I am all in favour of investing in high-quality companies when they have fallen out of favour. However, there reaches a point where the risk/reward trade-off is insufficiently attractive. Based on my analysis, 3M (MMM) is a toxic Dividend King to avoid.

NOTE: Dividend Kings are members of the S&P 500 that have increased their dividends for at least 50 consecutive years. In February 2022, MMM increased its quarterly dividend for the 64th consecutive year! Don’t get excited. In the Dividend and Dividend Yield segment of this post, we will see that even this is not good news!

I last reviewed MMM in my February 14, 2022 3M: This Dividend King Is A Train Wreck post at Financial Freedom Is A Journey. In that post, I disclosed my exit from this holding.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

In multiple posts, I express concern about the heavy reliance some investors place on dividend metrics as part of their investment decision-making process. These metrics are unreliable but because they are readily available, many investors rely on them.

MMM is a good example of a company with appealing dividend metrics with a high probability of generating a poor long-term total investment return.

Before delving into why 3M (MMM) is a toxic Dividend King to avoid, I highly encourage you to read Item 8, Note 16 – Commitments and Contingencies (pages 97 – 116) within MMM’s FY2021 Form 10-K. This section provides information regarding legal proceedings for which MMM potentially faces massive costs if they lose. In addition to the potential for sizable losses, investors may wish to consider the magnitude of MMM’s annual legal expenses and the internal costs related to defending the company from all these claims! Consequently, we view 3M as a toxic Dividend King to avoid.

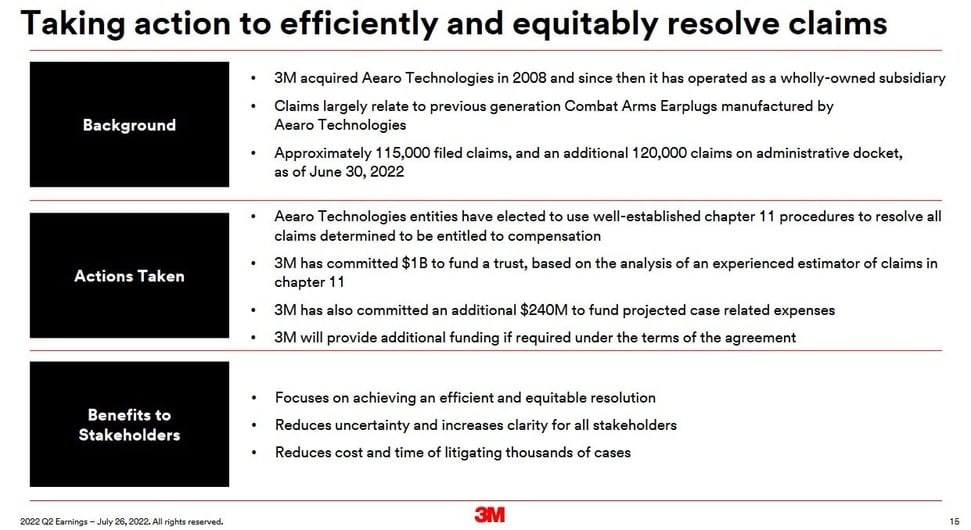

Ear Plug Litigation

An overview of MMM’s Dual-Ended Combat Arms earplugs product liability litigation commences on page 114 of 161 in the FY2021 Form 10-K.

The following, prepared BEFORE the United States Bankruptcy Court in the Southern District of Indiana declined Aearo Technologies’ request for a preliminary injunction to ongoing litigation against MMM related to Combat Arms Earplug Version 2 products, provides a very high-level overview of this litigation.

Following the Bankruptcy Court’s decision, MMM issued this Press Release:

‘Earlier today, the United States Bankruptcy Court in the Southern District of Indiana declined Aearo Technologies’ request for a preliminary injunction to ongoing litigation against 3M related to Combat Arms Earplug Version 2 products.

Aearo Technologies and 3M disagree with the ruling and Aearo intends to appeal the decision. Aearo will continue in the chapter 11 proceedings, which it believes will offer a more efficient, equitable and expeditious pathway to resolution of these matters for all parties. 3M also will continue to vigorously defend its position in the multi-district litigation and in its appeals in that litigation.’

Source: MMM – August 26, 2022 Press Release

To give investors some context as to the magnitude of this lawsuit, MMM was a named defendant in ~3,616 lawsuits (including 14 putative class actions) in various state and federal courts that purport to represent ~13,531 individual claimants making similar allegations as of FYE2021 (December 31, 2021).

Respirator Mask/Asbestos Litigation

As of December 31, 2021, MMM is also a named defendant, with multiple co-defendants, in numerous lawsuits in various courts that purport to represent ~3,876 individual claimants, compared to ~2,075 individual claimants with actions pending on December 31, 2020.

The current volume of new and pending matters is substantially lower than at the peak of filings in

2003. The Company expects that filing of claims by unimpaired claimants in the future will continue to be at much lower levels than in the past. Accordingly, the number of claims alleging more serious injuries, including mesothelioma, other malignancies, and black lung disease, will represent a greater percentage of total claims than in the past.

MMM has prevailed in many lawsuits over the past couple of decades. The remaining lawsuits, however, carry far greater potential for significant losses.

Having said this, judicial systems do not always rule in favour of the party who has been harmed. MMM has far deeper pockets than the plaintiffs. It can tie matters up in court to the point where the plaintiffs give up for a variety of reasons. Even though MMM might truly be guilty, there is no assurance the cases will conclude any time soon or that MMM’s losses will be significant.

‘Forever Chemicals’ Litigation

If the aforementioned litigation issues do not raise concerns, then consider that MMM also faces another wave of litigation with a multitude of cases tied to its past production of so-called ‘forever chemicals’.

The Company’s operations are subject to environmental laws and regulations including those pertaining to air emissions, wastewater discharges, toxic substances, and the handling and disposal of solid and hazardous wastes enforceable by national, state, and local authorities around the world, and private parties in the United States and abroad. These laws and regulations provide, under certain circumstances, a basis for the remediation of contamination, for capital investment in pollution control equipment, for restoration of or compensation for damages to natural resources, and for personal injury and property damage claims. The Company has incurred, and will continue to incur, costs and capital expenditures in complying with these laws and regulations, defending personal injury and property damage claims, and modifying its business operations in light of its environmental responsibilities. In its effort to satisfy its environmental responsibilities and comply with environmental laws and regulations, the Company has established, and periodically updates, policies relating to environmental standards of performance for its operations worldwide.

Source: MMM – 2021 Form 10-K (page 100 of 161)

These lawsuits are related to MMM’s past manufacturing of certain per- and polyfluoroalkyl chemicals, collectively known as PFAS. According to Bloomberg Intelligence, settlements in those cases could total as much as $20B.

Pension and Postretirement Benefit Plans

MMM has company-sponsored retirement plans covering substantially all US employees and many employees outside the US. In total, MMM has over 75 defined benefit plans in 28 countries.

On a worldwide basis, MMM’s pension and postretirement plans were 93% funded at FYE2021. The primary US-qualified pension plan, which is ~67% of the worldwide pension obligation, was 97% funded and the international pension plans were 101% funded. The U.S. non-qualified pension plan is not funded due to tax considerations and other factors.

MMM expects to contribute ~$0.1B – ~$0.2B of cash to its global defined benefit pension and

postretirement plans in 2022.

Details of MMM’s pension plans and their end-of-year Benefit Obligations, Funded Status, and the changes in both from one year to another are in the Notes within every Form 10-K.

The low-interest-rate environment for the last several years has placed pressure on many defined benefit pension plans. This is because the returns generated from the assets held in these pension plans generate insufficient returns to offset the disbursement obligations.

Higher interest rates help improve the performance of defined pension plans. The forecasted rate increases might, however, be insufficient to eliminate the need for MMM to make further contributions to narrow their shortfall gap.

MMM pensioners might not need to worry…for now. If MMM ultimately has to make additional sizable contributions to the pension plans, however, it might find itself in a predicament if the outcomes of its legal issues are unfavourable.

Proposal To Spin-Off Healthcare Business

On July 26, 2022, MMM announced its intent to spin off its Health Care business; the target completion date is the end of 2023.

It is far too early to comment on this proposed spin-off. However, looking at the expected net leverage at the time of the spin-off, I expect the domestic unsecured long-term debt credit ratings will be lower than MMM’s current ratings. In essence, MMM shareholders who elect to accept shares in the new company will be taking on greater risk.

Interestingly, within the past several days, a lawsuit against MMM has been launched by 2 U.S. military veterans to block the planned spinoff of MMM’s healthcare business. These veterans claim the planned spinoff is an illegal attempt to avoid compensating veterans for hearing damage caused by the company’s military-issue earplugs.

The lawsuit filed in federal court in Pensacola, Florida, states that the spinoff was ‘little more than a formalism’ intended to ‘wall off’ assets, violating a Florida law barring debtors from fraudulently transferring assets to shield them from creditors.

Expectations are for this case to go before U.S. District Judge M. Casey Rodgers, who is already overseeing more than 220,000 lawsuits over the earplugs and has been harshly critical of MMM’s legal strategy. Whether this healthcare business spin-off does occur remains to be seen. In any case, it is another reason why 3M is a toxic Dividend King to avoid.

Separation of Food Safety Business

On September 1, 2022, MMM completed its split-off exchange offer for MMM common stock in connection with the previously announced separation of its food safety business; refer to the Press Release regarding the closing of the merger of Garden SpinCo Corporation (‘SpinCo’), the 3M subsidiary holding the food safety business, with a subsidiary of Neogen Corporation (NEOG).

Under the terms of the spin-off, MMM shareholders had the opportunity to receive shares in NEOG.

If you are a MMM shareholder who elected to accept NEOG shares, this is your credit risk:

- On July 5, 2022, Moody’s issued a ‘Rating Action’ in which it assigned a B2 rating to Garden SpinCo Corporation’s proposed offering of $350 million in senior unsecured notes. It made no change to the company’s Ba3 Corporate Family Rating, the Ba3-PD Probability of Default Rating, or the Ba2 rating assigned to the company’s senior secured credit facilities.

- On May 27, 2022, S&P Global assigned a BB+ rating to NEOG’s domestic unsecured long-term debt.

The rating assigned by Moody’s is the bottom tier of the Non-investment grade speculative category. S&P Global’s rating is the top tier of the Non-investment grade speculative category. Despite the two-tier difference, both ratings define NEOG as being less vulnerable in the near term than other lower-rated obligors. However, it faces major ongoing uncertainties and exposure to adverse business, financial, or economic conditions which could lead to an inadequate capacity to meet its financial commitments.

Investors in NEOG’s common stock, however, face a greater risk than the unsecured long-term debt holders. If you own shares in NEOG, your risk is highly speculative.

Layoffs

Very recently, an internal memo from the head of MMM’s safety and industrial division warned employees of potential workforce cuts ahead. These cuts are part of a broader series of moves to control expenses amid the growing risk of a slowing economy.

Financial Review

Q2 and YTD2022 Results

Material related to MMM’s Q2 and YTD2022 results is accessible here.

A good portion of MMM’s Q2 2022 Earnings Release and Presentation makes assumptions about:

- MMM’s success regarding Chapter 11 proceedings to resolve current and future Combat Arms Earplugs Version 2 litigation; and

- a successful tax-free spin-off of Health Care into a standalone publicly-traded company.

We now know that the Chapter 11 proceedings have, to date, not gone according to plan. Furthermore, within the past several days, a lawsuit against MMM has been launched by 2 U.S. military veterans to block the planned spinoff of MMM’s healthcare business. Depending on the outcome of this lawsuit, the proposed tax-free spin-off of Health Care may not be possible or it could be delayed.

Credit Ratings

MMM has taken roughly two decades to destroy its credit rating; its AAA senior unsecured long-term domestic credit rating has fallen 4 tiers! By comparison, General Electric (GE) was far more successful in destroying its credit rating. It was able to knock back its AAA credit rating by 7 tiers in a shorter timeframe. Well done GE!

In February 1998, Moody’s downgraded MMM’s domestic senior unsecured credit rating from AAA to Aa1. It appears management was not satisfied with this downgrade. Now MMM’s domestic unsecured long-term debt ratings are:

- Moodys’: A1

- S&P Global: A+

It gets better!

In July 2022, S&P Global placed MMM’s A+ rating on CreditWatch with negative implications.

Surprisingly, I see no mention of Moody’s placing MMM’s credit ratings under review with negative implications. However, on July 26, Moody’s announced that MMM’s planned spinoff of its health care segment is credit negative. Furthermore, on August 24, Moody’s announced that MMM’s deleveraging is overshadowed by environmental and litigation risks.

I am at a loss as to why Moody’s does not have MMM’s ratings on Watch with negative implications. Perhaps the recent decision by the United States Bankruptcy Court in the Southern District of Indiana regarding the ear plug litigation will prompt Moody’s to place MMM’s ratings under review with negative implications.

I mention this because on August 31, 2022, S&P Global affirmed that the A+ rating is still under review with negative implications given the announcement that the United States Bankruptcy Court in the Southern District of Indiana declined MMM’s wholly owned subsidiary Aearo Technologies’ request for a preliminary injunction related to litigation against 3M Co. and its Combat Arms Earplug Version 2 products.

While Aero Technologies is appealing the decision and will continue with chapter 11 proceedings, the lawsuits against MMM will be allowed to continue.

The current ratings are the top tier of the upper-medium-grade investment-grade category. They define MMM as having a strong capacity to meet its financial commitments. However, MMM is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

MMM’s ratings would have to drop 6 tiers before they reach junk territory. However, investors might want to ask if the risk/potential reward is worth it. There is a reasonable probability of a broad market correction in the not-too-distant future. Why take on MMM risk when there are many far superior companies in which to invest?

Dividends and Share Repurchases

Dividend and Dividend Yield

Earlier in this post, I indicate that 64 consecutive years of dividend increases is no reason for excitement. Looking at MMM’s dividend history, there are several years of negligible dividend increases. The perception is that MMM is desperately attempting to prolong its record of annual dividend increases.

Most recently, MMM’s Board declared a Q1 2022 dividend of $1.49/share (up from $1.48 and $1.47 in 2021 and 2020). MMM’s dividend increases are not keeping pace with inflation!

With shares currently trading at $121.65, the $1.49 quarterly dividend yields ~4.9%.

In MMM, we have a company with a lengthy track record of dividend increases and an attractive dividend yield. However, MMM’s average annual total return over 20 years is only 6.54% if dividends are reinvested and 5.97% when dividends are not reinvested. In contrast, the S&P500 return is 9.78% and 8.65%.

Change the timeframe to 10 years, and the returns are 6.20% and 6.55% versus S&P returns of 13.02% and 12.16%. Typically, we would expect to see a superior return under the dividend reinvestment scenario. This is not the case with MMM.

Naturally, historical rates of return differ depending on the start and stop dates. I, therefore, encourage you to access this site and adjust start and stop dates to gauge MMM’s historical performance over different timeframes. In the vast majority of scenarios, MMM’s historical returns are abysmal.

This is why I repeatedly state that heavy reliance on dividend metrics is unwise.

Related Article About 3M on Dividend Power

Share Repurchases

In November 2018, MMM’s Board replaced the Company’s February 2016 repurchase program with a new $10B repurchase program with no pre-established end date. As of June 30, 2022, ~$4.8B remained available under the authorization.

The share count (in millions of shares outstanding) is 703, 694, 662, 637, 619, 613, 602, 585, 582, and 585). For the 3 months ending June 30, 2022, the diluted weighted average common shares outstanding was 572.7.

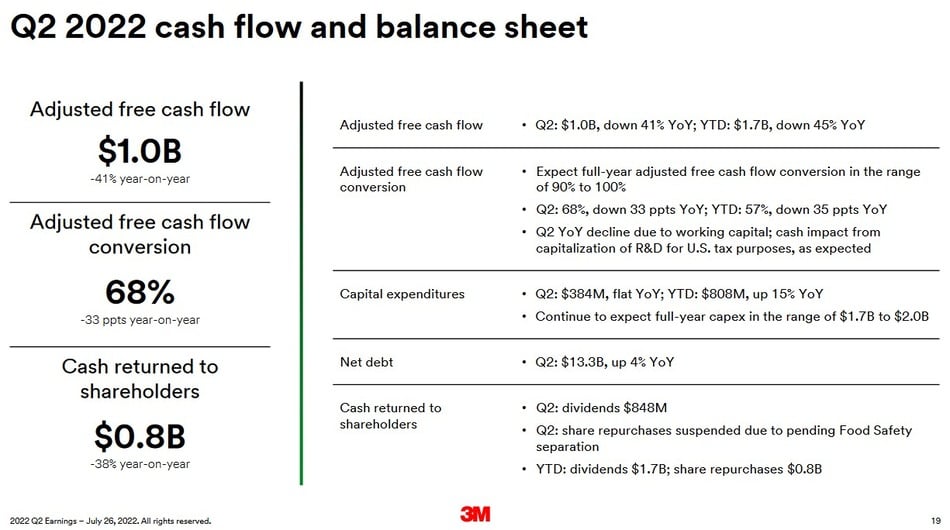

In the first 6 months of FY2022, MMM purchased $0.773B of its stock, compared to

$0.734B in the first 6 months of FY2021.

While MMM’s FY2012 – FY2021 share count trend might look ‘okay’, MMM has destroyed shareholder value by way of its share repurchases.

Keep in mind MMM’s current share price of ~$121.65. Using MMM’s historical Form 10-K reports, we see it repurchased several million shares at prices well above the current share price.

- 2014 – repurchased 40.235 million shares @ an average price of $138.92

- 2015 – repurchased 33.666 million shares @ an average price of $155.56

- 2016 – repurchased 22.164 million shares @ an average price of $164.04

- 2017 – repurchased 9.879 million shares @ an average price of $201.13

- 2018 – repurchased 23.289 million shares @ an average price of $207.46

- 2019 – repurchased 7.311 million shares @ an average price of $181.22

- 2020 – repurchased 2.045 million shares @ an average price of $156.29

- 2021 – repurchased 11.65 million shares @ an average price of $185.92

Valuation

When I wrote my February 14, 2022 post, management’s FY2022 adjusted diluted EPS outlook was $10.15 – $10.65. Using the current ~$157 share price and the ~$10.40 mid-point of guidance, the forward adjusted diluted PE was ~15.

I expected revisions over the coming days to the adjusted diluted EPS guidance from the brokers which cover MMM. Based on the current estimates, however, the following was the forward valuation.

- FY2022 – 20 brokers: $10.36 mean and $9.83 – $10.85 range. The valuation using the mean is ~15.2.

- FY2023 – 18 brokers: $11.07 mean and $10.51 – $11.52 range. The valuation using the mean is ~14.2.

- FY2024 – 10 brokers: $11.82 mean and $11.12 – $12.19 range. The valuation using the mean is ~13.3.

Shares are now trading at $121.65 and the valuations based on the forward adjusted diluted earnings estimates are:

- FY2022 – 20 brokers: $10.38 mean and $10.16 – $10.50 range. The valuation using the mean is ~11.7.

- FY2023 – 20 brokers: $10.87 mean and $10.39 – $11.68 range. The valuation using the mean is ~11.2.

- FY2024 – 9 brokers: $11.21 mean and $10.01 – $11.85 range. The valuation using the mean is ~10.85.

Management’s most recent adjusted diluted EPS earnings estimate for FY2022 is $10.30 – $10.80. With shares trading at $121.65, the forward adjusted diluted PE range is ~11.3 – ~11.8.

Investors, however, should view MMM’s adjusted diluted EPS earnings estimate with caution. The estimated range was provided when Q2 2022 results were released on July 26, 2022. Following the recent unfavourable Chapter 11 outcome, the range in broker estimates is lower than what MMM communicated just over a month ago. Furthermore, the unfavourable Chapter 11 outcome was publicly disclosed just a few days ago. Some brokers are likely revisiting their earnings estimates. In fact, based on the earnings estimates reflected on two discount brokerage platforms I use, some estimates have been revised lower in the last couple of days. In addition, the number of brokers who have provided estimates is lower than just a few days ago.

Some investors may argue that MMM’s low valuation offsets some of the litigation risks.

I respectfully disagree.

3M (MMM) is a toxic Dividend King to avoid. The company is contracting (stagnant at best) and it faces many significant headwinds and legal challenges. It is widely followed by the investment community and were the risks insignificant, MMM’s valuation would likely be higher. In my opinion, this low valuation is no reason to invest in MMM.

3M (MMM) – A Toxic Dividend King To Avoid – Final Thoughts

When MMM’s current CEO took the helm on July 1, 2018, shares were trading just shy of $200. Shares are now trading at $121.65.

MMM is essentially one of the worst performers in the S&P 500 index of industrial companies; Bloomberg Intelligence estimates MMM’s valuation relative to its manufacturing peers implies a discount of about $33B tied to the legal battles.

In my opinion, 3M (MMM) is a toxic Dividend King to avoid. Even if there was no growing risk of a slowing economy, MMM’s legal challenges are far too significant.

If the tens (or hundreds) of millions MMM has incurred (and has yet to incur) in legal fees and internal expenses related to its legal issues do not result in a favourable outcome, it may be forced to take drastic measures. This might include having to raise debt, suspend share buybacks AGAIN (share repurchases remained suspended in Q2 due to the impending separation of the Food Safety Business), and smaller dividend increases.

With the increasing likelihood that 2023 will be a ‘challenging’ year, I strongly suggest investors restrict any investment to companies that do not face headwinds of the magnitude MMM faces.

Although there is always the possibility MMM could turn things around, its track record gives me little reason for optimism.

If you thought MMM is a ‘sleep-well-at-night’ investment, you may want to complete your own investment analysis. I did not like what I saw and eliminated my MMM exposure.

Author Disclosure: I do not have exposure to 3M (MMM) and most certainly have no intention of initiating a position. I disclose holdings held in the FFJ Portfolio and the dividend income generated from these holdings. I do not disclose details of holdings held in various tax-advantaged accounts for confidentiality reasons.

Author Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

I am a self-taught investor and run the Financial Freedom is a Journey blog. I have invested in the North American equities markets for over 34 years. I retired from a career in banking and continue to invest as this is something about which I am passionate.