Income investors value reliability and consistency, as well as high dividend yields. Some stocks provide a combination of these factors, such as the Dividend Champions — stocks that have raised their payouts for at least 25 years in a row.

These companies have demonstrated their ability to manage temporary downturns, including recessions and the recent pandemic, reasonably well, and have maintained their dividend payouts even during such challenging times, which makes them valuable for those seeking a low-risk income stream. These 3 Dividend Champions have above-market yields and long-term dividend growth.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

Highest Yield Dividend Champions

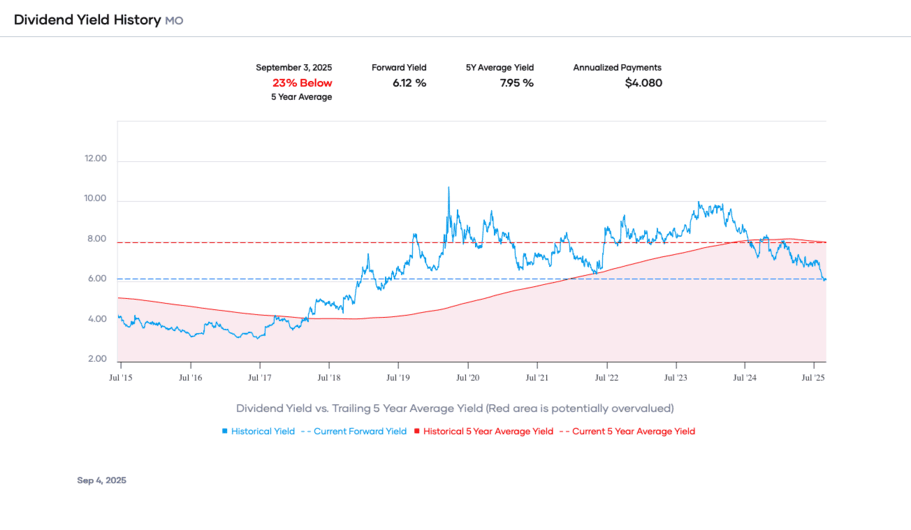

1: Altria Group (MO)

Dividend Yield: 6.3%

Altria Group was founded by Philip Morris in 1847. Today, it is a consumer staples giant. It sells the Marlboro cigarette brand in the U.S. and several other non-smokable brands. Altria also has large stakes in Juul, a vaping products manufacturer and distributor, as well as cannabis company Cronos Group (CRON).

On July 30, 2025, Altria Group, Inc. reported its financial results for the second quarter of 2025. The company posted adjusted earnings per share of $1.44, surpassing the analyst estimate of $1.38 and rising 8.3% year over year. Revenue came in at $6.1 billion, above the consensus estimate of $5.2 billion but down 1.7% compared to the same period last year. Net revenues were $6,102 million, with gross profit at $3,900 million and operating income at $3,200 million.

Net earnings stood at $2.4 billion, down from $3.8 billion in Q2 2024, impacted by a significant goodwill impairment in the e-vapor segment. Domestic cigarette volumes declined by 10.2%, but the smokeable products segment delivered solid adjusted operating company income growth, driven by the strength of Marlboro. In the oral tobacco products segment, the on! brand maintained momentum with strategic investments.

The company returned $4 billion to shareholders via dividends and buybacks, maintaining a 55-year dividend streak. Altria narrowed its full-year 2025 adjusted earnings guidance to $5.35 to $5.45 per share, raising the lower end and representing 3.0% to 5.0% growth from $5.19 in 2024.

The decline in the U.S. smoking rate continues, though it has recently recovered somewhat. In response to the negative long-term trend, Altria has invested heavily in new products that appeal to changing consumer preferences. They are also investing heavily in share repurchases to try to support continued earnings-per-share and dividend-per-share growth. Altria invested billions of dollars in Canadian marijuana producer Cronos Group for a 55% equity stake (including warrants) and a 35% equity stake in e-vapor manufacturer Juul Labs.

Related Articles About Altria on Dividend Power

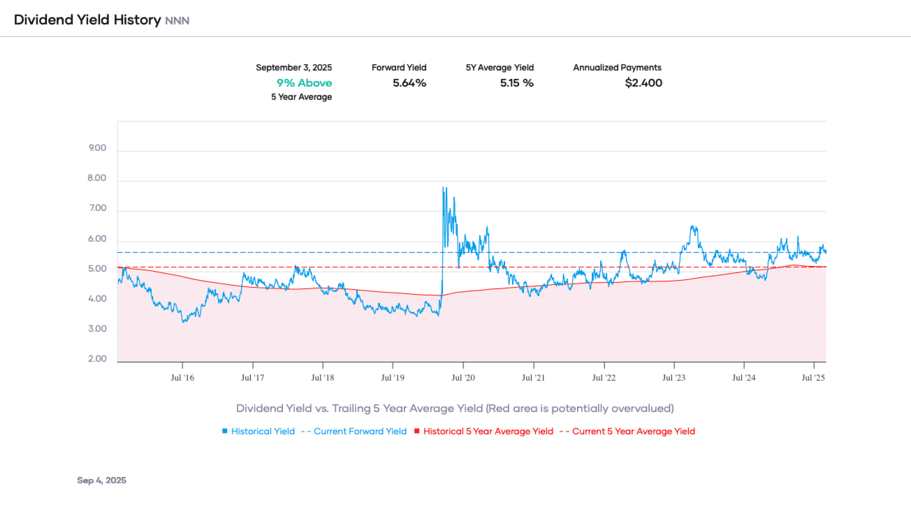

2: NNN REIT Inc. (NNN)

Dividend Yield: 5.7%

National Retail Properties is a REIT that owns single-tenant, net-leased retail properties across the United States. It is focused on retail customers because they are much more likely to accept rent hikes to avoid switching locations and losing their customer base.

Very high occupancy rates also characterize it; its 15-year low occupancy rate is 96%, and it typically ranges between 98% and 99%.

On July 30, 2025, NNN REIT reported results for the second quarter ended June 30, 2025, reflecting stable performance across its triple-net lease portfolio. Total revenue was $232.1 million, up from $221.5 million in the prior year, driven by rental income growth from new property acquisitions and contractual rent escalations. Net income attributable to common shareholders was $105.7 million, or $0.56 per diluted share, compared with $100.2 million, or $0.53 per share, in the second quarter of 2024.

Funds from operations, a key REIT metric, totaled $176.8 million, or $0.94 per share, slightly above the $0.92 per share reported a year earlier. Adjusted funds from operations were $171.5 million, or $0.91 per share, compared with $0.89 in the prior year, demonstrating steady cash flow growth. Portfolio occupancy remained exceptionally high at 99.2%, consistent with the company’s long-term stability.

During the quarter, NNN acquired 57 properties for approximately $274 million at an initial cash yield of 7.2%, expanding its retail-focused portfolio across diverse geographies. The company also sold 14 properties for $62 million, realizing modest gains while recycling capital into higher-yielding assets. The balance sheet remained strong with a net debt to EBITDA ratio of 5.3 times and liquidity of $1.3 billion, providing flexibility for future acquisitions. A quarterly dividend of $0.575 per share was declared, marking the 36th consecutive annual increase..

3: Franklin Resources (BEN)

Dividend Yield: 5.0%

Franklin Resources, founded in 1947 and headquartered in San Mateo, CA, is a global asset manager with a long and successful history. The company offers investment management, which makes up the bulk of the fees the company collects, and related services to its customers, including sales, distribution, and shareholder servicing.

As of June 30th, 2025, assets under management (AUM) totaled $1.612 trillion for the $12 billion market cap company.

On December 4th, 2024, Franklin Resources announced a $0.32 quarterly dividend, marking a 3% year-over-year increase and the company’s 45th consecutive year of increasing its payment.

On August 1st, 2025, Franklin Resources reported third-quarter 2025 results for the period ending June 30, 2025. Total assets under management equaled $1.612 trillion, up $71 billion sequentially, as a result of $78 billion of net market change, distributions, and other, and $2.7 billion of cash management net inflows, partly offset by $9.3 billion of long-term net outflows.

For the quarter, operating revenue totaled $2.064 billion, down 3% year-over-year. On an adjusted basis, net income equaled $263 million or $0.49 per share, down 18% from $0.60 in Q3 2024. During Q3, Franklin repurchased 7.3 million shares of stock for $157 million. Franklin ended the quarter with $5.9 billion in cash and investments.Franklin Resources has been acquiring alternative AUM through purchases such as Legg Mason, Lexington Partners, and Alcentra. It also closed its acquisition of Putnam Investments on January 1, 2024, which added $148 billion in assets to the company, which has since grown by approximately 20%.

Related Article on Franklin Resources on Dividend Power

Disclosure: No positions in any stocks mentioned.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Bob Ciura

Bob Ciura is President of Content at Sure Dividend. Bob has worked at Sure Dividend since October 2016. He oversees all content for Sure Dividend and its partner sites. Prior to joining Sure Dividend, Bob was an independent equity analyst. Bob received a bachelor’s degree in Finance from DePaul University, and an MBA with a concentration in Investments from the University of Notre Dame.