolio.

Chevron is the second-largest American integrated oil firm. It operates in two business segments: Upstream and Downstream. The Upstream business explores, develops, produces, and transports crude oil and natural gas. The Downstream business refines crude oil into petroleum and petrochemical products. Total revenue was $195,985 million in 2023.

The oil company grows chiefly by exploring and developing new crude oil and natural gas fields. It can also expand existing projects. These activities are capital intensive, giving large firms like Chevron an advantage. The aim is to add to verified reserves and develop the field for production. Additionally, Chevron acquires smaller companies. It has offered to buy Hess Corporation (HES) for $53 billion.

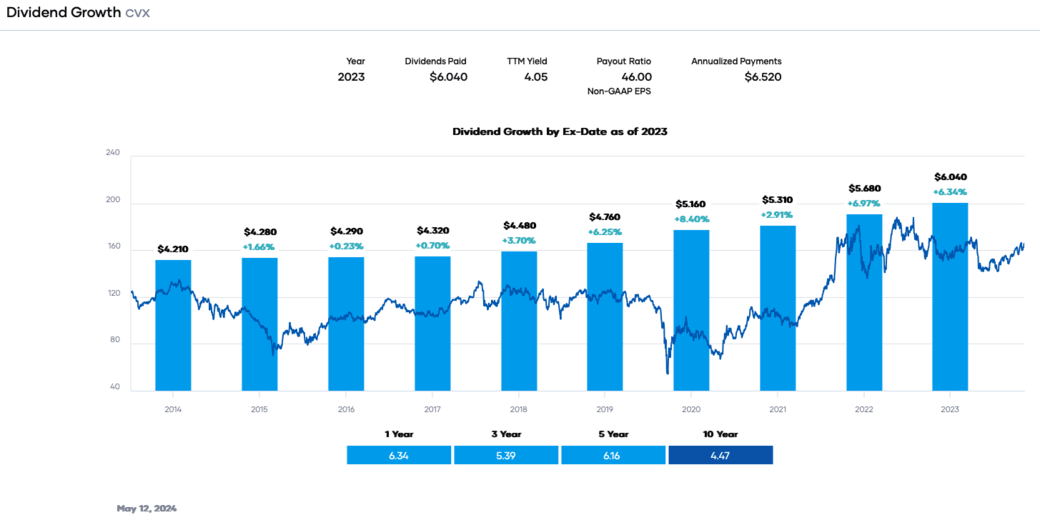

Because of increasing oil prices, Chevron’s revenue should be more in 2024 than in 2023. Similarly, earnings per share should be greater, too. That said, people can buy Chevron and get a 4% yield, with a dividend climbing from 4% to 6% per annum.

This yield and growth come with solid dividend safety. The firm is a 2024 Dividend Aristocrat with a 37-year streak of increases. The payout ratio is only 46%, and free cash flow of almost $20 billion easily covers the ordinary dividend requirement of $11.3 billion. Chevron earns an ‘A’ dividend quality grade, meaning it’s in the 90th percentile of dividend-paying stocks. It also has an AA-/Aa2 high-grade investment credit rating, giving greater confidence about safety.

We view Chevron as a buy because of the excellent yield, dividend growth, and reasonable valuation of 12.5 times earnings.

Related Articles About Chevron on Dividend Power

Disclosure: Long PEP, AMGN.

A version of this post by Dividend Power originally appeared on Investor Place and was republished with permission.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.