Summary

- In mid FY2020 Genuine Parts Company (GPC), a Dividend King, divested itself of its underperforming Business Products group. GPC is now focused on its faster growing and higher margin automotive and industrial businesses.

- Through various initiatives GPC’s FY2020 Free Cash Flow far exceeded historical levels. This is not sustainable, and we should be prudent when trying to determine GPC’s valuation using FCF.

- GPC incurred restructuring charges and a sizable non-cash Goodwill impairment charge which resulted in a FY2020 GAAP loss.

- GPC’s current valuation based on adjusted earnings guidance and a reasonable FCF/share level suggests shares are currently overvalued.

Introduction

Toward the end of July 2017 I initiated a 300 share position in Genuine Parts Company (GPC), a Dividend King, in one of the ‘Core’ accounts within the FFJ Portfolio and have subsequently automatically reinvested all quarterly dividends.

This distributor of automotive replacement parts and industrial parts and materials operates in the United States, Canada, France, the United Kingdom, Germany, Poland, the Netherlands, Belgium, Australia, New Zealand, Mexico, Indonesia, and Singapore.

With GPC having released Q4 and FY2020 results and FY2021 guidance on February 17, 2021 I now take this opportunity to analyze results and guidance to determine whether I should add to my position.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

Business Overview of Genuine Parts Company – A Dividend King

I, as a long-term investor desiring to hold positions in high quality companies for the long-term, want to know about the companies in which I invest before initiating a position. I have found that reviewing the ‘Business’ and ‘Risk Factors’ sections of a company’s 10-K is a wonderful source of information and I provide this link to GPC’s 2020 10-K if you wish to learn about this company.

A Factsheet about GPC and information about its footprint and its history can be accessed here.

GPC consists of two groups: Automotive Parts and Industrial Parts. Prior to mid 2020, it had a third group, Business Products, but this was deemed to be a non-core part of the company. In fact, Net Sales from this group in FY2014 -2019 made up 11%, 13%, 13%, 12%, 10%, and 9% of Total Annual Net Sales.

Following a strategic review, the Board of Directors and Senior Management deemed the divestiture of this group (S.P. Richards) to be the best course of action. In mid-June 2020, GPC announced that it had completed the sale of the Business Products group as part of the plan to streamline operations and to optimize the portfolio. The focus is now on opportunistically expanding GPC’s global footprint and strengthening the focus on sustainable, value-driving initiatives associated with the faster growing and higher margin automotive and industrial businesses.

Earnings Results, Guidance, and Free Cash Flow

Q4 and FY2020 Results

GPC’s Q4 and FY2020 results and FY2021 guidance can be accessed here.

Looking at these results we see that in accordance with GPC’s 2019 $0.1B cost savings plan, the company achieved the $0.1B annual target. It also reported an incremental $40 million in savings in Q4 and $0.15B in permanent expense reductions for FY2020. In addition, a number of additional savings initiatives were implemented in response to the impact of COVID-19 which contributed temporary cost savings of ~$40 million in Q4 and ~$0.3B for FY2020. Altogether, GPC generated ~$80 million in total savings during Q4 and ~$0.45B for FY2020.

In Q4, GPC repaid $0.23B of debt and total debt of $2.7B as of December 31, 2020 is down $0.749B from $3.4B in 2019. GPC also further improved its debt position in Q4 with new public debt and a new revolving credit agreement that provided for expanded credit capacity and more favorable rates. As at FYE 2020, GPC has ~$2.9B of available liquidity versus $1.3B as at FYE2019.

FY2021 Guidance

In 2021 within the Global Automotive Group, GPC plans to continue to execute on several global initiatives and to invest in its B2B and B2C omnichannel strategy, to enhance and build new digital catalog and search capabilities, implement strategic pricing initiatives, focus on value-added services and continue the rollout of the NAPA brand in Europe and Australasia.

Plans are to expand the global store footprint with additional bolt-on acquisitions, changeovers and new stores to enhance the company’s competitive positioning across its automotive operations. These initiatives are designed to deliver customer value, sell more parts and capture market share.

Management has indicated that improving product availability, colder winter weather in North America and Europe and the gradual reopening up the economy are tailwinds for its automotive business. It is also cautiously optimistic that favorable industry fundamentals, a growing total vehicle fleet, an increase in vehicles aged 6 – 12 years, and expectation for the gradual recovery in miles driven will help the company meet FY2021 growth expectations despite the ongoing uncertainties due to COVID-19.

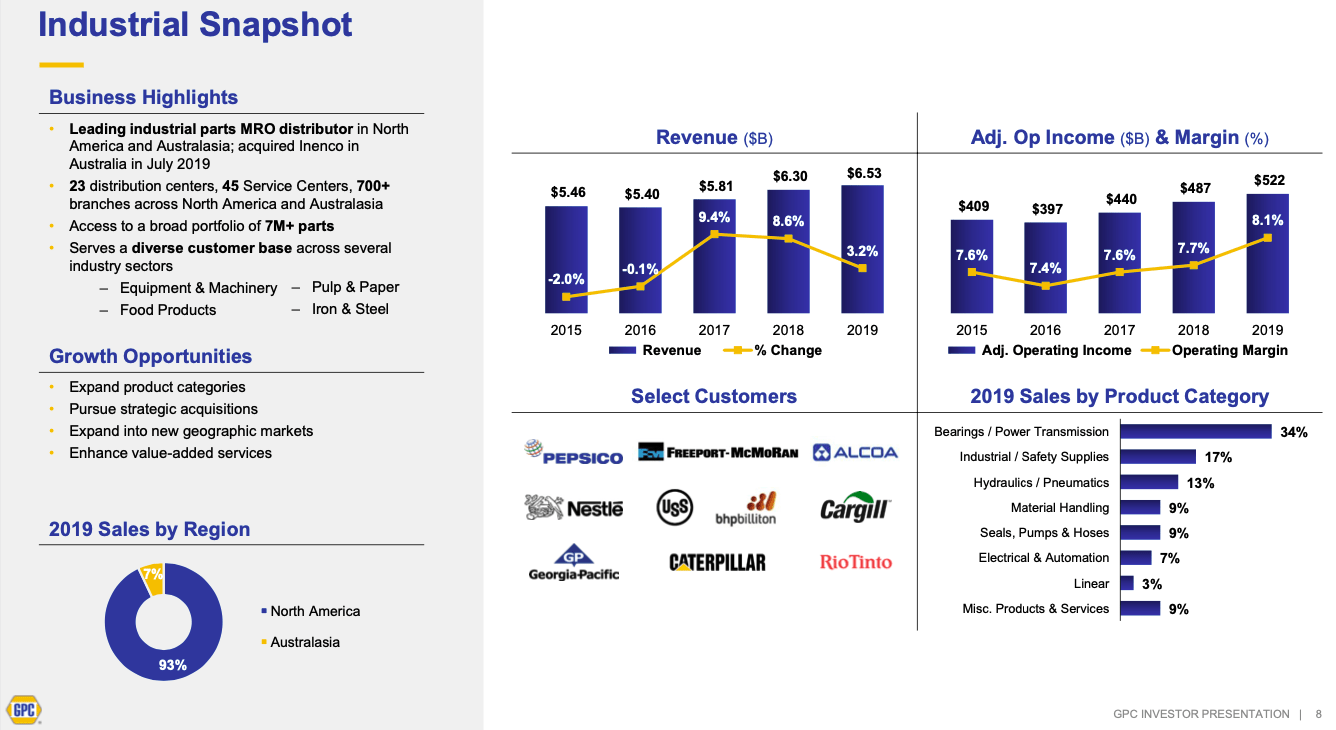

Within the Industrial Parts Group there has been a gradual improvement in the industrial economy. Strengthening conditions together with GPC’s ongoing initiatives to drive growth and lower costs resulted in a 70 bps improvement in segment profit margin and the strongest quarterly return on sales since the Q4 2007.

Q4 and full year gains represented the 13th consecutive quarter and the 5th consecutive year of improved gross margin. This improvement in gross margin is attributed the favorable impact of sales mix shifts to higher gross margin operations, positive product mix shifts, strategic pricing tools and analytics, global sourcing advantages and strategic category management initiatives. Acquisitions and divestitures also impacted results through the last 9 months of the year.

Free Cash Flow (FCF)

I view FCF as a critical metric when analyzing a company because this represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. Unlike net income, free cash flow is a measure of profitability that excludes the non-cash expenses of the income statement and includes spending on equipment and assets as well as changes in working capital from the balance sheet.

In the 2011 – 2020 timeframe, GPC generated roughly (in millions of USD) 521, 804, 933, 682, 1050, 785, 658, 919, 614, and 1866 in FCF. I arrived at these levels by looking at the Consolidated Statements of Cash Flows (page 46 in the FY2020 10-K) and using the net cash provided by operating activities, the purchases of property, plant and equipment, proceeds from sale of property, plant and equipment, and the net cash (used in) provided by discontinued operations.

While GPC’s valuation based on FY2020 FCF looks appealing I do not think this is representative of what we can expect going forward. FY2020 was truly different from prior years in that GPC generated $1.866B in FCF because of initiatives it undertook as a result of the COVID-19 pandemic. While some of these initiatives were permanent in nature, there was also a good portion that was precautionary and temporary.

I think annual FCF within the $0.8B – $1B range might be more realistic in FY2021.

Genuine Parts Dividend Growth, Dividend Yield, Credit Rating, and Share Repurchases

Dividend Growth and Dividend Yield of Genuine Parts Company – A Dividend King

Genuine Parts Company prides itself on its track record as a Dividend King which is defined as a company with 50 or more consecutive years of dividend increases. The company is also a Dividend Aristocrat.

The company’s website has a graph which depicts the growth in the company’s dividend over time. Surprisingly, however, one must look to external websites (see here and here) to gather more details; even these external sites do not show the complete 65 year history.

On February 16, 2021, GPC declared a $0.815/quarter/share dividend payable to shareholders on April 1st. Genuine Parts Company increased the quarterly dividend by ~3.16% from the prior $0.79 quarterly dividend making this the 65th consecutive annual increase for the Dividend King.

The following is a snapshot of GPC’s compound annual growth rate of its dividend over two different time frames.

The growth rate over these two arbitrarily determined time frames is reasonably similar and we see that the growth rate is distorted by a few years where the annual growth rate was in the 8 – 10% range. The trialing growth rate over the past 40-years was ~7% CAGR with the annual dividend increasing from $0.21 per share in 1980 to $3.16 per share in 2020. Genuine Parts target a payout ratio of 50% to 55%. The forward payout ratio is 56.7%

On the basis of the current $109.20 share price, GPC’s $3.26 FY2021 dividend provides investors with a ~3% dividend yield. This is near the trailing 5-year average of about 3.1% based on StockRover* before taking into consideration any withholding tax that may be incurred if you are a shareholder who resides outside the US and shares are held in a taxable account. Notably, the Genuine Parts was yielding over 5% during the nadir of the COVID-19 pandemic market downturn.

Credit Ratings

As an investor who acquires common stock, I know that I rank last in the ‘pecking order’ in the event of restructuring or liquidation. As a result, I like to look at how the major credit ratings agencies view a company’s debt. If they deem the company’s debt to be non-investment grade, then I very seriously need to determine whether I want to assume the risk associated with a company whose debt has a higher degree of vulnerability of default than companies whose debt is defined as investment grade.

In October 2020, Moody’s and S&P Global initiated coverage and assigned a rating to GPC’s unsecured long-term debt.

Moody’s has assigned a Baa1 rating and S&P Global has assigned a BBB rating.

Moody’s rating is the top tier of the lower medium grade while S&P Global’s rating is 1 notch lower and is the middle tier of the lower medium grade. Both ratings are investment grade and are defined as an obligor having ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

Both ratings are satisfactory for my purposes.

Share Repurchases

GPC has reduced the weighted average number of shares outstanding in 2011 – 2020 as follows (in millions): 158, 156, 156, 154, 152, 150, 148, 147, 146, and 145.

On August 21, 2017, GPC’s Board of Directors announced that it had authorized the repurchase of 15 million shares. The authorization for these repurchases plans continues until all such shares have been repurchased or the repurchase plan is terminated by action of the Board of Directors.

In 2020, GPC repurchased 1.1 million shares of common stock prior to suspending share repurchases amid the pandemic. As of December 31, 2020, GPC was authorized to repurchase up to 14.5 million additional shares and management has indicated it expects to make additional opportunistic share repurchases again in 2021.

Valuation of Genuine Parts Company – A Slightly Overvalued Dividend King

I initiated my GPC position in July 2017 at which time shares were trading at $82.71. The mean FY2017 adjusted EPS projections from various brokers was $4.75 and $5.15 for FY 2018. On the July 20, 2017 Q2 conference call with analysts, management indicated the full year adjusted diluted EPS outlook had been revised downward to $4.70 – $4.75 from its previous guidance of $4.75 – $4.85.

I decided to err on the side of caution and used an annual adjusted diluted EPS of $4.70 for the purpose of my calculations. Using the $82.71 share price I arrived at an adjusted diluted PE of ~17.60 for FY2017 and using the forecast FY2018 mean adjusted diluted EPS of $5.15 I arrived at a projected PE of ~16.06. I viewed these levels as acceptable (although a bit on the high side) for the purposes of initiating a position in GPC.

We now find ourselves with GPC trading at $109.20 and negative FY2020 earnings because of a ~$0.5B goodwill impairment charge (a non-cash charge) and ~$50 million in restructuring costs for a total of $0.55B in non-recurring expenses (see page 43 of GPC’s FY2020 10-K). Having reported a loss in FY2020, calculating a PE based on GAAP earnings is impossible.

We also see $0.1B in restructuring costs and ~$43 million of special termination costs in FY2019. Clearly, these expenses have impacted GPC’s GAAP results. I am, therefore, using adjusted earnings as it is unlikely these expenses will be incurred again in FY2021.

GPC’s FY2021 adjusted diluted EPS guidance is $5.55 – $5.75. Using the current $109.20 share price we get a forward adjusted diluted PE range of ~19 – ~19.7.

One of my sources reflects FY2021 mean, low, and high adjusted diluted EPS guidance from 12 brokers of $5.72 and $5.49 – $5.90. Using this information, I get a mean adjusted diluted PE of ~19 and a ~18.51 – ~19.9 range.

Although GPC has narrowed its focus on sustainable, value-driving initiatives associated with the faster growing and higher margin automotive and industrial businesses, I think an adjusted diluted PE of ~16 and below is a more appropriate valuation at which to acquire shares. On this basis and using the mean $5.72 guidance from analysts and the $5.65 mid-point of GPC’s guidance, a price in the low $90s is a level I think is a fairer representation of GPC’s current value.

My sources of historical information reflect GPC’s Price/FCF during the 2011 – 2020 timeframe of ~16, ~11, ~13.3, ~20.4, ~12, ~14.3, ~18.9, ~12, ~16, and ~9.

The weighted average number of diluted shares outstanding in FY2018 – FY2020 was (in millions) 147,241, 146,417, and 145,115. If the number of outstanding shares declines by ~1 million in FY2021 we end up with ~144,115 million outstanding. Using the $0.9B mid-point of the FY2021 FCF range I anticipate then we get ~$6.24 FCF/share. I think a P/FCF of ~15ish is more a realistic multiple. This suggests ~$93 is a fairer share price than the current $109.20.

Final Thoughts on Genuine Parts Company – A Slightly Overvalued Dividend King

Disregarding a company’s valuation and overpaying to acquire shares is a recipe for poor investment returns. In my opinion, we are currently witnessing market conditions in which the share price of many companies has become somewhat detached from the underlying fundamentals and growth prospects.

Although GPC has successfully shed itself of its underperforming Business Products Group and can now focus on its faster growing and higher margin automotive and industrial businesses, I think GPC’s valuation based on FY2021 guidance is slightly rich. I would like to see GPC’s share price drop to the low $90s from the current $109.20 before I would consider adding to my position.

Stay safe. Stay focused.

I wish you much success on your journey to financial freedom.

Thanks for reading, “Genuine Products Company – A Slightly Overvalued Dividend King!”

Disclosure: I am long GPC.

Author Disclosure: I disclose our holdings which are held in the FFJ Portfolio and the dividend income generated from these holdings but for confidentiality reasons do not disclose details of holdings held in various tax advantaged accounts.

Author Disclaimer: I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article. I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Here are my recommendations:

If you are unsure on how to invest in dividend stocks or are just getting started with dividend investing. Take a look at my Review of the Simply Investing Report. I also provide a Review of the Simply Investing Course. Note that I am an affiliate of Simply Investing.

If you are interested in an excellent resource for DIY dividend growth investors. I suggest reading my Review of The Sure Dividend Newsletter. Note that I am an affiliate of Sure Dividend.

If you want a leading investment research and portfolio management platform with all the fundamental metrics, screens, and analysis tools that you need. Read my Review of Stock Rover. Note that I am an affiliate of Stock Rover.

If you would like notifications as to when my new articles are published, please sign up for my free weekly e-mail. You will receive a free spreadsheet of the Dividend Kings! You will also join thousands of other readers each month!

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

I am a self-taught investor and run the Financial Freedom is a Journey blog. I have invested in the North American equities markets for over 34 years. I retired from a career in banking and continue to invest as this is something about which I am passionate.

Nice sharing for people who are working on food niches!