Equity markets have experienced elevated volatility throughout 2025, driven by persistent inflation, escalating geopolitical risks, and concerns about a potential recession stemming from tariffs.

Not all stocks are hit equally by equity market turmoil, however. Instead, some stocks tend to be more volatile than others due to their vulnerability to recessions.

On the other hand, some stocks remain resilient during these times due to their relatively low volatility. For an investor seeking to add stability to their portfolio, low-volatility stocks can be a solid choice.

In this report, we’ll showcase three stocks that combine low volatility with a high dividend yield, making them suitable for conservative income investors.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

3 Low Volatility Stocks with High Yields

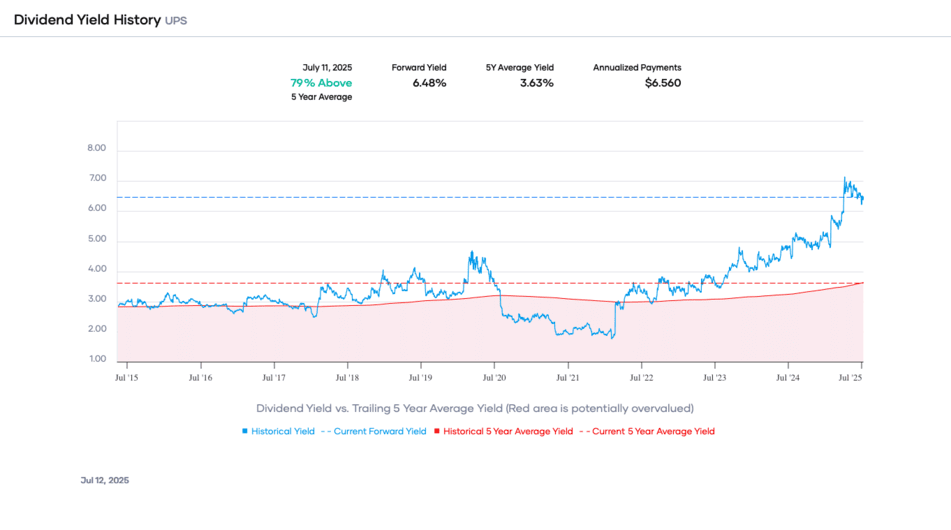

United Parcel Service, Inc. (UPS)

United Parcel Service, founded in 1907 and headquartered in Atlanta, GA, is a logistics and package delivery company that offers services including transportation, distribution, ground freight, ocean freight, insurance, and financing. Its operations are split into three segments: U.S. Domestic Package, International Package, and Supply Chain & Freight.

On April 29, 2025, UPS reported its first-quarter 2025 results for the period ended March 31, 2025. For the quarter, the company generated revenue of $21.5 billion, a 0.7% year-over-year decrease. The U.S. Domestic segment making up 67% of sales saw a 1.4% revenue increase, with International also posting a 2.7% revenue increase, while Supply Chain Solutions saw a 15% decrease. Adjusted net income equaled $1.49 per share, up 4.2% year-over-year.

With an uncertain economic landscape ahead, UPS is reducing costs to support its earnings growth. The company announced that it expects to reduce its headcount by approximately 20,000 in 2025 and close 73 buildings by the end of June. Through these initiatives, it expects to generate $3.5 billion of cost savings.

UPS also has growth initiatives in place. UPS has been experiencing a number of benefits in recent years. One such tailwind is e-commerce, which leads to growth in the number of packages that must be transported across the country. With online shopping continuing to outpace brick-and-mortar growth for the foreseeable future, UPS is expected to continue benefiting from strong demand for its services.

As an industry leader, the company has the ability to pay a high dividend and regularly raise it. UPS announced it increased its quarterly dividend by one penny to $1.64 on February 5th, 2024, marking its 16th consecutive annual increase. UPS stock currently yields 6.4%.

Related Articles About United Parcel Service

Flowers Foods (FLO)

Flowers Foods opened its first bakery in 1919 and has since become one of the largest producers of packaged bakery foods in the United States, operating 46 bakeries in 18 states. Well-known brands include Wonder Bread, Home Pride, Nature’s Own, Dave’s Killer Bread, Tastykake, and Canyon Bakehouse.

The company operates in two segments: Direct Store Delivery (DSD) and Warehouse Delivery, with ~85% of the company’s products being delivered directly to stores. Fresh breads, buns, rolls, and tortillas account for approximately three-fourths of the business, with sales channels split among supermarkets, Mass Merchandisers, Foodservice, and Convenience Stores.

On May 16, 2025, Flowers Foods reported first-quarter results for the period ended April 19, 2025. For the quarter, revenue decreased 1.4% to $1.55 billion, $50 million less than expected. Adjusted earnings-per-share of $0.35 compared to $0.38 last year and were $0.02 below estimates.

For the quarter, Branded Retail sales decreased 0.4% to $1.011 billion as pricing was lower by 0.9% and volume was down 1.9%. Simple Mills added 2.4%. Other sales declined 3.3% to $543 million, as a 0.4% benefit from pricing and mix was offset by a 3.7% decrease in volume.

FLO has increased its dividend for 22 consecutive years, making it a Dividend Contender. It has paid 91 consecutive quarterly dividends without interruption. FLO stock currently yields 6.3%.

T. Rowe Price Group (TROW)

T. Rowe Price Group, founded in 1937 and headquartered in Baltimore, MD, is one of the largest publicly traded asset managers. The company offers a diverse range of mutual funds, sub-advisory services, and separate account management for individual and institutional investors, retirement plans, and financial intermediaries. T. Rowe Price had assets under management (AUM) of nearly $1.6 trillion as of March 31st, 2025.

On May 2nd, 2025, T. Rowe Price reported first quarter results for the period ending March 31st, 2025. For the quarter, revenue grew 0.6% to $1.76 billion, though this was $20 million less than expected. Adjusted earnings-per-share of $2.23 compared unfavorably to $2.38 in the prior year, but this beat estimates by $0.10.

During the quarter, AUMs of $1.57 billion grew 1.9% year-over-year, but decreased 4.2% sequentially. Market depreciation of $37.1 billion and net cash outflows of $19.2 billion were partially offset by increases in money market and multi-asset inflows. Operating expenses of $1.17 billion increased 0.3% year-over-year, but declined 7.0% quarter over-quarter.

T. Rowe Price’s earnings, as well as its dividends, have grown substantially over the last decade. While earnings did drop in the previous financial crisis, the overall record has been solid. Since 2015, the company has grown earnings per share by an average compound annual rate of 8.1%.

Asset managers, such as T. Rowe, have low variable costs. As a result, higher revenues, driven primarily by increasing assets under management, allow for margin expansion and attractive earnings growth rates. Assets under management grow in two basic ways: increased contributions and higher underlying asset values. While asset values are volatile, the trend is upward over the long term.

On the contribution side, T. Rowe Price’s strong past performance is a key selling point and could attract customers going forward. In addition, T. Rowe has another earnings-per-share growth lever in the way of share repurchases.

TROW has increased its dividend for 39 consecutive years, and shares are currently yielding 5.4%. The firm is a Dividend Aristocrat.

Related Articles About T. Rowe Price

Disclosure: No positions in any stocks mentioned.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Bob Ciura

Bob Ciura is President of Content at Sure Dividend. Bob has worked at Sure Dividend since October 2016. He oversees all content for Sure Dividend and its partner sites. Prior to joining Sure Dividend, Bob was an independent equity analyst. Bob received a bachelor’s degree in Finance from DePaul University, and an MBA with a concentration in Investments from the University of Notre Dame.