The average dividend yield in the S&P 500 Index remains low at 1.1%. As a result, income investors largely have to settle for less dividend income when buying stocks. However, there are still quality companies with high dividend yields well above the market average.

Investors do not have to sacrifice income when it comes to quality dividend payers with competitive advantages and long-term growth potential. This article will highlight three stocks that could be attractive for income investors due to their high dividend yields.

All 3 stocks have yields above 5%, compared with the S&P 500’s average yield of 1.2%.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

High-Yielding Stocks

HP Inc. (HPQ)

HP Inc. has centered its business activities around two main segments: its product portfolio of printers and its range of so-called personal systems, which includes computers and mobile devices.

HP reported its fourth quarter (fiscal 2025) results on November 25. The company reported revenue of $14.6 billion for the quarter, which beat the analyst consensus estimate by a solid $150 million, and which was up 4% from the previous year’s quarter.

This was a bit better than the performance of the company during the previous quarter, when revenues had grown at a slightly slower rate. Non-GAAP earnings-per-share totaled $0.93 during the fourth quarter, which was just ahead of the analyst consensus estimate.

HP Inc. saw its operating margin decline over the last year. The company currently forecasts adjusted earnings per share in a range of $0.73 to $0.81 for the first quarter of the current fiscal year, which would mean a weaker result versus the most recent quarter.

For the current year, HP is expected to generate earnings per share of around $3.05, with management forecasting free cash flow at around $2.8 billion.

Over the last decade, HP’s earnings per share rose thanks to a combination of growing net earnings and a declining share count, although the ~8% growth rate since 2016 will likely not be replicated forever. HP is a leader in the printing and personal computing markets, but these are areas that face challenges as consumers continue to prioritize mobile devices.

The adoption of 3D printing could help, as HP is already entrenched in this industry, but so far, the majority of profits are generated by traditional printers and printing products. Even without any meaningful business growth, corporations can still generate growth on a per-share basis using shareholder return programs, and we believe that buybacks will remain a key growth factor for HP in the future.

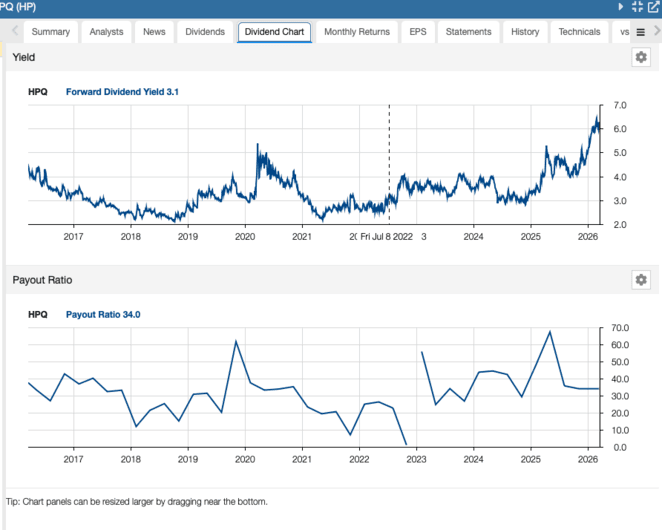

HP has increased its dividend for 15 consecutive years and currently yields 6.4%. The stock is also a Dividend Contender.

Kimberly-Clark Corp. (KMB)

The Kimberly-Clark Corporation is a global consumer products company that operates in 175 countries and sells disposable consumer goods, including paper towels, diapers, and tissues. It operates through two segments that each house many popular brands: Personal Care Segment (Huggies, Pull-Ups, Kotex, Depend, Poise) and the Consumer Tissue segment (Kleenex, Scott, Cottonelle, and Viva), generating about $20 billion in annual revenue.

Kimberly-Clark posted fourth quarter and full-year earnings on January 27th, 2026, and results were mixed. Sales fell 0.5% year-over-year to $4.1 billion as organic sales growth of 2.1% was offset by a 2.5% decline resulting from the exit of the company’s private label diaper business in the US.

Organic sales growth was driven by volume and mix growth of 3%, partially offset by a 1.1% pricing headwind. Adjusted gross margin was 37% of sales, in line with the year-ago period. Adjusted earnings-per-share came in at $1.86, which was up from $1.50 a year ago and a nickel ahead of estimates.

Management noted the merger with Kenvue was overwhelmingly approved by shareholders of both companies, and that it is expected to close in the second half of this year.

Kimberly-Clark’s competitive advantage is in its longstanding dominance with a variety of its brands, which are well known in the marketplace. It should also perform well during recessions as most of its products are consumable staples, which was evidenced during the COVID recession.

The dividend was also boosted to $5.12 per share annually from $5.04 previously. That is the 54th consecutive year of dividend increases for the company. KMB currently yields 5.0%. The equity is a Dividend King.

H&R Block (HRB)

H&R Block, Inc. is a U.S.-based tax preparation and financial services company founded in 1955 and headquartered in Kansas City, Missouri. The firm provides assisted and do-it-yourself tax return preparation services through its extensive network of approximately 9,000 retail offices, online platforms, and mobile applications, serving individual taxpayers as well as small-business clients across the United States, Canada, and Australia.

Beyond core tax filing services, H&R Block offers related financial products, including refund transfer services, prepaid debit cards, loans, identity protection, and small-business bookkeeping and payroll solutions through its Wave Financial subsidiary.

On February 3, 2026, H&R Block, Inc. reported fiscal 2026 second-quarter results for the period ended December 31, 2025, demonstrating solid progress across its diversified tax and small-business solutions portfolio. The company delivered healthy top-line growth, with total revenue rising 11.1 percent year over year to $198.9 million, supported by higher assisted tax preparation volume, increased net average charges, strong Wave subscription and payments growth, and solid DIY software performance, underscoring the strength of its multi-channel model across assisted, do-it-yourself, and online offerings.

Profitability remained seasonally negative, with a net loss from continuing operations of $241.6 million, or $1.91 per share, and adjusted loss per share of $1.84, though both metrics improved by mid-single digits year over year and reflected typical off-season dynamics rather than underlying deterioration.

Capital returns were another clear strength, as H&R Block returned $507.7 million to shareholders year to date via dividends and buybacks, while retaining roughly $700 million of remaining capacity under its $1.5 billion repurchase authorization, signaling continued confidence in long-term cash generation. Looking ahead, the company reaffirmed fiscal 2026 guidance for revenue of $3.875 to $3.895 billion, EBITDA of $1.015 to $1.035 billion, and adjusted diluted EPS of $4.85 to $5.00.

HRB has paid increasing dividends over the past 11 years. HRB stock currently yields 5.6%. The company is a Dividend Contender.

Disclosure: No positions in any stocks mentioned.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Bob Ciura

Bob Ciura is President of Content at Sure Dividend. Bob has worked at Sure Dividend since October 2016. He oversees all content for Sure Dividend and its partner sites. Prior to joining Sure Dividend, Bob was an independent equity analyst. Bob received a bachelor’s degree in Finance from DePaul University, and an MBA with a concentration in Investments from the University of Notre Dame.