Attractively valued Imperial Oil (IMO) is gushing free cash flow and is likely to continue to do so over the foreseeable future. Investors, therefore, might be interested in looking at this Calgary, Alberta headquartered company which is 69.6% owned by Exxon Mobil Corporation (XOM).

IMO is listed on the TSX in Canada and the NYSE in the US. All financial results are reported in Canadian dollars, and therefore, all financial figures herein are expressed in Canadian dollars.

Imperial Oil was incorporated under the laws of Canada in 1880. It is one of Canada’s largest integrated oil companies with activities in all phases of the petroleum industry in Canada. This includes the exploration for, and production and sale of, crude oil and natural gas.

While it is a major producer of crude oil, the largest petroleum refiner, a leading marketer of petroleum products, and a major producer of petrochemicals in Canada, it also pursues lower-emission business opportunities including carbon capture and storage and biofuels.

Affiliate

Take the Simply Investing Course to learn more about investing and dividends.

- Lifetime access with 27 self-paced lessons.

- Covers placing stock orders, building and tracking portfolios, when to sell, reducing fees and risk, etc.

- Learn the 12 Rule of Simply Investing

- Simply Investing Coupon Code – DIVPOWER15.

Imperial Oil Company Overview

IMO’s operations are conducted in three main segments:

- Upstream – these operations include the exploration for, and production of, crude oil, natural gas, synthetic oil and bitumen;

- Downstream – this segment consists of the transportation and refining of crude oil, blending of refined products and the distribution and marketing of those products; and

- Chemical – this consists of the manufacturing and marketing of various petrochemicals.

As noted earlier, XOM is a controlling shareholder. Looking through IMO’s FY2021 Form 10-K, we see just how closely these companies are intertwined.

Imperial Oil, for example, relies upon its research and development organizations and those of XOM, with whom IMO conducts shared research.

Several of IMO’s incumbent Directors and Executive Officers also own common shares or restricted stock units in IMO and XOM.

IMO’s ‘Long-term business outlook’ is also based on XOM’s Outlook for Energy. This outlook is used to help inform IMO’s long-term business strategies and investment plans.

IMO further benefits from its relationship with XOM’s North American chemical businesses. This enables it to maintain a leadership position in its key market segments.

At FYE2021, IMO had also borrowed $4.5B under an existing agreement with an affiliated company of XOM. This long-term, variable-rate, Canadian dollar loan from XOM permits IMO to borrow up to $7.75B at interest equivalent to Canadian market rates. The loan agreement is effective until June 30, 2025 and is cancelable if XOM provides at least 370 days of advance written notice.

I strongly encourage you to review Part 1 of IMO’s FY2021 Form 10-K if you wish to learn more about the company.

IMO’s March 10, 2022 Investor Day Presentation is also highly informative and we see that the company is committed to returning surplus cash to shareholders in the form of dividends and share repurchases.

Canadian-Based, Canadian Focus

Given how closely these two companies are intertwined, some investors may wonder ‘Why not just invest in XOM to have exposure to IMO?’

This is a fair question and for the sake of full disclosure, I do not own IMO shares. My exposure to IMO is solely through my share ownership in XOM.

Some investors, however, are reluctant to invest in XOM for specific reasons. One such reason is that XOM has operations in regions far less stable than Canada and the United States.

Although XOM has significant experience in operating in challenging regions, no company can be fully prepared when a country unilaterally decides that a company’s assets are to be seized (Russia? Venezuela?).

XOM also has operations in Argentina, for example, whose economy is ranked the 144th globally and 27th among 32 countries in the Americas region as being freest in the 2022 Index of Economic Freedom. This global ranking is even worse than that of Nigeria, Angola, and Cameroon. On the bright side, Argentina’s ranking is slightly better than that of Chad which is ranked 146th.

All of these aforementioned countries have an overall economic freedom score below their regional and world averages.

If XOM’s exposure to these countries is a concern, then knowing that ExxonMobil Iraq Limited (EMIL), an affiliate of XOM, has an agreement with the South Oil Company of the Iraq Ministry of Oil to rehabilitate and redevelop the West Qurna I field in southern Iraq might be even more worrisome.

Oil Industry Overview

Some investors might think the days are numbered for oil and gas companies because of the trend away from fossil fuels. I completely disagree and for the past several years have been increasing my exposure to XOM and Chevron (CVX); I also own shares in TotalEnergies SE (TTE).

The return on both these investments has been lacklustre for the past few years. However, their depressed stock price has provided investors with a ‘buying opportunity’.

Given the long-term outlook for fossil fuels, these integrated major oil and gas companies have significantly scaled back exploration. Historically, the major oil and gas producers would incur billions of dollars in CAPEX over several years before any earnings would be generated from these major projects. Those days are over!

Furthermore, we have a refining issue. As of January 1, 2021, there were 129 operable petroleum refineries in the United States. The newest refinery in the United States is the Targa Resources Corporation’s refinery in Channelview, Texas, which began operating in 2019. However, the newest refinery with significant downstream unit capacity is Marathon’s facility in Garyville, Louisiana which came online in 1977.

While capacity has been added to existing refineries through upgrades or new construction, there are limitations as to how quickly supply can keep up with demand.

This is borne out by US President Joe Biden’s order earlier this year for a major release of oil from America’s reserves to bring down high fuel costs created by a supply crunch sparked by war in Ukraine.

The release of up to 180 million barrels of oil over 6 months is the largest since the reserve was created in 1974. This release of ~1 million barrels a day will not resolve the energy crisis. It merely serves as a stopgap until the end of the year by which time it is anticipated domestic production will ramp up.

In a nutshell, we have been structurally under-supplied and heading into 2022, we were already approaching the exhaustion of OPEC spare capacity. This year is essentially the culmination of all these factors combined with the surge in demand as the world slowly recovers from COVID lockdowns.

Recession – Demand Destruction?

The war in Ukraine, which triggered a wave of sanctions on Russian flows, has resulted in oil being ~40% more expensive than a year ago. These higher prices coupled with concerns of a global slowdown could lead to demand erosion; Vitol Group, the biggest independent oil trader, has recently indicated that surging fuel costs are starting to hurt demand. However, many product prices are still elevated because crude oil supply outages, including in Libya, have offset some of the weaknesses.

It is difficult to predict how oil prices will behave over the very short term. Nevertheless, it is readily apparent global supply challenges are likely to lead to continued elevated product prices even if a global recession leads to demand destruction.

In my opinion, we may witness wild swings in crude prices thus leading to significant variances in the quarterly results of major industry participants. However, I expect oil and gas prices to remain well above breakeven levels for several more quarters thus resulting in continued strong free cash flow generation.

Preparing For The New Climate Reality

The major oil and gas producers will likely be awash in Free Cash Flow over the foreseeable future. Senior management at these companies, however, is well aware they must adapt to a changing world.

I highly encourage you to listen to interviews with XOM’s CEO. The interviews are lengthy but worthy of your time if investing in the Oil and Gas sector piques your interest.

- How ExxonMobil Will Survive In The New Climate Reality

- How ExxonMobil Is Planning For A Future Of EVs

- ExxonMobil At The Crossroads | CNBC Documentary

XOM’s CEO is predicting every new passenger car sold globally by 2040 will be an electric vehicle. This might discourage some investors from investing in the oil and gas sector. However, investors need to look at the big picture.

XOM estimates global oil demand in 2040 may be equivalent to what the world needed in 2013 or 2014 and we know XOM was profitable at that time.

Given management’s outlook regarding global passenger vehicles in 2040, it is evident the company is looking to what the world might look like decades into the future. Management is clearly evaluating how the decline in gasoline sales could impact its business and that chemicals will be key to keeping the company profitable during the clean energy transition.

This is why investors must invest in a company with the long term in mind. Leave the short-term price fluctuations to the gamblers who sometimes have no clue about a company’s business.

Investors are also very highly encouraged to listen to 2 industry experts discuss falling inventories, OPEC spare capacity, $180 oil, and their outlook for energy stocks in this June 27, 2022 Oil and Energy update.

Imperial Oil Financial Review

Q1 2022 Results

On April 29, 2022, IMO reported strong Q1 2022 results across all business lines as pandemic restrictions were lifted and commodity prices further strengthened.

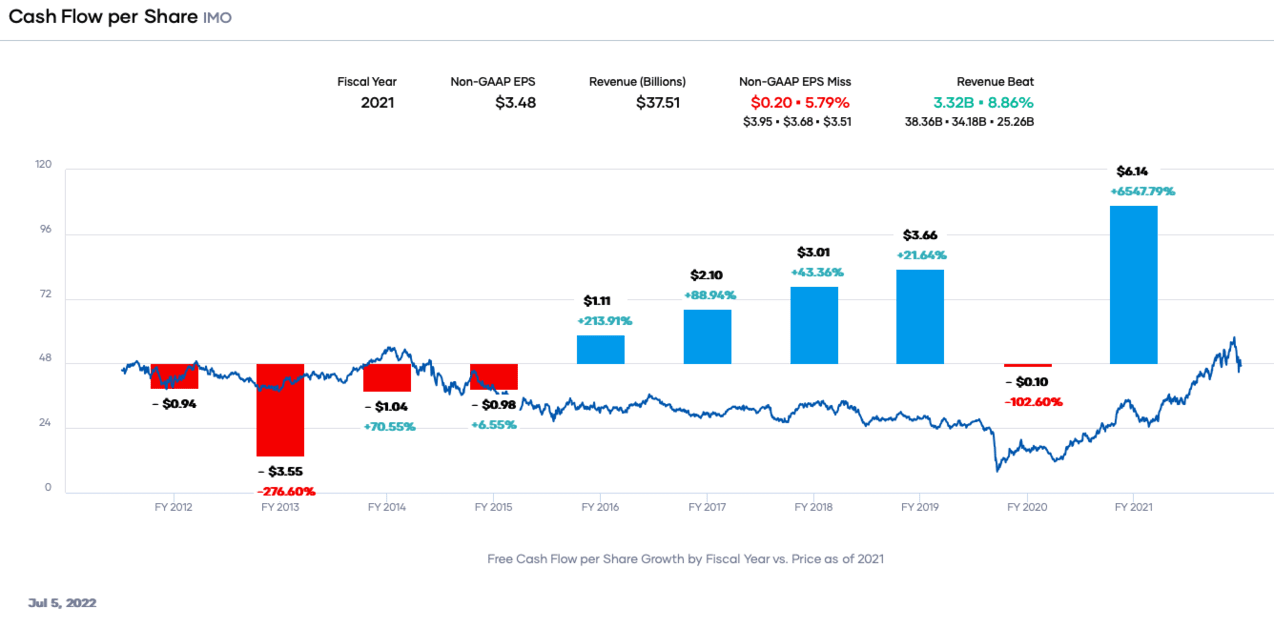

During the quarter, Imperial Oil generated $1.635B of Free Cash Flow (FCF) versus $0.898B in Q1 2021. In comparison, IMO generated $1.233B and $4.464B of FCF in Q4 2021 and FY2021.

FY2023 Guidance

Management does not issue guidance. Expectations, however, are for IMO to continue to generate substantial free cash flow over the remainder of FY2022. It is not unreasonable to expect IMO to generate at least $6B in FCF ($1.635B FCF in Q1 x 4 quarters = $6.54B).

Credit Ratings

Risk assessment is a critical component of any investment analysis, yet it is often overlooked by so many investors. Had investors properly analyzed their potential risk exposure before investing in highly speculative companies or cryptocurrencies, we might not be reading so many stories on social media from people whose ‘investments’ have been decimated.

Where possible I check if the major rating agencies have assigned ratings to a company’s domestic long-term unsecured debt. This form of debt carries more risk than secured debt but is less risky than owning common shares. It is, therefore, important, that equity investors account for this higher risk. If a company’s domestic long-term unsecured debt is rated at the lowest tier of the lower medium grade investment-grade category, for example, then a common shareholder’s risk is a non-investment grade (speculative).

Moody’s withdrew its ratings for Imperial Oil in November 2003. S&P Global, however, still rates IMO.

S&P Global downgraded IMO’s domestic long-term unsecured debt from AA to AA- in February 2021. This is the bottom tier of the high-grade investment grade category. This rating was last reviewed in May 2022 and the outlook is stable.

Since IMO is so heavily dependent on XOM we must look at XOM’s credit ratings. Its current domestic long-term unsecured debt ratings and outlook are:

- Moody’s: Aa2 (stable) last reviewed March 2021 at which time this rating was downgraded from Aa1

- S&P Global: AA- (stable) last reviewed May 2022. This rating was downgraded from AA in February 2021.

The rating assigned by Moody’s is the middle tier of the high-grade investment grade category. It is one tier above the rating assigned by S&P Global.

Both ratings define XOM as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

Dividends and Share Repurchases

Dividends and Dividend Yield

Imperial Oil distributed dividends of $0.407B, $0.441B, $0.449B, $0.492B, $0.524B, $0.572B, $0.631B, $0.649B, and $.706B. In Q1 2022 it distributed $0.185B versus $0.162B in Q1 2021. IMO’s dividend history and market cap allow it to be included in the 2022 Canadian Dividend Aristocrats.

IMO’s website reflects a very limited dividend history so investors may wish to look at the dividend history reflected on the TMX website. However, IMO is one of the longest dividend paying Canadian companies with a streak of more than 100 years.

IMO’s dividend history reflects several instances in which the quarterly dividend was held constant for more than 4 consecutive quarters. When reviewing IMO’s dividend history, we must account for the 3 for 1 stock splits in 1998 and 2006. This explains why IMO’s quarterly dividend dropped from $0.24 to $0.08 in 2006 and $0.55 to $0.185 in 1998.

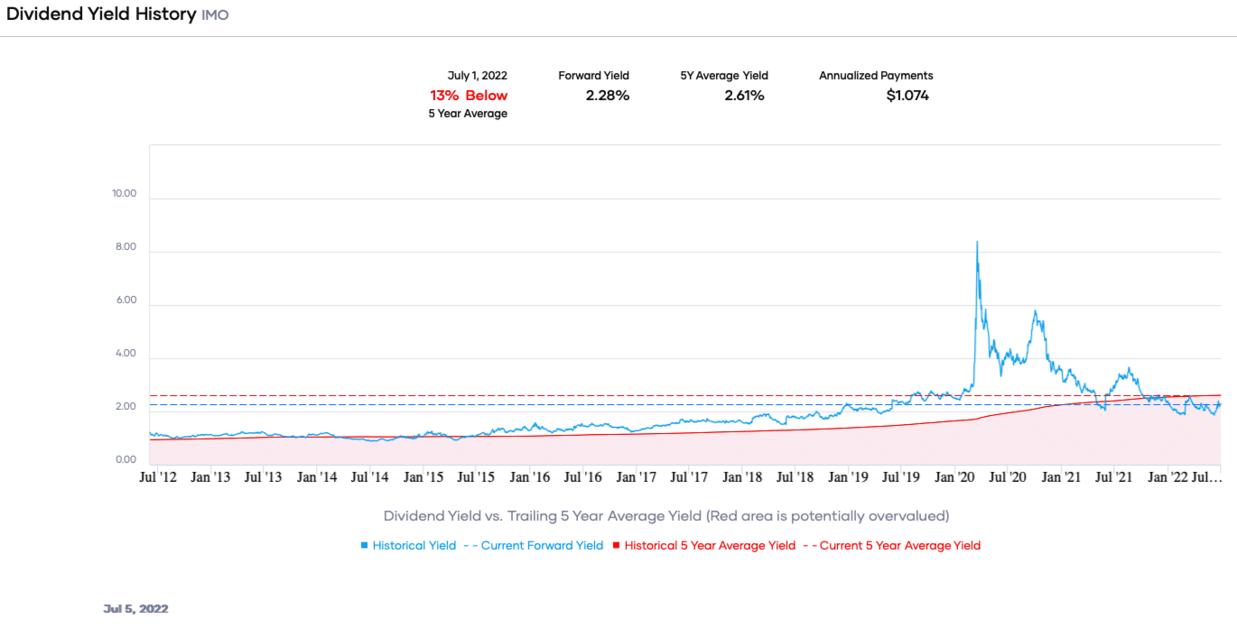

IMO’s most recent quarterly $0.34 dividend was distributed on July 1, 2022, but with the markets being closed on Canada Day, the dividend will be deposited on the next business day.

With shares trading at ~$61 at the market close on June 29, 2022, the dividend yield is ~2.28%, according to Portfolio Insight*. US residents who hold IMO shares in a taxable account will incur a dividend withholding tax so the dividend yield will be lower.

The company generates ample cash flow and is very conservatively capitalized. I envision no issue with IMO’s ability to continue to reward shareholders with dividend increases.

Share Repurchases

IMO repurchased no shares in FY2013 – FY2016. In FY2017 – FY2021 it repurchased $0.627B, $1.971B, $1.373B, $0.274B, and $2.245B. In Q1 2022 it repurchased $0.449B versus $0 in Q1 2021.

On June 15, 2022, IMO announced that it had purchased shares representing an aggregate of $2.5B and 4.9% of the total number of issued and outstanding shares as of the close of business on May 2, 2022. Immediately following the completion of this offer, IMO had 636,676,182 issued and outstanding shares.

Affiliate

Try the Simply Investing Report & Analysis Platform.

- 6,000+ stocks on the NYSE, NASDAQ, and TSX

- 120+ metrics and financial data updated daily

- Portfolios, watch lists, dividend income, e-mail alerts, etc.

- List of top ranked stocks based on the 12 Rules of Simply Investing

- 14-day free trial

Try the Simply Investing Course

- 10 modules and 27 lessons

- Access to 21-years of stock data and portfolio tracker

- 1-month free access the Report & Analysis Platform

- Lifetime access to the course and 30-day money back guarantee

Use the Simply Investing Coupon Code DIVPOWER15 for 15% off.

Valuation

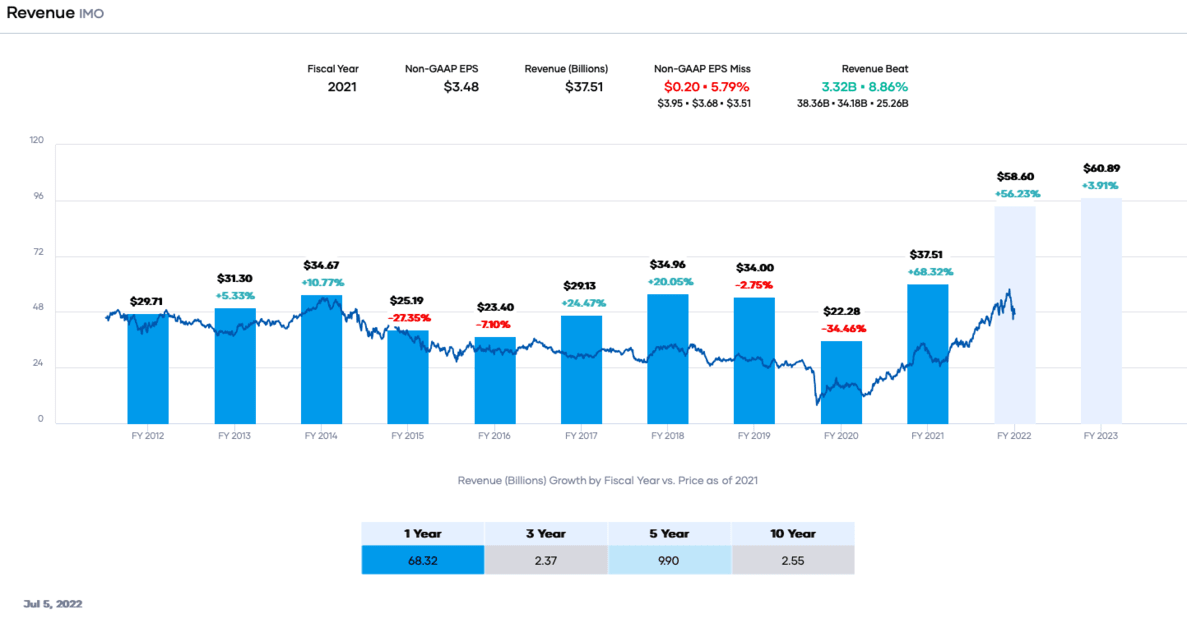

In FY2021, IMO generated $3.48 in diluted EPS. Using the current ~$61 share price IMO’s diluted PE ratio is ~17.5X based on trailing earnings.

Industry conditions in FY2022, however, are VERY different from FY2021. In Q1 2022, IMO generated $1.75 and I anticipate another 3 solid quarters. Taking into consideration the $2.5B share repurchase, I envision FY2022 diluted EPS of ~$8.50. This would give us a forward diluted PE ratio of ~7.2 based on the current share price.

Using the adjusted diluted earnings estimates from the brokers which cover IMO, we get the following forward adjusted diluted PE levels.

- FY2022 – 8 brokers – mean of $8.96 and low/high of $5.38 – $10.92. Using the mean estimate, the forward adjusted diluted PE is ~6.8.

- FY2023 – 9 brokers – mean of $8.55 and low/high of $3.98 – $12.59. Using the mean estimate, the forward adjusted diluted PE is ~7.

- FY2024 – 6 brokers – mean of $8.94 and low/high of $4.75 – $13.93. Using the mean estimate, the forward adjusted diluted PE is ~6.8.

- FY2025 – 3 brokers – mean of $10.31 and low/high of $5.00 – $16.25. Using the mean estimate, the forward adjusted diluted PE is ~6.

Only 3 brokers have provided estimates for FY2025. Furthermore, much can change between now and FY2025, so I am very reluctant to place any reliance on estimates beyond FY2023.

Earlier, I suggested that if the remainder of the current fiscal year is as strong as Q1, it is not unreasonable to expect IMO to generate at least $6B in free cash flow. With ~636.7 million shares outstanding this results in FY2022 FCF/share of ~$9.42. With shares trading at ~$61, we get a forward Price/FCF share valuation of ~6.5.

I consider IMO to be attractively valued.

Imperial Oil (IMO) Is Gushing Free Cash Flow – Final Thoughts

The majority of my exposure to the oil and gas industry is by way of my share ownership in CVX, XOM, TTE, and Enbridge (ENB); CVX and XOM were my 3rd and 19th largest holdings when I completed my mid-2022 Investment Holdings Review.

While IMO is attractively valued, I do not intend to initiate a position. I do, however, have indirect exposure to IMO because of XOM’s 69.6% ownership in the company.

Another article by Charles Fournier is Pass on Stanley Black and Decker.

Author Disclosure: I hold no position in IMO and have no intention of initiating one in the foreseeable future. I disclose holdings held in the FFJ Portfolio and the dividend income generated from these holdings. I do not disclose details of holdings held in various tax-advantaged accounts for confidentiality reasons.

Author Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

Related Articles on Dividend Power

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend histories, and much more. It is an excellent resource for DIY dividend growth investors and retirees.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

I am a self-taught investor and run the Financial Freedom is a Journey blog. I have invested in the North American equities markets for over 34 years. I retired from a career in banking and continue to invest as this is something about which I am passionate.