It’s the end of February, and Valentine’s Day was on everyone’s mind. People bought candy, cards, flowers, jewelry, and clothing, and ate out at restaurants.

The National Retail Federation estimates consumers will spend a record $29.1 billion on Valentine’s Day this year. As a result, companies providing these products and services can make suitable investments.

Moreover, they often have market leadership and scale because of industry consolidation. Consequently, they return prodigious amounts of cash to investors through dividends and share buybacks.

This article examines three dividend growth stocks for February 2026, emphasizing companies with higher sales during Valentine’s Day.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

Dividend Growth Stocks for February 2026

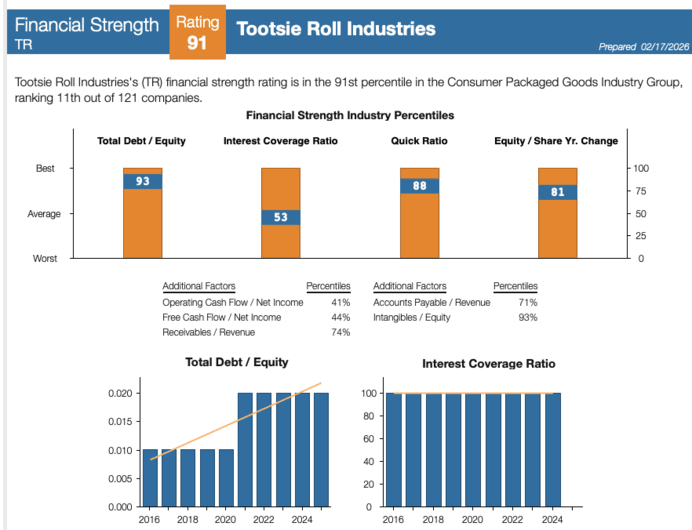

Tootsie Roll Industries (TR)

Tootsie Roll Industries, Inc. traces its roots to the late 1890’s when its namesake product, the Tootsie Roll, was first created. Today, the company sells a wider variety of candy and gum products. Other well-known brands include DOTS, Junior Mints, Andes, Charms, Blow-Pops, Sugar Daddy, and Dubble Bubble.

With over 50 years of dividend increases, Tootsie Roll is on the list of Dividend Kings.

Tootsie Roll reported Q3 2025 results on October 22nd, 2025. Net sales were up 3% to $230.6M for the quarter versus $223.9M in the prior year. In the same period, net earnings rose to $35.7M compared to $32.8M. Diluted EPS increased 9% to $0.49 per share from $0.45 on a year-over-year basis on higher sales volumes and a lower share count.

Although volumes and revenue declined in 2024, margins were higher because of lower freight costs and higher prices. Tariffs and inflation, particularly for cocoa and chocolate, are impacting input costs and margins in 2025. Inflation is a concern, and input costs have risen for labor, ingredients, freight and delivery, fuel, packaging materials, energy, and manufacturing supplies. The company has raised prices in response to restore margins.

Tootsie Roll should achieve on average 3% earnings per share growth moving forward to 2030, mostly via small amounts of revenue growth driven by incremental product innovation and price increases. Influences on earnings per share growth include commodity input and freight cost inflation on the downside, and volume and price increases and operational efficiencies to the upside.

The regular cash dividend was last increased in 2016 and is currently $0.36 per share. The payout ratio is only ~29%, and there is room for an increase. The company issues a 3% stock dividend each year in addition to the regular dividend, giving a ~4% effective yield if an investor sells the stock dividend annually.

Mondelez International (MDLZ)

Mondelez manufactures and distributes snacks in more than 150 countries, generating annual revenues of ~$38 billion. Its 2025 revenues came from Europe (39%), North America (28%), Asia, the Middle East, & Africa (21%), and Latin America (13%).

While cocoa cost headwinds continue to impact Mondelez’s profitability, the company is doing what it can control — improved volumes, brand investments, structural cost savings, and disciplined capital allocation — to create multi-year shareholder value as cocoa prices normalize over time.

Mondelez reported its Q4 2025 results on 02/03/2026. For the quarter, its organic net revenue growth was 4.4%, with pricing up 8.5%, offset by volume/mix of -4.1%. Net revenue rose 9.3% year-over-year to $10.5 billion. Organic net revenue growth of 8.3% in Europe was the strongest, followed by 7.5% in Asia, the Middle East, & Africa, and 4.4% in Latin America. It was negative at -0.5% in North America.

The adjusted gross profit rose 5.8% to $3.2 billion, along with an adjusted gross profit margin contraction of 1.0% to 30.5%. Adjusted earnings rose 7.2% to $929 million, while the adjusted earnings per share rose 10.8% to $0.72.

For the full year, its organic net revenue growth was 4.3% with pricing up 8.0%, offset by volume/mix of -3.7%. Net revenue rose 5.8% YOY to $38.5 billion. Organic net revenue growth of 8.6% in Europe was the strongest, followed by 5.7% in Asia, the Middle East, & Africa, and 4.6% in Latin America, while it was negative at -1.9% in North America. Free cash flow was $3.2 billion for the year.

Mondelez initiated its guidance for 2026, as follows: Organic net revenue growth of 0-2% and adjusted EPS growth of 0 5% on a constant currency basis, while it projects to generate free cash flow of ~$3 billion.

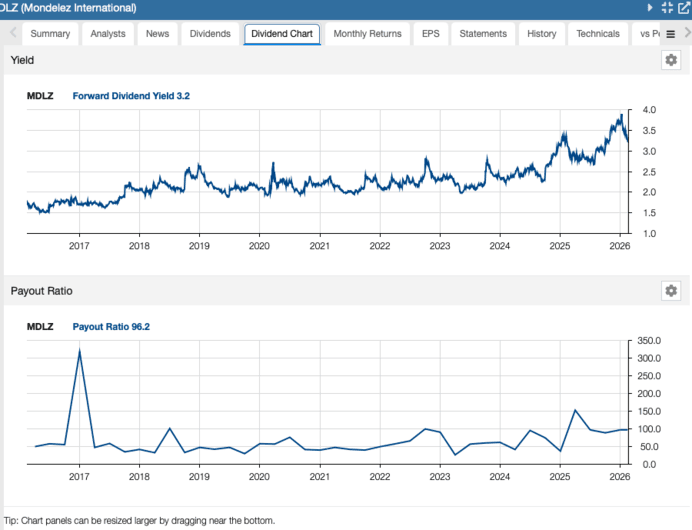

Long term, MDLZ should continue to innovate, invest in its brands, and expand its offerings. We estimate a five-year EPS growth rate of 7.5%, assuming that emerging markets will typically drive relatively higher growth than developed markets, and estimate dividend growth of 3.0% annually for a payout ratio that better aligns with its historical levels of ~50%. Mondelez is on the list of Dividend Contenders.

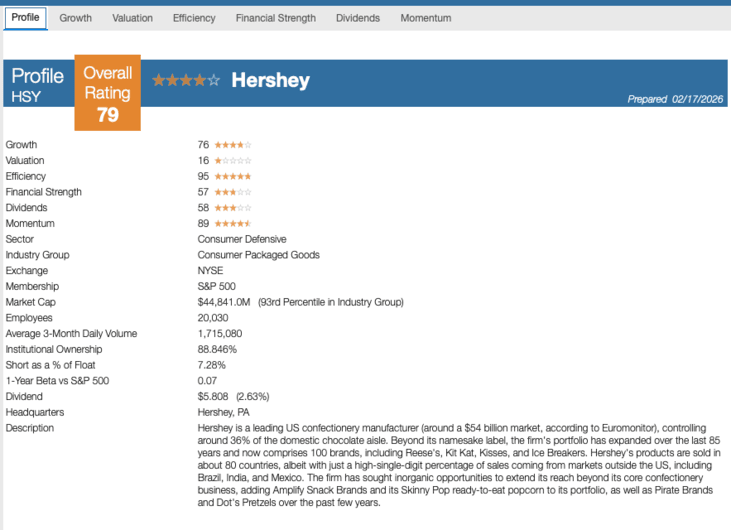

The Hershey Company (HSY)

The Hershey Company, founded in 1894, is a manufacturer of chocolate and sugar confectionery products that sells major brands such as Hershey’s, Reese’s, Kisses, Cadbury, Ice Breakers, Kit Kat, Almond Joy, Jolly Rancher, Twizzlers, Heath, and Milk Duds. Hershey primarily operates in North America but has international operations as well.

On February 5th, 2026, Hershey reported results for the fourth quarter of 2025. The North America Confectionery segment (80% of sales) grew its sales 5% over the prior year’s quarter, thanks to price hikes. Earnings-per-share decreased 36%, from $2.67 to $1.71, but exceeded the analysts’ consensus by $0.31, primarily thanks to an effective hedging strategy, which partly offset the effect of exceptionally high cocoa prices.

In 2025, Hershey faced an extremely strong headwind from sky-high cocoa prices, which squeezed the profit margins of the chocolate maker. However, cocoa prices have declined sharply in recent months. As a result, Hershey provided positive guidance for 2026. It expects 4%-5% growth in sales and adjusted earnings per share of $8.20-$8.52.

Hershey’s earnings-per-share growth stems from several factors. The first one is organic revenue growth, which Hershey has achieved despite the public becoming more conscious about healthy eating habits.

The company has also been able to improve its margins throughout the last decade. Hershey owns well-recognized brands, so price hikes have not been a headwind to increasing the volume of its products. Hershey is set up well for nearly any environment. Hershey posted low earnings last year due to sky-high cocoa prices, but we view this headwind as temporary and expect 33% growth in earnings this year and 6% average annual growth in earnings per share beyond this year.

Hershey’s dividend payout ratio spiked last year due to the depressed earnings amid exceptionally high cocoa prices, but we expect the payout ratio to normalize in the upcoming years. Moreover, Hershey just raised its dividend by 6% this year, thus showing confidence in a strong recovery.

Related Article About Hershey on Dividend Power

Disclosure: The author has no positions in any stocks mentioned.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Bob Ciura

Bob Ciura is President of Content at Sure Dividend. Bob has worked at Sure Dividend since October 2016. He oversees all content for Sure Dividend and its partner sites. Prior to joining Sure Dividend, Bob was an independent equity analyst. Bob received a bachelor’s degree in Finance from DePaul University, and an MBA with a concentration in Investments from the University of Notre Dame.