Bogleheads 3 Fund Portfolio

Lazy retirement portfolios simplify life for busy workers without the time to invest actively. An important one that works for many people is the Bogleheads 3 Fund Portfolio.

It is an excellent option for 401(k) and IRA retirement accounts because it contains exposure to American stocks, bonds, and international equities. Workers can just set and forget it because it is a preplanned asset allocation of three passive index funds except for an annual or bi-annual review.

Granted, retirement portfolios have a few other things to worry about, like rebalancing, the amount of contributions, expense ratios, etc. However, the Bogleheads Three-fund Portfolio is simple, and almost anyone can follow it.

Affiliate

Stock Rover is an award winning investment research platform.

- The site has 8,500+ stocks, 4,000 ETFs, and 40,000 mutual funds.

- Access to 650+ metrics, financial data, market news, stock and fund ratings, fair value, margin of safety, etc.

- Includes brokerage integration, portfolio tracking, rebalancing, watchlists, alerts, future income forecasts, etc.

Click here to try Stock Rover for free (14-day free trial).

History of the Bogleheads 3 Fund Portfolio

For those who don’t know, the Bogleheads are a group of investors who follow the investing principles espoused by the father of passive index funds and founder of Vanguard, John Bogle. He generally advocated indexing, diversifying investments, minimizing taxes, keeping it simple, and staying the course. As Jack Bogle so eloquently put it,

“In investing, the winning technique is to own the whole stock market via an index fund and then do nothing.”

Taylor Larimore, a Boglehead, initially advocated a 3 Fund Portfolio. The portfolio contains three total market index funds: a U.S. stock market fund, an international stock market fund, and a U.S. taxable investment-grade bond market fund. In 1997, the Bogleheads Three-fund Portfolio could finally be implemented when Vanguard introduced a total international index fund to investors.

As a historical note, a money market fund was also included in the initial idea for four total funds in the old Vanguard Diehards forum on the Morningstar discussion boards around 1999. This initial idea seemingly developed into the Bogleheads 3 Fund Portfolio.

What is the Bogleheads 3 Fund Portfolio?

The Bogleheads 3 Fund Portfolio is a strategy that uses three low-cost index funds to emphasize simplicity and tax efficiency. It also reduces the risk of style drift, tracking error, overlap, asset bloat, and other problems. The Bogleheads Three-fund Portfolio also reduces the possibility of fund manager changes. This risk is real, as new fund managers can underperform their predecessors. Does anyone recall Robert Stansky or Jeffery Voinik at the Fidelity Magellan Fund after they followed Peter Lynch?

The main idea is to own the most essential asset classes: U.S. stocks, international stocks, and U.S. bonds. Investors now have to decide only on asset allocation. The basic idea is to invest in uncorrelated assets using passive index funds to capture as much market return as possible with adequate diversification and lower volatility. These ideas should be everyone’s goal for their retirement fund.

Implementation

The table below outlines the Bogleheads 3-Fund Portfolio assuming an overall 60% stock / 40% bond asset allocation. Historically, in retirement plans, the three-fund portfolio has been the Vanguard Total Stock Market Index Fund (VTSMX), the Vanguard Total Bond Market Index Fund (VBMFX), and the Vanguard Total International Stock Market Index Fund (VGTSX). Some people prefer the Vanguard 500 Index Fund (VFINX) over the Vanguard Total Stock Market Index Fund.

| Asset Class | Vanguard Index Fund | Expense Ratio | Vanguard ETF | Expense Ratio |

|---|---|---|---|---|

| Total Stock Market Index | VTSMX | 0.14% | VTI | 0.03% |

| Total International Stock Market Index | VGTSX | 0.17% | VXUS | 0.07% |

| Total Bond Market Index | VBMFX | 0.15% | BND | 0.03% |

A person investing in Admiral shares will have a lower expense ratio than investor shares. Alternatively, Vanguard’s ETFs can be used for a taxable account. Although we focus on Vanguard funds, today, most asset managers offer passive index funds or ETFs.

Related Articles About Mutual Funds and ETFs on Dividend Power

- The Largest Mutual Funds

- The Complete Vanguard ETFs List

- The Complete Fidelity ETF List

- The Complete T. Rowe Price ETF List

- The Complete SPDR ETF List

Pros and Cons

Advantages

There are several pros and cons to the Bogleheads 3 Fund Portfolio. Under benefits, index funds are low-cost, diversified, and tax-efficient. In addition, the portfolio is simple to understand and implement and will usually outperform most active fund portfolios over time.

It is well known that low-cost index funds outperform active funds because they usually match the index’s return over time minus the expense ratio and trading costs. Passive index funds have lower fees than active mutual funds, and ETFs have even lower expense ratios.

Furthermore, investing in index funds removes the short-term trading mentality and other distractions people should not care about.

Disadvantages

We now outline several cons, but these are minimal. Limited control exists; the portfolio will only match market returns and be overweight mega-cap stocks. However, reduced control is a negligible disadvantage, but some people desire to be hands-on. Instead, they should set the asset allocation and review it every six months to one year.

Second, some people like to beat the market, but studies have shown that most cannot do so in retirement plans. So, matching market returns is a reasonable approach.

The last item is a real risk. Mega-cap stocks, especially tech stocks, are increasingly dominating the market. Consequently, index returns are heavily influenced by a handful of stocks. For example, the S&P 500 Index is dominated by mega-cap tech stocks like Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), etc.

Performance and Risk

We perform an evaluation using Vanguard funds to assess the performance and volatility of the Bogleheads Three-fund Portfolio further. Our goal is to determine how this three-fund portfolio does over 20+ years in a retirement plan assuming a buy-and-hold strategy.

We examine the period from January 2000 to December 2023 because it encompasses both bull markets and recessions with bear markets.

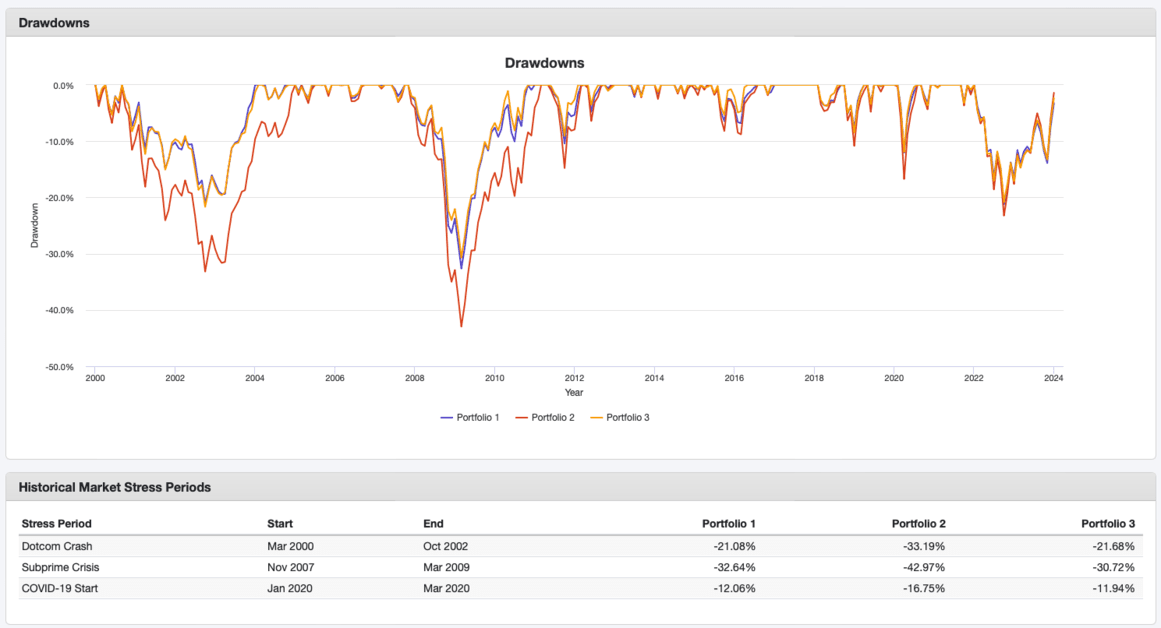

In this comparison, using the Portfolio Visualizer tool, we examine the Vanguard Total Stock Market Index (VTSMX), the Vanguard Total International Stock Index (VGTSX), and the Vanguard Total Bond Market Index (VBMFX). We evaluate the following percentages: Portfolio 1 – 40% / 20% / 40% (blue line), Portfolio 2 – 60% / 20% / 20% (red line), and Portfolio 3 – 60% / 0% / 40% (orange line).

Our assumption is the portfolios are rebalanced annually. We discuss the compound annual growth rate (CAGR), standard deviation, and max drawdown numbers.

The results vary for CAGR and volatility. But clearly, including a higher percentage of U.S. stocks (Portfolio 2) increases returns slightly but simultaneously causes volatility to rise. Portfolio 2 has the best and worst years and the most significant max drawdown.

Removing international stocks and increasing the allocation to U.S. bonds (Portfolio 3) increases returns slightly but significantly reduces volatility. It also causes the Sharpe Ratio, a measure of risk-adjusted relative returns, to climb. Also, the worst years and max drawdown are lower in value.

The growth of portfolio 3 is greater than that of portfolio 1 or 2 because U.S. equities have performed better than bonds and international stocks during this period. Large-cap U.S. tech equities have driven the stock market’s gains, while low-interest rates kept bond returns flat. Also, when interest rates rose, bond prices fell, resulting in one of the worst years for fixed income in 2022. Moreover, global equities have performed poorly on a relative basis because of the robust American economy.

Max Drawdowns

The max drawdowns are worse for portfolio 2 due to a lower percentage of bonds and a higher percentage of stocks. Furthermore, the drawdowns were more extended for portfolio 2, meaning this asset allocation took longer to recover. Both portfolios 1 and 3 produce more tolerable drawdowns of shorter duration. But of the two, portfolio 3 is better for those seeking lower volatility and higher risk-adjusted returns, implying that replacing international stocks with more U.S. stocks and bonds is better.

The Bottom Line About the Bogleheads 3 Fund Portfolio

Most retirement plans have a combination of passive index funds and active funds. The Bogleheads 3 Fund Portfolio is one possible strategy, assuming all asset classes are available as index funds in a retirement plan. Because of their advantages, employing passive index funds for retirement portfolios in 401(k) plans or IRAs takes little effort. A future retiree will capture much of the market return with good diversification and minimize costs while avoiding many cons.

Interestingly, there is no penalty for excluding international stocks. In fact, the reverse is true because returns are high, and volatility is much lower in portfolio three. As a result, investors may want to think twice about their international stock exposure.

Related Articles on Dividend Power

- Warren’s Buffett Two-Fund Portfolio: It’s Easy

- The Little Book of Common Sense Investing Review: Is Bogle’s Investment Guide Still Relevant?

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.