I would avoid PPG Industries, Inc. (PPG)! Investors relying on a steady stream of dividend income and who focus heavily on various dividend metrics will undoubtedly have a different opinion. Based on my goals, objectives, risk tolerance, and universe of potential investment opportunities, however, I can’t see what would remotely prompt me to invest in this company.

Perhaps I have been asked to analyze it because it is a Dividend King having increased its dividend for 53 consecutive years. Maybe it is because the dividend declared on July 18 marks the company’s 504th consecutive dividend payment.

Whatever the reason, my outlook is no different from the time I last analyzed the company in this October 14, 2018 post. The focus should be on an investment’s future TOTAL potential return and accompanying risk. Based on my analysis, I would continue to avoid PPG.

Affiliate

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more.

Business Overview

PPG was incorporated in Pennsylvania in 1883 and is in the business of manufacturing and distributing a broad range of paints, coatings and specialty materials.

You may be familiar with the company to some degree but the best way to learn about the business and risks is to review the company’s website and Part 1 in the most recent Form 10-K.

Historical Investor Returns

Past performance is not necessarily indicative of future returns. Having said this, if a company’s total investment return over several years is less than stellar, what are the odds it is going to pull a rabbit out of its hat and generate better returns over the next decade or longer?

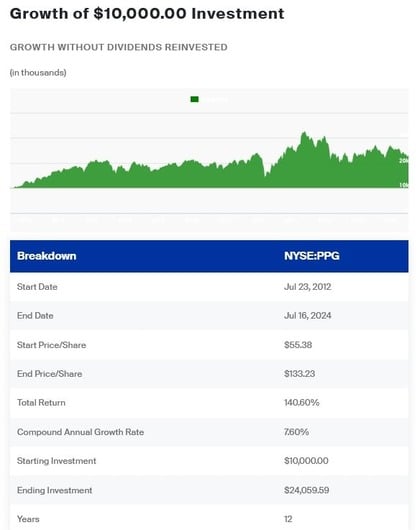

I am a long-term investor so how a company performs over a few years is of little relevance to me. My interest lies in an investment TOTAL investment return over a very long time frame. Since PPG has been kind enough to include an Investment Calculator on its website, let’s see how an investment in this company would have fared over time.

As I compose this post, PPG’s Investment Calculator only goes back to July 23, 2012; this could change by the time you look at this Investment Calculator.

Currently, this is what PPG’s website generated.

Applying the Rule of 72 and PPG’s 7.60% compound annual growth rate means it took almost 9.50 years to double an investment in the company.

Naturally, the rate of return is heavily dependent on the entry point, the duration in which an investment is held, and whether the dividends have been reinvested or not.

For interest sake, I decided to see how a PPG investment has fared using the earliest start date I could obtain on the Tickertech website.

There you have it. Over a span of ~29 years, the average annual total return was 8.8% when dividends were reinvested and 7.11% if not.

You decide if these rates of return are acceptable. Before you make your decision, however, consider using a US inflation calculator to gauge the impact of inflation on your investment.

I chose August 1995 to coincide with the start date I selected in Tickertech. If you do not like the time frame I selected, use this Inflation Calculator to change the start date.

Those 8.8% and 7.11% average annual total returns start to look less attractive when we account for a 2.53% annual inflation rate.

Financial Review

Q2 and YTD2024 Results

Currently available material related to this earnings release is accessible here and the Q2 Form 10-Q is accessible here.

Despite reporting record reported EPS and adjusted EPS and YoY adjusted EPS growth of 11% ($2.50 versus $2.25 in Q2 2023), marking the sixth consecutive quarter of growth, PPG continues to face an increasing challenging macro-environment.

While the company has reduced its inventory by $0.21B from Q2 2023 (85 days of inventory in Q2 2024 versus 88 days in Q2 2023), it is still above the 83 days level in Q2 2019 (pre-COVID).

For comparison purposes, PPG’s days of inventory in Q1 2023 and Q1 2024 was 98 and 94, respectively. In Q1 2029, it was 91 days.

PPG’s net debt has also increased to $5.2B at the end of Q2 2024 versus $5.0B at the end of Q1 2024 and $4.5B at FYE2023 (December 31).

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

In the FY2014 – FY2023 time frame, PPG’s:

- OCF was (in B$) 1.528, 1.895, 1.351, 1.568, 1.467, 2.080, 2.130, 1.562, 0.963, and 2.411.

- CAPEX was (in B$) 0.564, 0.430, 0.380, 0.360, 0.411, 0.413, 0.304, 0.371, 0.518, and 0.549.

- FCF was (in B$) 0.964, 1.465, 0.971, 1.208, 1.056, 1.667, 1.826, 1.191, 0.445, and 1.862.

To put these numbers in perspective, PPG’s annual revenue during the same period was (in B$) 14.79 ,14.24, 14.27, 14.75, 15.37, 15.15, 13.83, 16.80, 17.65, and 18.25. Revenue in the first half of FY2024 is ~$9.1B.

The most current Consolidated Statement of Cash Flows is reflected in the Q2 Form 10-Q (refer to the SEC Filings section of PPG’s website). In the first half of FY2024, PPG generated $0.305B of OCF, and its CAPEX was ~$0.374B thus resulting in (~$0.069B) in FCF.

I have exposure to several companies that generate comparable or less revenue than PPG that consistently generate more OCF and FCF. This is just one of several reasons why I would avoid PPG.

Return On Invested Capital (ROIC)

PPG’s ROIC (%) in FY2014 – FY2023 is 25.24, 15.89, 10.21, 17.42, 14.64, 12.7, 9.81, 11.63, 7.95, and 9.33.

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level. We see that PPG’s ROIC track record is less than stellar.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

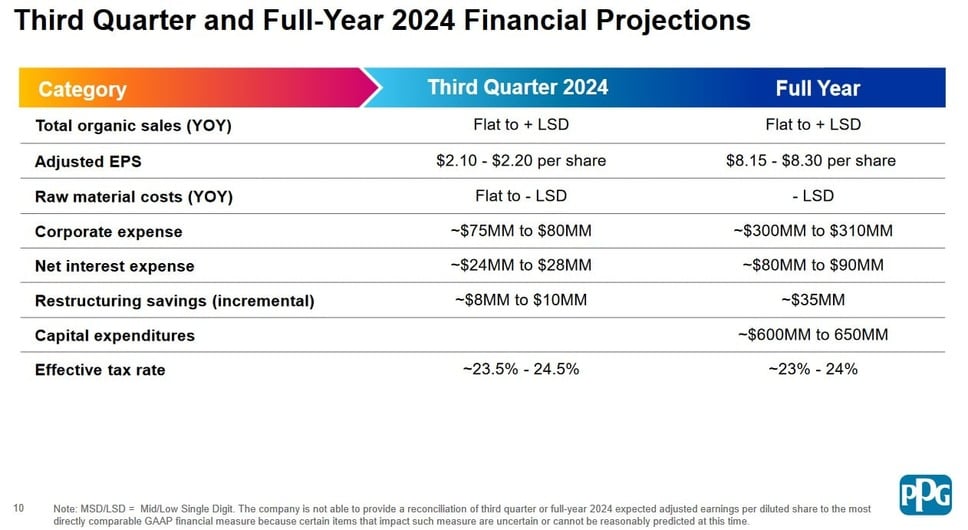

FY2024 Outlook

The following reflects PPG’s Q3 and FY2024 financial projections.

For comparison, I include PPG’s projections provided when it released its FY2023 and Q1 2024 results.

We see from these projections that PPG has lowered its total organic sales outlook for the year from a low single digit to flat/low single digit. The adjusted diluted EPS outlook has also been lowered.

Needless to say, PPG expects continued headwinds that will contribute to less than stellar results.

Risk Assessment

Every investment should be viewed from a risk/reward aspect. Far too often, however, investors neglect the risk aspect of an investment. This can often lead to heartbreak.

I fully appreciate that credit rating companies don’t always ‘get it right’. Nevertheless, I still look at how they rate a company’s domestic senior unsecured debt to determine if my risk assessment is in sync with their assessment.

Prior to October 1985, Moody’s assigned an Aa3 rating to PPG’s domestic senior unsecured debt. This was the lowest tier of the High Grade investment grade category and was just 3 tiers below the coveted AAA rating.

How did PPG do over the years?

By August 2009, PPG’s management had done what was necessary for Moody’s to assign a Baa1 rating (the top tier of the lower medium grade investment grade tier. That is 4 tiers below the Aa3 rating. Fantastic!

This rating was subsequently upgrade to A3 in March 2016 and is unchanged since that upgrade. This rating, the lowest tier of the upper medium grade investment grade category and is just 1 tier higher than the prior Baa1 rating.

S&P Global downgraded PPG’s issuer rating to BBB+ from A- in March 2020 and there has been no change since then. This rating is comparable to Moody’s Baa1 rating.

Fitch downgraded PPG’s domestic senior unsecured debt from A to A- in July 2007 and downgraded it further in December 2021 from A- to BBB+.

Although these ratings are acceptable from my risk tolerance perspective, the downgrades together with several other factors lead me to conclude that there are far better companies in which I should invest.

Details about PPG’s Leases and Long-Term Debt are found in Notes 9 and 10 in the FY2023 Form 10-K commencing on page 46 of 241.

Dividends and Share Repurchases

Dividends and Dividend Yield

Dividend metrics (ie. dividend yield, consecutive number of years of dividend increases) should have very little influence in an investor’s decision making process.

I promised myself that I would not go on a rant about investment decisions that are heavily dependent on dividend metrics and will merely suggest reading my Focus On Total Shareholder Return post.

Once a company prioritizes the distribution of dividends in its capital allocation policy, it becomes very difficult to change this path. Were PPG to decide to make changes in the allocation of capital (eg. increase debt repayment and/or share repurchases), its investor base would likely receive a shock. Many PPG investors have come to rely on the dividend distributions and would likely ‘jump ship’ if PPG were to make changes.

If dividend metrics are still important to you, here is PPG’s dividend history. You will see that it just declared

Share Repurchases

PPG’s weighted average diluted shares outstanding in FY2014 – FY2023 (millions of shares) is 280, 274, 267, 258, 245, 238, 238, 239, 237, and 237. In the 3 months ending June 30, 2024, this had been reduced to 235.7.

The following details of PPG’s repurchase activity for the three months ended June 30, 2024 has been extracted from page 36 of 43 in the Q2 Form 10-Q.

Looking at PPG’s historical Consolidated Statement of Cash Flows, it is readily apparent that dividend distributions have been a much higher priority than share repurchases. In FY2021 – 2023, PPG repurchased (in millions of $) 210, 190, and 86. In contrast, it distributed dividends amounting to (in millions of $) 536, 570, 598.

So far in FY2024, PPG has ramped up its share repurchases to ~$0.312B while its dividend distributions amount to $0.305B. Whether PPG continues to repurchase shares to the same degree as in Q1 and Q2 2024 is subject to debate. Unless the FCF results improve, I suspect PPG’s share repurchases might be scaled back.

Valuation

PPG’s PE levels in FY2014 – FY2023 are 23.78, 23.09, 30.08, 22.68, 20.78, 26.38, 31.77, 28.98, 28.26, and 25.05.

Its P/FCF levels during the same period are 21.03, 18.42, 15.94, 19.20, 21.17, 15.38, 17.38, 19.91, 35.95, and 16.88.

In the first half of FY2024, PPG generated $3.93 ($1.69 in Q1 and $2.24 in Q2) of diluted EPS. With shares trading at ~$127.50 on July 22 and assuming PPG’s diluted EPS results in the second half of FY2024 are somewhat comparable to the first half, the forward PE is ~16.2.

YTD adjusted diluted EPS is $4.36 ($1.86 in Q1 and $2.50 in Q2) and management’s FY2024 adjusted diluted EPS outlook is $8.15 – $8.30. Using the ~$127.50 share price, the forward adjusted diluted PE range is ~15.4 – ~15.6.

PPG forward adjusted diluted PE levels using the current brokers’ outlook is:

- FY2024 – 24 brokers – mean of $8.28 and low/high of $8.14 – $8.47. Using the mean estimate: ~15.4.

- FY2025 – 25 brokers – mean of $9.12 and low/high of $8.58 – $9.95. Using the mean estimate: ~14.

- FY2026 – 13 brokers – mean of $9.96 and low/high of $9.10 – $11.15. Using the mean estimate: ~12.8.

There is a wide range in earnings estimates and with management’s recent adjusted diluted EPS outlook, I expect analysts with estimates at the top end of the ranges might be revisiting their numbers.

Looking at PPG from a P/FCF perspective, we see that PPG has generated negative FCF in the first half of FY2024. I do not expect PPG to have negative FCF for the entire fiscal year but by mid-2023, PPG had generated ~$0.379B in FCF. PPG’s YTD2024 FCF is ~$0.448B less than the same time in the prior fiscal year. I am not, therefore, optimistic that it will generate ~$1.862B of FCF as it did in FY2023.

As noted earlier, the adjusted weighted average common shares outstanding in Q2 is 235.7 million; I expect the average for the year to be ~235 million.

If I give PPG the benefit of the doubt that it will generate ~$1.45B of FCF in FY2024, PPG would generate ~$6.17 of FCF/share. With shares trading at ~$127.50, I estimated the forward P/FCF is ~20.7.

PPG’s valuation may appeal to some investors but I consider PPG to be a value trap. Quite often, a company’s valuation is appealing because investors’ expectations for the company are low.

Final Thoughts

At the outset of this post, I state that I would not remotely invest in this company given my goals, objectives, risk tolerance, and the universe of potential investment opportunities.

Although the company’s Dividend King status may appeal to some investors, my preference is to invest in a company with far superior long-term total investment potential and superior capital allocation. I would much rather that a company retain funds for growth, share repurchases, and/or debt reduction.

Another consideration investors should make lies in the tax implications associated with dividend payments. Depending on your circumstances, you may incur a tax liability on dividends received from PPG. I pay enough taxes as it is so I am endeavoring to delay tax liabilities for as long as possible.

Furthermore, I am a Canadian. If I were to hold PPG shares in a taxable account, I would incur a 15% dividend withholding tax ‘haircut’ BEFORE the dividend hits my investment account. That $0.68/share quarterly dividend becomes $0.578/share making a PPG investment even less appealing.

I wish you much success on your journey to financial freedom!

Disclosure: I do not have PPG exposure and have no intention of initiating a position. I disclose holdings held in the FFJ Portfolio and the dividend income generated from the holdings within this portfolio. I do not disclose details of holdings held in various tax-advantaged accounts for confidentiality reasons.

Author Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

Related articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

I am a self-taught investor and run the Financial Freedom is a Journey blog. I have invested in the North American equities markets for over 34 years. I retired from a career in banking and continue to invest as this is something about which I am passionate.