Technology is a high-growth industry where many companies are focused on reinvesting the majority or even all of the cash flows to grow the company further.

That’s why many technology stocks offer no dividend payments, and many that do pay dividends have very low yields.

Some tech stocks are outliers, however. In this article, we’ll highlight three technology companies that could be attractive for income investors due to their high dividend yields.

All three stocks have yields above 2.5%, compared with the S&P 500’s average yield of 1.3%.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

3 High-Yielding Tech Stocks

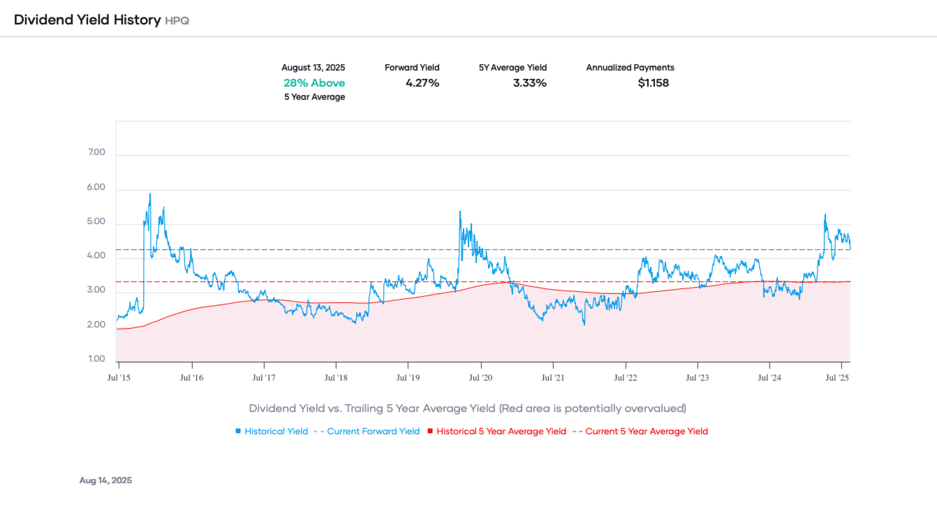

HP Inc. (HPQ)

Hewlett-Packard’s story goes back to 1935 with two men in a one-car garage making a significant impact on electronic test equipment, computing, data storage, networking, software, and services that have lasted for more than eight decades.

HP Inc. has centered its business activities around two main segments: its product portfolio of printers and its range of so-called personal systems, which includes computers and mobile devices.

HP reported its second quarter (fiscal 2025) results in June. The company reported revenue of $13.2 billion for the quarter, which beat the analyst consensus estimate by a solid $80 million, and which was up around 3% from the previous year’s quarter.

This was slightly better than the performance of the company during the previous quarter, when revenues had grown at a somewhat lower rate. Non-GAAP earnings per share totaled $0.71 during the second quarter, which was slightly below the analyst consensus estimate. HP Inc. saw its operating margin decline over the last year.

The company currently forecasts earnings per share in a range of $0.68 to $0.80 for the third quarter of the current fiscal year, which would mean a better result versus the most recent quarter at the midpoint of the guidance range. For the current year, HP forecasts earnings per share of around $3.15, with free cash flow being forecasted at around $2.8 billion.The company’s strong cash flow allows it to return significant amounts of cash to shareholders through dividends. With a 2025 payout ratio expected to be below 40%, the dividend payout looks secure. Also, it is a Dividend Contender with a 16 year streak of increases. HPQ stock currently yields 4.4%.

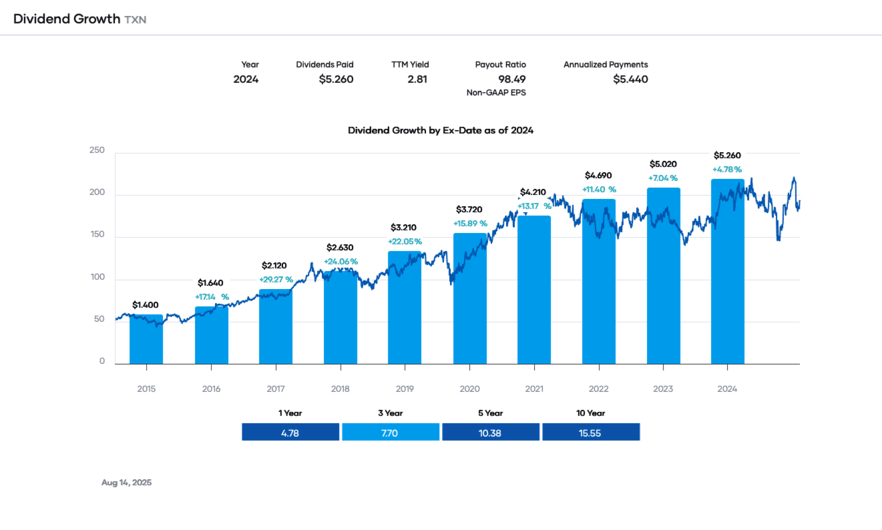

Texas Instruments (TXN)

Texas Instruments is a semiconductor company that operates two business units: Analog and Embedded Processing. Its products include semiconductors that measure sound, temperature, and other physical data and convert them to digital signals, as well as semiconductors that are designed to handle specific tasks and applications.

Texas Instruments reported its second-quarter earnings results on July 22. During the quarter, Texas Instruments generated revenues of $4.45 billion, which represents an increase of 17% versus the previous year’s second quarter. This was better than what the analyst community had forecasted, as estimates were beaten by $130 million.

Texas Instruments managed to keep its gross profit margin at a very solid level of 58%, and due to the effect of operating leverage, the company saw its operating margin expand compared to one year earlier. Texas Instruments generated earnings per share of $1.41 during the second quarter, which was better than the consensus estimate, coming in $0.08 ahead of the analyst community’s forecast.

Texas Instruments generated solid cash flows over the last year, although slightly less than during the previous period. Shareholder returns totaled $6.7 billion over the last twelve months, which was up from the prior year. Spending on buybacks rose to a little more than $1.8 billion. Texas Instruments guides for revenues of $4.65 billion and earnings-per-share of around $1.48 for the current quarter.

XN should be able to benefit from rising demand for processors, as favorable trends such as Industry 4.0 and automation pose long-term tailwinds for the chip company. Texas Instruments’ policy of returning all free cash flows to the company’s shareholders in the form of dividends and share repurchases affects its earnings-per-share growth. The equity is also a Dividend Contender.TXN currently yields 2.9%.

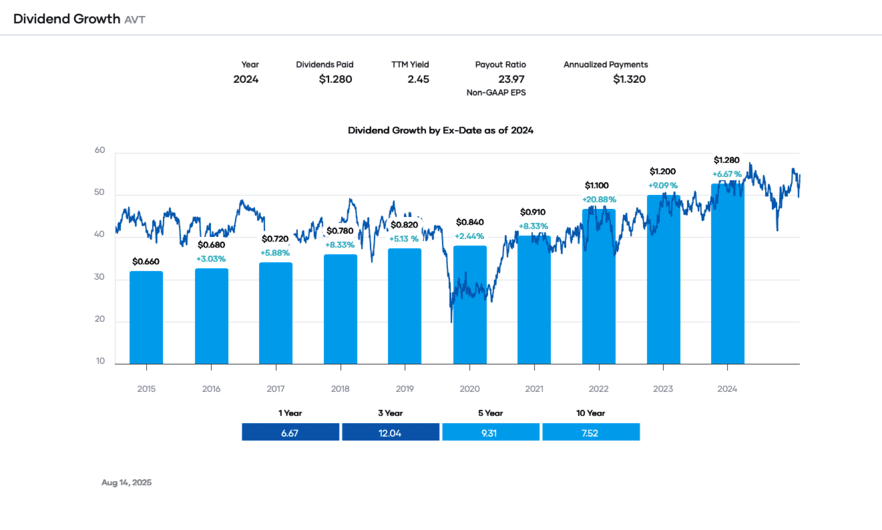

Avnet Inc. (AVT)

Avnet Inc. (AVT) is a global distributor of electronic components and technology solutions, connecting semiconductors and other component suppliers to customers in 140 countries. Avnet is the third largest semiconductor distributor in the world and the largest for European chip distribution.

The company has two main operating segments: the Electronic Components segment, which sells electrical components, semiconductors, interconnect, passive, and electromechanical components, and the Farnell segment, which sells kits, tools, test measurement, and electronic components. The Electronic Components segment is the primary segment of the company, constituting more than 90% of sales.

On August 6th, 2025, Avnet announced Q4 2025 results, reporting non-GAAP adjusted diluted EPS of $0.81, which beat estimates by $0.09. The company reported revenue of $5.6 billion, which was flat year-over-year. Adjusted operating margin declined to 2.5% from 3.5% a year ago.

The company generated $139 million in operating cash flow and returned $78 million to shareholders via dividends and buybacks. Farnell posted a 3% sales increase and expanded its operating margin by 25 basis points to 4.3%.

For fiscal 2025, Avnet delivered $22.2 billion in revenue, down from $23.8 billion in the prior year, with adjusted EPS of $3.44 versus $5.34. Operating cash flow reached $725 million, aided by a $414 million inventory reduction. The company returned $414 million to shareholders, including $301 million in repurchases representing 6.7% of shares outstanding.

Looking ahead, Q1 FY2026 guidance calls for sales of $5.55–$5.85 billion and adjusted EPS of $0.75–$0.85, implying ~2% sequential growth.Avnet has paid increasing dividends over the past 12 years, making to another Dividend Contender. AVT stock currently yields 2.5%.

Disclosure: No positions in any stocks mentioned.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Bob Ciura

Bob Ciura is President of Content at Sure Dividend. Bob has worked at Sure Dividend since October 2016. He oversees all content for Sure Dividend and its partner sites. Prior to joining Sure Dividend, Bob was an independent equity analyst. Bob received a bachelor’s degree in Finance from DePaul University, and an MBA with a concentration in Investments from the University of Notre Dame.