In my recent Consider Blackstone For Alternative Asset Exposure post, I explain my rationale for investing in the world’s largest asset manager based on market capitalization. I also disclose a position in Brookfield Asset Management (BAM); my exposure also includes positions in publicly listed entities that fall under the BAM umbrella. While both are leaders in their own right, there is one significant difference between the two firms: Blackstone (BX) is asset light while BAM is asset heavy.

An ‘asset-light’ business model strategy has (relatively) little ownership of assets, i.e. only a small amount of fixed assets on the balance sheet. An ‘asset-heavy’ business model strategy is the opposite.

The difference between the two companies is readily apparent when you look at their respective Q1 2022 Balance Sheet.

BAX’s Total Assets at the end of Q1 2022 are ~$2.25B. BAM’s Total Assets, on the other hand, are ~$402B.

The best way to understand why BAM differs from many of its peers is to listen to Brookfield CEO Bruce Flatt on Bloomberg Wealth with David Rubenstein. Around the 3 minute mark of the video, Bruce Flatt explains why BAM’s structure is different.

However, BAM’s ‘asset light’ model is about to change. After much speculation, Brookfield has announced its plan to become asset light.

The plan is to publicly list 25% of its asset-management business in a transaction that would value the new entity at US$80B. It expects to publicly distribute this 25% to shareholders before the end of 2022. This special distribution of shares will be around US$20B, or US$12/share.

In Bruce Flatt’s (CEO) Q1 2022 Letter to Shareholders, he explains the rationale and benefits of the spin-off.

Given this recent announcement and the release of Q1 2022 results, this is an opportune time to review BAM.

Affiliate

Take the Simply Investing Course to learn more about investing and dividends.

- Lifetime access with 27 self-paced lessons.

- Covers placing stock orders, building and tracking portfolios, when to sell, reducing fees and risk, etc.

- Learn the 12 Rule of Simply Investing

- Simply Investing Coupon Code – DIVPOWER15.

Industry Overview

Conventional investment categories include stocks, bonds, and cash. Alternative investment classes, however, are financial assets that do not fall into one of the conventional investment categories. Examples of alternative investments include private equity or venture capital, hedge funds, real property, commodities, and tangible assets.

The industry leaders typically leverage their deep operational expertise, global reach and access to large-scale capital and invest their capital alongside their investors. BAM, for example, does so in virtually every transaction thus aligning its interests with those of its investors.

From 2015 to the end of 2021, assets under management (AUM) across all alternative asset classes have increased at a CAGR of 10.7%. At the end of 2015, AUM stood at $7.23T versus $13.32T by the end of 2021. Some industry forecasts expect AUM growth to accelerate to exceed $22T by the end of 2026. Whether this is achievable is irrelevant. The takeaway is that AUM will continue to grow and well-established industry leaders stand to significantly benefit from this growth.

Expectations are for the entire industry to grow AUM at a double-digit rate; the larger alternative asset managers (eg. BAM, BX) are forecast to grow AUM at an even higher rate. A couple of reasons are:

- institutional investors plan to consolidate their relationships with alternative asset managers; and

- transactions sizes continue to grow significantly and the larger industry participants can raise far greater amounts of capital;

Alternative asset managers traditionally target institutional or accredited investors such as pension plans, endowments, foundations, sovereign wealth funds, financial institutions, and

insurance companies. However, in recent years they have identified a significant untapped market…retail investors.

Company Overview

At the end of Q1 2022, BAM had ~$725B of AUM across real estate, infrastructure, renewable power, private equity and credit. Its AUM, however, is growing rapidly given that it had ~$693B of AUM as recently as FYE2021 (December 31, 2021).

- ~$430B in North America

- ~$44B in South America

- ~$129B in Europe and the Middle East (BAM has no AUM in Russia and Ukraine)

- ~$85B in Asia Pacific

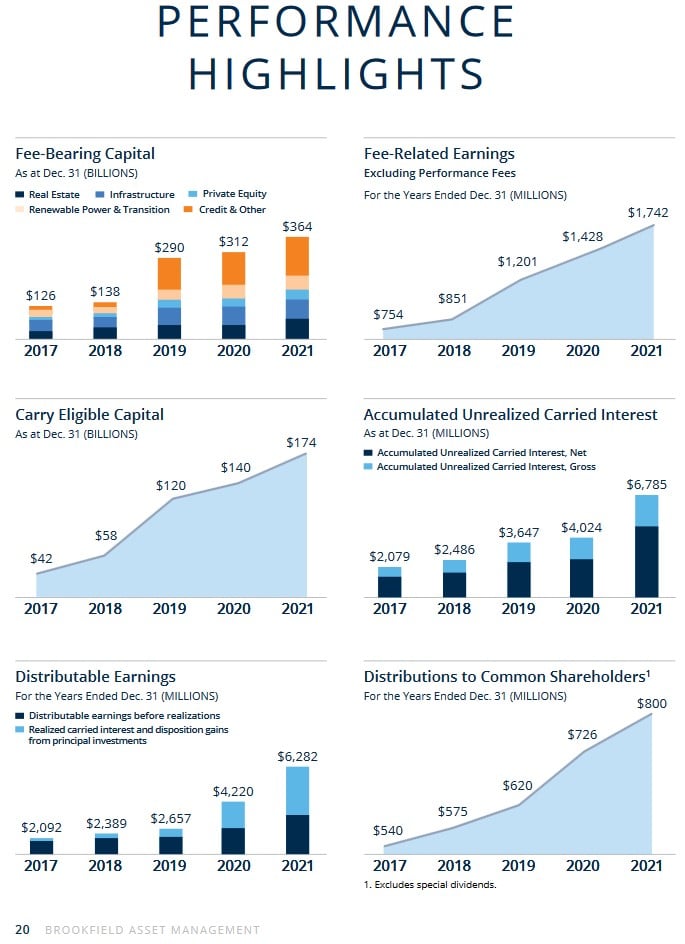

Part 1 Our Business and Strategy in the 2021 Annual Report presents a comprehensive overview of BAM. The following image, however, reflects BAM’s 2017 – 2021 performance highlights. This visual gives a good indication of BAM’s explosive growth and exceptional performance in recent years.

BAM’s September 20, 2021, 2021 Investor Day presentation provides investors with a great overview including how management plans to achieve more than double fee-related earnings by the end of 2026 (~$1.6B in FY2021 to ~$3.7B in FY2026).

How BAM generates income is much the same as how BX generates income.

- Management Fees

- Incentive Fees

- Performance Allocations

- Advisory and Transaction Fees

As BAM continues to deliver for its clients across more strategies, it deepens the client relationship.

The magnitude of BAM’s global reach also offers significant opportunities when assessing potential acquisitions. One very recent example includes Brookfield Infrastructure’s potential acquisition of HomeServe plc. In late March 2022, it announced that one of its private infrastructure funds was in the early stages of considering a possible offer for HomeServe. This opportunity likely arose because BAM recognizes the potential benefits of owning the company outright given its sizable real estate portfolio which could benefit from HomeServe’s services.

In essence, BAM’s scale is such that the entities in which it has a controlling interest can cross-sell to each other (keep the profits within the ‘family’).

Oaktree Capital Management

In March 2019, BAM announced an agreement whereby it would acquire ~61.2% of Oaktree Capital Group, LLC; the merger was completed on September 30, 2019. This transaction enables BAM to broaden its product offering to include one of the finest credit platforms in the world which has a value-driven, contrarian investment style.

Oaktree Capital Group LLC remains a publicly traded company. On the closing date of the merger, however, its direct and indirect ownership of general partner and limited partner interests in certain Oaktree Operating Group entities were transferred to newly-formed, indirect subsidiaries of BAM as of October 1, 2019. As a result, on October 1, 2019, 4 of 6 Oaktree Operating Group entities were no longer indirect subsidiaries and became part of the BAM family.

Now, Brookfield Oaktree Wealth Solutions offers institutional-calibre alternatives expertise and innovative solutions for the individual investor; details of BAM/Oaktree Wealth Solutions are accessible here.

Many investors may be familiar with Oaktree, Howard Marks (Co-Chairman) or other members of Oaktree’s executive team. Periodic memos from Howard Marks in which he shares his insights are well worth a read or a listen. I can’t stress enough how much we can learn by taking the time to listen to this highly successful investor!

I also recommend the following two books he authored:

- Mastering the Market Cycle – Getting the Odds On Your Side

- The Most Important Thing Illuminated – Uncommon Sense for the Thoughtful Investor

Key Metrics

Many investors rely heavily on Earnings per Share (EPS) when evaluating a company. EPS, however, has many drawbacks and is a metric that does not accurately portray how an asset manager performs.

An asset manager uses several non-IFRS measures that give a much better indication of its results; a comprehensive Glossary of Terms BAM uses to analyze and discuss results commences on page 138 of 244 in the 2021 Annual Report.

Funds from Operations (FFO), Fee-Related Earnings (FRE), and Distributable Earnings (DE) are key non-IFRS metrics investors should look at.

BAM’s definition of FFO includes:

We use realized disposition gains and losses within FFO to provide additional insight regarding the performance of investments on a cumulative realized basis, including any unrealized fair value adjustments that were recorded in equity and not otherwise reflected in current period FFO, and believe it is useful to investors to better understand variances between reporting periods. We exclude depreciation and amortization from FFO as we believe that the value of most of our assets typically increases over time, provided we make the necessary maintenance expenditures, the timing and magnitude of which may differ from the amount of depreciation recorded in any given period.

In addition, the depreciated cost base of our assets is reflected in the ultimate realized disposition gain or loss on disposal. As noted above, unrealized fair value changes are excluded from FFO until the period in which the asset is sold. We also exclude deferred income taxes from FFO because the vast majority of the company’s deferred income tax assets and liabilities are a result of the revaluation of our assets under IFRS.

The definition of FRE includes:

FRE is comprised of fee revenues less direct costs associated with earning those fees, which include employee expenses and professional fees as well as business related technology costs, other shared services and taxes.

Fee revenue includes base management fees, incentive distributions, performance fees and transaction fees presented within our Asset Management segment. Many of these items do not appear in consolidated revenues because they are earned from consolidated entities and are eliminated on consolidation.

Its definition of DE includes:

As of January 1, 2021, we now include realizations from our principal investments as these are earnings that are directly received by the Corporation and are available for distribution to common shareholders or to be reinvested into the business.

This table discloses the FY2020 and FY2021 results for these 3 metrics.

Furthermore, management reviewed a couple of these metrics at BAM’s 2021 Investor Day when discussing historical performance and outlook.

Bruce Flatt (CEO) states in his Q1 2022 Letter to Shareholders, that:

Since asset managers don’t need much in the way of facilities, equipment or working capital to do business, we plan for the Manager to pay out approximately 90% of its annual earnings in dividends.

While he does not specifically use the DE term, I fully expect the distributions will be based on DE to be consistent with distributions made by other alternative asset managers.

BX’s Dividend Policy, for example, clearly states:

The intention is to pay to holders of common stock a quarterly dividend representing ~85% of BX’s share of Distributable Earnings, subject to adjustment by amounts determined by Blackstone’s board of directors to be necessary or appropriate to provide for the conduct of its business.

Financials

Q1 2022 Results

I include links to BAM’s Q1 2022 Earnings Release, Form 6-K, and Supplemental Information for ease of reference.

An investment decision based on changes in quarterly results is ludicrous when assessing any entity. This is even more so when assessing an asset manager!

I do not deny that asset managers and their investors look at short-term and medium-term performance. However, the very nature of how asset managers operate is such that investors need to pay less attention to fluctuations in quarterly results.

Taking into consideration BAM’s AUM and transaction sizes, it is very easy to see how quarterly results can exhibit wild swings.

BAM, for example, raises billions of dollars for flagship funds from highly sophisticated investors who commit to investing for several years. The goal is to identify assets where BAM can use its expertise to enhance the returns to meet or exceed target returns. This can result in several years elapsing before BAM disposes of an asset.

Furthermore, market conditions are an important factor in the timing of asset purchases and sales. If market conditions are depressed, BAM may delay the sale of assets until conditions are more favourable. On the other hand, if market conditions are extremely conducive to asset sales, BAM may sell several assets thus generating billions of dollars that flow into DE. Market conditions also come into play when it comes to acquisitions.

Credit Ratings

BAM’s domestic unsecured long-term debt ratings and outlook are:

- Moody’s: Baa1 (stable)

- S&P Global: A- (stable)

- Fitch: A- (stable)

The rating assigned by Moody’s is the top tier of the lower medium grade category. It is one tier lower than the ratings assigned by S&P Global and Fitch which are the lowest tier in the upper medium grade category.

Moody’s rating defines BAM as having an adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity to meet its financial commitments.

The other two ratings define BAM as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Whether the rating agencies amend the ratings once BAM becomes ‘asset light’ remains to be seen. Regardless, BAM’s current ratings are satisfactory for my conservative investor profile.

Dividends and Share Repurchases

Dividend and Dividend Yield

Investors who hold the TSX listed shares should be accustomed to a fluctuation in the quarterly dividend. This is because BAM declares its quarterly dividend in USD. Naturally, foreign currency fluctuations impact any conversion to CDN.

On May 12, 2022, BAM announced that its Board had declared a US$0.14/share quarterly dividend payable on June 30, 2022 to shareholders of record as at the close of business on May 31, 2022. The US shares currently trade at ~$47.60 thus resulting in a ~1.2% dividend yield. Furthermore, BAM has raised the dividend 11 consecutive years making the stock a Dividend Contender.

Investors whose investment decisions are heavily swayed by dividend yield have likely found BAM to be an unappealing investment; BAM’s dividend yield is typically in a tight range of around 1%. However, once BAM completes the proposed spin-off of its asset management business in late 2022, the quarterly payout will change and the dividend yield will most likely rise above historical levels. Although BAM’s quarterly dividend distribution will likely be unpredictable, the dividend distribution should grow over the very long term.

Given the proposed spin-off which is expected to be completed in late 2022, I suggest investors pay little attention to BAM’s historical dividend track record.

Stock Splits and Spin-Offs

Determining the historical return on my BAM investment is beyond my capabilities. While BAM provides an Investment Calculator on its website, it is somewhat simplistic because it merely asks for a specific timeframe and an amount invested OR the number of shares bought.

I have made multiple purchases over the years and these purchases have been spread across several investment accounts. In addition, in some accounts, I hold sufficient shares to acquire additional shares through the automatic reinvestment of quarterly dividends. Furthermore, my monthly FFJ Portfolio reports reflect holdings in several different entities within the BAM group of companies; this report does not reflect BAM holdings in tax advantaged accounts for which I do not disclose details.

I, quite honestly, have no idea of my BAM return on investment. I do know, however, that I am the beneficiary of four 3 for 2 stock splits and I have received shares from several spin-offs.

Share Repurchases

Shares and share equivalents (millions of shares) for the 3 months ended March 31 2021 and 2022 amounted to 1545.4 and 1626.8. These figures include the dilutive effect of the conversion of 34.9 million and 59 million options and escrowed shares.

Looking at the Consolidated Statements of Cash Flows in several BAM Annual Reports, I see the weighted average number of issued and outstanding shares has grown over time.

Comprehensive details regarding BAM’s Common Equity are found commencing on page 225 of 244 in the 2021 Annual Report.

Valuation

I typically include diluted EPS, adjusted diluted EPS, and free cash flow metrics in my assessment of a company. These metrics, however, are not pertinent when analyzing an asset manager.

BAM has historically compared FFO to Net Income; the variance between both metrics can be significant. The sources from which the FY2020 and FY2021 results are obtained are provided so you can see a breakdown of the calculation of both metrics for FY2019 – FY2021. In FY2020, for example, BAM reported sizable fair value changes and depreciation and amortization. Neither of these affected FFO nor DE.

- FY2021 FFO: $4.67/share and Net Income: $2.39/share

- FY2020 FFO: $3.27/share and Net Loss: ($0.12)/share

- FY2019 FFO: $2.71/share and Net Income: $1.73/share

- FY2018 FFO: $4.35/share and Net Income: $3.40/share

- FY2017 FFO: $3.74/share and Net Income: $1.34/share

As mentioned in my BX post, for which a link is provided at the beginning of this post, it is virtually impossible to estimate future FFO, FRE, and DE. Furthermore, BAM does not provide guidance.

The reason BAM is not easy to value is that it raises large pools of capital from clients for deployment thus resulting in multiple multi-billion-dollar acquisitions annually. Because it continually makes sizable investment transactions (acquisitions and divestitures), earnings estimates can quickly become outdated.

As with BX, BAM acquires some assets meant to be perpetual holdings. In other cases, BAM uses its expertise to improve the performance of the companies in which it invests with the intent of monetizing these assets as part of its capital recycling programs.

We also have to consider that market conditions can lead to very wide swings in GAAP earnings.

It is not, therefore, unusual to see wide fair value changes in amounts attributable to consolidated entities and equity accounted investments; an accounting rule requires BAM and BX to report unrealized gains and losses.

Both BAM and BX are not alone in having to report fair value changes. In my Berkshire Hathaway Is Better Than A Broad-Based ETF post, I mention that the reason unrealized gains and losses must be reported is that a GAAP rule imposed in 2018 requires a company to include in earnings the net change in the unrealized gains and losses of its investments. These unrealized gains and losses are paper losses and not actual realized gains and losses that come from any sale.

Warren Buffett often urges investors to ignore such gains and losses.

Brookfield (BAM) Plans To Become Asset Light – Final Thoughts

Some individual investors might want to invest directly in Wealth Solutions offered by BAM/Oaktree and BX. However, I prefer to limit my investment in alternative assets to direct investments in BAM and BX. Ultimately, these two publicly traded companies benefit from their underlying alternative asset offerings.

Undoubtedly, some alternative asset offerings will perform exceptionally well while others may not fare as well. By investing directly in these two publicly listed companies, I stand to benefit from their respective global operations. If some areas of their business experience challenges then the performance of other areas should, in theory, counteract the weaker performers.

Case in point…Brookfield Property Partners was adversely affected by the COVID-19 pandemic and the preventive measures taken to curb the spread of the virus, as well as the potential for future outbreaks of other highly infectious or contagious diseases. Its performance suffered thus negatively impacting investors who invested directly in Brookfield Property Partners.

Post FYE2020, BAM launched a tender offer to take the property company private. This was done because most property securities traded poorly in the market, despite the underlying real estate being valuable. The decision to take it private offered BAM greater flexibility in managing assets.

I envision BAM will take its real estate arm public again in the future. Undoubtedly, the value of the public offering will be higher than that at which it was taken private.

What I see from this example, is that investing at the top of the house (BAM and BX) is a situation in which ‘heads I win, tails I win’.

In previous posts, I mention that I like to ‘follow the money’. Although I have no way of verifying my suspicions, I am almost certain that BAM’s and BX’s senior executives have much larger positions in the parent companies than in the underlying alternative asset ‘flagship funds’. By having direct exposure to BAM and BX, senior executives ultimately participate in the underlying performance of the multiple alternative assets.

When I completed a January 2022 Investment Holdings Review, The Brookfield Group of companies was my 10th largest holding. The ranking may have changed since then but unless I conduct another review I can not confirm its ranking. It is time-consuming to complete such a review because I have holdings spread over 19 investment accounts at two financial institutions; I hold shares in “Core’ and ‘Side’ accounts within the FFJ Portfolio and retirement accounts for which I do not disclose details.

Regardless of whether BAM is still a Top 10 holding or not, I think it will be far more valuable in the future. I, therefore, view the recent weakness in its share price as an opportunity to increase my exposure. On May 11, 2022, I acquired 200 additional shares @ $60.96 in one of the ‘Core’ accounts.

Although it may seem counterintuitive to want BAM’s share price to remain weak, I truly hope the broad market weakness will persist. This will give investors more opportunity to acquire reasonably valued BAM shares to generate attractive total returns over the long term.

I wish you much success on your journey to financial freedom.

Another article by Charles Fournier is Why I Exited My Colgate Position.

Related Articles on Dividend Power

Author Disclosure: I disclose holdings held in the FFJ Portfolio and the dividend income generated from these holdings. I do not disclose details of holdings held in various tax-advantaged accounts for confidentiality reasons.

Author Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, "Become a Better Investor: 5 Fundamental Metrics to Know!" Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

I envision BAM’s FFO, FRE, and DE will fluctuate but will rise over the long term. This is because BAM:

- continually raises new pools of capital;

- the extent to which it acquires or disposes of assets should increase as the level of AUM grows; and

- the timing of asset sales and dispositions is highly unpredictable.

Much like BX, BAM does not operate in a vacuum. Were we to encounter another ‘Financial Crisis’, BAM’s short-term results would likely experience weakness. BAM, however, raises large pools of capital from highly sophisticated investors who have a long-term investment time horizon and who commit to investing for several years. Therefore, BAM should not need to urgently liquidate assets to raise funds to return to its investors. On the contrary, BAM’s access to sophisticated investors with ‘deep pockets’ makes it likely that it would be in a position to acquire assets at favourable valuations.

Brookfield (BAM) Plans To Become Asset Light – Final Thoughts

Some individual investors might want to invest directly in Wealth Solutions offered by BAM/Oaktree and BX. However, I prefer to limit my investment in alternative assets to direct investments in BAM and BX. Ultimately, these two publicly traded companies benefit from their underlying alternative asset offerings.

Undoubtedly, some alternative asset offerings will perform exceptionally well while others may not fare as well. By investing directly in these two publicly listed companies, I stand to benefit from their respective global operations. If some areas of their business experience challenges then the performance of other areas should, in theory, counteract the weaker performers.

Case in point…Brookfield Property Partners was adversely affected by the COVID-19 pandemic and the preventive measures taken to curb the spread of the virus, as well as the potential for future outbreaks of other highly infectious or contagious diseases. Its performance suffered thus negatively impacting investors who invested directly in Brookfield Property Partners.

Post FYE2020, BAM launched a tender offer to take the property company private. This was done because most property securities traded poorly in the market, despite the underlying real estate being valuable. The decision to take it private offered BAM greater flexibility in managing assets.

I envision BAM will take its real estate arm public again in the future. Undoubtedly, the value of the public offering will be higher than that at which it was taken private.

What I see from this example, is that investing at the top of the house (BAM and BX) is a situation in which ‘heads I win, tails I win’.

In previous posts, I mention that I like to ‘follow the money’. Although I have no way of verifying my suspicions, I am almost certain that BAM’s and BX’s senior executives have much larger positions in the parent companies than in the underlying alternative asset ‘flagship funds’. By having direct exposure to BAM and BX, senior executives ultimately participate in the underlying performance of the multiple alternative assets.

When I completed a January 2022 Investment Holdings Review, The Brookfield Group of companies was my 10th largest holding. The ranking may have changed since then but unless I conduct another review I can not confirm its ranking. It is time-consuming to complete such a review because I have holdings spread over 19 investment accounts at two financial institutions; I hold shares in “Core’ and ‘Side’ accounts within the FFJ Portfolio and retirement accounts for which I do not disclose details.

Regardless of whether BAM is still a Top 10 holding or not, I think it will be far more valuable in the future. I, therefore, view the recent weakness in its share price as an opportunity to increase my exposure. On May 11, 2022, I acquired 200 additional shares @ $60.96 in one of the ‘Core’ accounts.

Although it may seem counterintuitive to want BAM’s share price to remain weak, I truly hope the broad market weakness will persist. This will give investors more opportunity to acquire reasonably valued BAM shares to generate attractive total returns over the long term.

I wish you much success on your journey to financial freedom.

Another article by Charles Fournier is Why I Exited My Colgate Position.

Related Articles on Dividend Power

Author Disclosure: I disclose holdings held in the FFJ Portfolio and the dividend income generated from these holdings. I do not disclose details of holdings held in various tax-advantaged accounts for confidentiality reasons.

Author Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, "Become a Better Investor: 5 Fundamental Metrics to Know!" Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

I am a self-taught investor and run the Financial Freedom is a Journey blog. I have invested in the North American equities markets for over 34 years. I retired from a career in banking and continue to invest as this is something about which I am passionate.

I don’t own BAM but its renewable energy subsidiary, BEPC. With everything that is going on with ESG and a looming energy crisis, it’s beyond me why BEPC is not way more up. It’s 40% off its ATH about a year ago. Anyways, I see prices sub 40 USD as buying opportunities. Would you say BAM is one of the best asset managing companies out there?

The Asset Manager (AM) space is highly fragmented. Just access a stock filter and search for companies in the Asset Management industry. You will get a laundry list of industry participants. Rank them in order of market cap and you will see a huge gap in market cap after you get past the top 3 (BLK, BX, and BAM).

I have chosen to invest in BAM and BX because they have a proven track record of success and because they are so large they can do transactions many other AMs can only dream of doing.

Another consideration is that BAM and BX can make strategic acquisitions where they know there will be synergies with the companies they already own; smaller AMs might not have this advantage. In my post, I provide the example of BAM’s acquisition of HomeServe.

The nature of this business is that billions of $ are raised which are then deployed. Raising this kind of money means going after ‘deep pockets’. BAM and BX need no introduction when calling on potential investors. Smaller AMs, on the hand, probably have to spend time explaining who they are and why these sophisticated investors should consider adding them to the list of AMs with whom they have already forged a successful relationship. Once an AM proves itself, the ‘wallets’ open more easily. Both BAM and BX deal with thousands of ‘wallets’.

Brain power is also a key element in this space. You want the brightest of the bright on your team. Both firms get inundated with applicants from which they select what they consider to be those with the most potential. Those who are not hired by BAM and BX then seek out other AMs. I am not implying those who end up with other AMs will not ultimately be great investors but these job applicants are much like athletes wanting to make it to the professional leagues.

As far as BEPC goes, stock prices do not necessarily always represent the true value of a company. Stop being surprised why the share price is off 40% from the ATH. Crazier stuff has happened. Worthless companies were once trading at stratospheric levels. The old adage ‘you can’t fix stupid’ applies in the world of investments.

I presume you are referencing the US listed shares and not those on the TSX. If this is correct then you now have a buying opportunity.